You might also like

- Unit 4 Accounting For Investments: Topic 5 - Investment in PropertyDocument7 pagesUnit 4 Accounting For Investments: Topic 5 - Investment in PropertyRey HandumonNo ratings yet

- Forest Products: Advanced Technologies and Economic AnalysesFrom EverandForest Products: Advanced Technologies and Economic AnalysesNo ratings yet

- Investment PropertyDocument5 pagesInvestment PropertyKristine PerezNo ratings yet

- Investment Property ProblemsDocument3 pagesInvestment Property ProblemsAbigail TalusanNo ratings yet

- 5-1 (Uy Company) : Property, Plant and Equipment ProblemsDocument13 pages5-1 (Uy Company) : Property, Plant and Equipment ProblemsExequielCamisaCrusperoNo ratings yet

- Intermediate Accounting Unit4 - Topic5Document7 pagesIntermediate Accounting Unit4 - Topic5Lea PolinarNo ratings yet

- Investment PropertyDocument14 pagesInvestment PropertyJerome BaluseroNo ratings yet

- Gonzales, Ian Rogel L. - Assignment#3Document4 pagesGonzales, Ian Rogel L. - Assignment#3GONZALES, IAN ROGEL L.No ratings yet

- ACCT 410 Candel Financial StatementDocument14 pagesACCT 410 Candel Financial StatementAthia Adams-KerrNo ratings yet

- ACC3201Document6 pagesACC3201natlyhNo ratings yet

- Quiz 3 Ppe QuestionsDocument4 pagesQuiz 3 Ppe QuestionsJessica Marie MigrasoNo ratings yet

- Audit of PPE AnnotatedDocument10 pagesAudit of PPE AnnotatedLloydNo ratings yet

- Kandy Co Draft FSMT and MobyDocument4 pagesKandy Co Draft FSMT and MobyAliNo ratings yet

- QuestionDocument2 pagesQuestionKamoheloNo ratings yet

- Finals Reviewer ACCTG34Document12 pagesFinals Reviewer ACCTG34Drey StudyingNo ratings yet

- Buscom 3Document4 pagesBuscom 3dmangiginNo ratings yet

- ACCO20093Document7 pagesACCO20093jfcNo ratings yet

- PpeDocument7 pagesPpeJer Rama100% (1)

- AP 004 D.1 Audit If Investments Prob. 1Document1 pageAP 004 D.1 Audit If Investments Prob. 1Loid Gumera LenchicoNo ratings yet

- #3 Financial Accounting and Reporting Test BankDocument32 pages#3 Financial Accounting and Reporting Test BankPatOcampo100% (5)

- Financial Accounting and Reporting Test Bank 80102016 - 3: - Investment in AssociateDocument10 pagesFinancial Accounting and Reporting Test Bank 80102016 - 3: - Investment in AssociateFery AnnNo ratings yet

- Multiple Choice Problems 9Document15 pagesMultiple Choice Problems 9Dieter LudwigNo ratings yet

- Follow-Up Problem SubsequentDocument4 pagesFollow-Up Problem SubsequentasdasdaNo ratings yet

- Gabriel Jay M. Mendoza OCTOBER 3, 2016 At3A - Advone Ms. Janine AbuDocument3 pagesGabriel Jay M. Mendoza OCTOBER 3, 2016 At3A - Advone Ms. Janine AbuGJ MendozaNo ratings yet

- Chap 13 - 1 To 5Document5 pagesChap 13 - 1 To 5Buenaventura, Lara Jane T.No ratings yet

- aNSWER 2Document5 pagesaNSWER 2Sinclair faith galarioNo ratings yet

- aNSWER 2Document5 pagesaNSWER 2Sinclair faith galarioNo ratings yet

- aNSWER 2Document5 pagesaNSWER 2Sinclair faith galarioNo ratings yet

- Answer 6Document5 pagesAnswer 6Sinclair faith galarioNo ratings yet

- Answer 6Document5 pagesAnswer 6Sinclair faith galarioNo ratings yet

- aNSWER 2Document5 pagesaNSWER 2Sinclair faith galarioNo ratings yet

- Answer 6Document5 pagesAnswer 6Sinclair faith galarioNo ratings yet

- Answer 6Document5 pagesAnswer 6Sinclair faith galarioNo ratings yet

- Exercise 13 Statement of Cash Flows - 054924Document2 pagesExercise 13 Statement of Cash Flows - 054924Hoyo VerseNo ratings yet

- Property, Plant and Equipment: Ppe - Pas 16 Tangible Assets PurposesDocument5 pagesProperty, Plant and Equipment: Ppe - Pas 16 Tangible Assets PurposesJp Combis0% (1)

