You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Coal India Limited CIL General Knowledge Question Paper Answers Model PaperDocument4 pagesCoal India Limited CIL General Knowledge Question Paper Answers Model PaperAshish Mahapatra77% (31)

- Coal India Limited FinalDocument30 pagesCoal India Limited FinaladihonNo ratings yet

- Coal MarketingDocument5 pagesCoal MarketingVenuNo ratings yet

- A Project Report On Financial Statement AnalysisDocument74 pagesA Project Report On Financial Statement AnalysisSushmita Barla100% (3)

- Coal Directory 2016-17Document213 pagesCoal Directory 2016-17pravinreddy67% (3)

- 04-A Mesurement in Business ResearchDocument3 pages04-A Mesurement in Business ResearchRaunak RayNo ratings yet

- 01 Introduction To MacroeconomicsDocument8 pages01 Introduction To MacroeconomicsRaunak RayNo ratings yet

- 05 Measuring The Cost of LivingDocument3 pages05 Measuring The Cost of LivingRaunak RayNo ratings yet

- Macroeconomics Vs MicroeconomicsDocument13 pagesMacroeconomics Vs MicroeconomicsRaunak RayNo ratings yet

- 03 The Data of MacroeconomicsDocument4 pages03 The Data of MacroeconomicsRaunak RayNo ratings yet

- 04 Real GDP Versus Nominal GDPDocument6 pages04 Real GDP Versus Nominal GDPRaunak RayNo ratings yet

- Annual REport Coal India 2020-21 New HtDoRsCDocument346 pagesAnnual REport Coal India 2020-21 New HtDoRsCRaunak RayNo ratings yet

- Solved XAT 2021 Paper With SolutionsDocument44 pagesSolved XAT 2021 Paper With SolutionsRaunak RayNo ratings yet

- Business Model of Coal India LTDDocument2 pagesBusiness Model of Coal India LTDKrutikaNo ratings yet

- Report11 12Document141 pagesReport11 12Anil SinghNo ratings yet

- Working Capital Management at CCLDocument127 pagesWorking Capital Management at CCLManishGupta67% (3)

- AdaniPower - Initiating CoverageDocument8 pagesAdaniPower - Initiating CoverageP VinayakamNo ratings yet

- July 23Document217 pagesJuly 23Priya SainiNo ratings yet

- Swati Patle Performance ApprisalDocument64 pagesSwati Patle Performance ApprisalujwaljaiswalNo ratings yet

- Secure Jobs.90164459Document175 pagesSecure Jobs.90164459MuraliNaiduNo ratings yet

- Tatasteel ReportDocument83 pagesTatasteel ReportBarun KumarNo ratings yet

- Project CollegeDocument75 pagesProject Collegehary vickyNo ratings yet

- Ann Rep 1011Document118 pagesAnn Rep 1011Rachit TiwariNo ratings yet

- CCL Avanshi Fianl ProjectDocument98 pagesCCL Avanshi Fianl ProjectSanjay NgarNo ratings yet

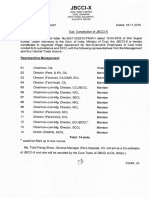

- COAL INDIA Constitution of JBCCI-XDocument3 pagesCOAL INDIA Constitution of JBCCI-Xrajat304shrivastavaNo ratings yet

- Eco Analysis Tata SteelDocument79 pagesEco Analysis Tata SteelRavNeet KaUrNo ratings yet

- Induction Material December 2005Document69 pagesInduction Material December 2005Rachit TiwariNo ratings yet

- Jefferies On Metal StocksDocument36 pagesJefferies On Metal StocksTejesh GoudNo ratings yet

- B) To CIL A To: Case As AsDocument6 pagesB) To CIL A To: Case As AsAjit KushwahaNo ratings yet

- Project Report On Recruitment and Selection at Cmpdi: 19 May2014 To 20 June 2014Document20 pagesProject Report On Recruitment and Selection at Cmpdi: 19 May2014 To 20 June 2014Sanjay SNo ratings yet

- Project Report On CNDocument42 pagesProject Report On CNBittu kumar mandalNo ratings yet

- "Capital Budgeting": A Summer Training Report OnDocument45 pages"Capital Budgeting": A Summer Training Report OnRahul BhagatNo ratings yet

- Baishakhu Ram Binjhavar Vs South Eastern Coaldields LTD On 11 September 2017Document58 pagesBaishakhu Ram Binjhavar Vs South Eastern Coaldields LTD On 11 September 2017Subhash SharmaNo ratings yet

- A Project of Liquidity Analysis & Trend Analysis: Coal India LimitedDocument54 pagesA Project of Liquidity Analysis & Trend Analysis: Coal India Limitedpooja07No ratings yet

- Swot AnalysisDocument22 pagesSwot AnalysisUddish BagriNo ratings yet

- Safety Objective Policy Organisation 28022013Document0 pagesSafety Objective Policy Organisation 28022013Nilpakhi NilNo ratings yet

- Employees Welfare and Social Security SchemesDocument8 pagesEmployees Welfare and Social Security SchemesPratik KhimaniNo ratings yet

- Fac Ratio Analysis Assignment Sector: Coal 1) Global Coal and Mining Pvt. LTDDocument25 pagesFac Ratio Analysis Assignment Sector: Coal 1) Global Coal and Mining Pvt. LTDankan dattaNo ratings yet