- Final Long Quiz Acct 039Document3 pagesFinal Long Quiz Acct 039Karen YpilNo ratings yet

- Solutions-IAS 40Document7 pagesSolutions-IAS 40Blitz KaizerNo ratings yet

- Assessment No. 3-Midterm - Exam SheetDocument7 pagesAssessment No. 3-Midterm - Exam Sheetarnel buanNo ratings yet

- Describe and Illustrate The Acquisition Methods of Accounting For Business CombinationDocument5 pagesDescribe and Illustrate The Acquisition Methods of Accounting For Business CombinationAljenika Moncada GupiteoNo ratings yet

- Hifa NurafwaDocument8 pagesHifa Nurafwa20197 Elisa Nurhayati AhmadNo ratings yet

- Investment-Property-Non-Current-Asset-Held-For-Sale AnswersDocument6 pagesInvestment-Property-Non-Current-Asset-Held-For-Sale AnswersEvelina Del RosarioNo ratings yet

- Of Financial PositionDocument3 pagesOf Financial PositionIrah LouiseNo ratings yet

- Business Combinations - Net Asset AcquisitionDocument15 pagesBusiness Combinations - Net Asset AcquisitionLyca Mae CubangbangNo ratings yet

- LEC03B - BSA 2102 - 012021-Problems, Part IDocument3 pagesLEC03B - BSA 2102 - 012021-Problems, Part IKatarame LermanNo ratings yet

- Chapter 15Document9 pagesChapter 15Coleen Joy Sebastian PagalingNo ratings yet

- Local Media1556764160936285934Document5 pagesLocal Media1556764160936285934Prince PierreNo ratings yet

- PPE - Part - 1. CHAPTER 15Document22 pagesPPE - Part - 1. CHAPTER 15Ms VampireNo ratings yet

- Acc 113 - Accounting For Business CombinationsDocument8 pagesAcc 113 - Accounting For Business CombinationsAlthea CagakitNo ratings yet

- Abc Co. Statement of Financial Position As of December 31, 20x0 AssetsDocument37 pagesAbc Co. Statement of Financial Position As of December 31, 20x0 AssetsJonnafe Almendralejo IntanoNo ratings yet

- Problems Chapter 22 Investment PropertyDocument8 pagesProblems Chapter 22 Investment PropertyXNo ratings yet

- Practice Test 5.1 Ppe GarciaDocument3 pagesPractice Test 5.1 Ppe GarciaArlene Garcia100% (1)

- AA 4101 Midterm With AnswersDocument9 pagesAA 4101 Midterm With AnswersAlyssa AnnNo ratings yet

- Property, Plant and Equipment Chapter 15Document9 pagesProperty, Plant and Equipment Chapter 15Kiminosunoo LelNo ratings yet

- Property, Plant and Equipment Chapter 15Document9 pagesProperty, Plant and Equipment Chapter 15Kiminosunoo Lel100% (3)

- Assignment IV Advanced Financial Accounting Chapter 4&5Document6 pagesAssignment IV Advanced Financial Accounting Chapter 4&5Lidya AberaNo ratings yet

- Tutorial 40F - Suggested SolutionDocument4 pagesTutorial 40F - Suggested Solutionmusa morinNo ratings yet

- A311Chapter 10 ProblemsDocument43 pagesA311Chapter 10 ProblemsVibria Rezki Ananda0% (1)

- Chapter 21 - Investment PropertyDocument3 pagesChapter 21 - Investment PropertyXiena67% (3)

- Exercise 02 INTACC2 Cadiz Jericho E.Document15 pagesExercise 02 INTACC2 Cadiz Jericho E.Kervin Rey JacksonNo ratings yet

- Cebu (/sɛ Bu / Cebuano: Sugbo), Officially The Province of Cebu (Cebuano: Lalawigan Sa SugboDocument28 pagesCebu (/sɛ Bu / Cebuano: Sugbo), Officially The Province of Cebu (Cebuano: Lalawigan Sa SugboIsla PageNo ratings yet

- Central Visayas: Central Visayas (Cebuano: Tunga-Tungang Kabisay-An TagalogDocument7 pagesCentral Visayas: Central Visayas (Cebuano: Tunga-Tungang Kabisay-An TagalogIsla PageNo ratings yet

- Cebuano LanguageDocument15 pagesCebuano LanguageIsla PageNo ratings yet

- Chapter 8-General Ledger, Financial Reporting, and Management Reporting Systems True/FalseDocument8 pagesChapter 8-General Ledger, Financial Reporting, and Management Reporting Systems True/FalseIsla PageNo ratings yet

- Blaw Review Quiz PDF FreeDocument34 pagesBlaw Review Quiz PDF FreeIsla PageNo ratings yet

- Cpa Reviewer in Taxation by Tabag 2019pdf PDF FreeDocument259 pagesCpa Reviewer in Taxation by Tabag 2019pdf PDF FreeIsla PageNo ratings yet

- Hall 5e TB ch06Document14 pagesHall 5e TB ch06Isla PageNo ratings yet

- Accounting Cost Definition - AccountingToolsDocument2 pagesAccounting Cost Definition - AccountingToolsIsla PageNo ratings yet

- Q-6. Enter The Following Transactions in The Cash Book With Cash and BankDocument4 pagesQ-6. Enter The Following Transactions in The Cash Book With Cash and Bankkrish mehtaNo ratings yet

- DownloadDocument1 pageDownloadsandroNo ratings yet

- Role of "Sebi" in New Issue MarketDocument11 pagesRole of "Sebi" in New Issue MarketSwati RawatNo ratings yet

- Vol3-Ch3-Tools of Financial Statement AnalysisDocument40 pagesVol3-Ch3-Tools of Financial Statement Analysiswatchtimebro69No ratings yet

- Grade 7 EMS QP and Answer Sheets - Midyear 2022Document8 pagesGrade 7 EMS QP and Answer Sheets - Midyear 2022Life MakhubelaNo ratings yet

- 8.0money Demand & Money MKT EquilibriumDocument16 pages8.0money Demand & Money MKT EquilibriumJacquelyn ChungNo ratings yet

- Chapter 4 Review Principles of Accounting AnswersDocument3 pagesChapter 4 Review Principles of Accounting AnswersChien Phuong ThanhNo ratings yet

- Sonal Trivedi PDFDocument201 pagesSonal Trivedi PDFAshish RajputNo ratings yet

- Active EquityDocument9 pagesActive EquityHabib ImamNo ratings yet

- Installment BuyingDocument33 pagesInstallment BuyingNors PataytayNo ratings yet

- Ufr Quiz 4Document4 pagesUfr Quiz 4sam barrientosNo ratings yet

- The Indian Internet Banking JourneyDocument4 pagesThe Indian Internet Banking JourneySandeep MishraNo ratings yet

- Daima Bundles Customer Journey - Buy For OtherDocument10 pagesDaima Bundles Customer Journey - Buy For OtherALFRED KIPTISYANo ratings yet

- A Study On Sources of Fund and Its MobilizationDocument28 pagesA Study On Sources of Fund and Its MobilizationsaN bAn100% (1)

- Corporate Reporting-1Document69 pagesCorporate Reporting-1Najmul IslamNo ratings yet

- Gambling With Other People'S Money: Russell RobertsDocument44 pagesGambling With Other People'S Money: Russell Robertsjallan1984No ratings yet

- Jawaban Buku Besar UD. BUANA P3Document10 pagesJawaban Buku Besar UD. BUANA P3HusniBaroqNo ratings yet

- (CPAR2016) TAX-8014 (+llamado Notes - OTHER PERCENTAGE TAXES)Document12 pages(CPAR2016) TAX-8014 (+llamado Notes - OTHER PERCENTAGE TAXES)jamNo ratings yet

- ExercisesDocument11 pagesExercisesJirlin LncNo ratings yet

- Student Loan ABS 101Document27 pagesStudent Loan ABS 101yugehang100% (1)

- ICICIPru IProtectSmart MoneyBackDocument4 pagesICICIPru IProtectSmart MoneyBacksaurabh sumanNo ratings yet

- NC 079-80-264 Interest RatesDocument3 pagesNC 079-80-264 Interest RatesSaddam AliNo ratings yet

- Sbi Loan1Document1 pageSbi Loan1gangadhar_payyavulaNo ratings yet

- 01 Activity 1Document1 page01 Activity 1ToastedBaconNo ratings yet

- ENTREP10 MODULES-Quarter2-Week5-9Document16 pagesENTREP10 MODULES-Quarter2-Week5-9Kristel AcordonNo ratings yet

- Principles of Accounts 10Document70 pagesPrinciples of Accounts 10Jâmés Bøñd100% (2)

- European Banking UnionDocument7 pagesEuropean Banking Unionwim331No ratings yet

- Business Plan EnjeraDocument24 pagesBusiness Plan Enjerahinsene begna100% (1)

- Mcqs On ForexDocument43 pagesMcqs On ForexRam Iyer90% (10)

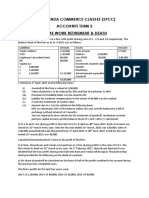

- Sunil Panda Commerce Classes (SPCC) Accounts Term 2 Home Work Retirement & DeathDocument3 pagesSunil Panda Commerce Classes (SPCC) Accounts Term 2 Home Work Retirement & DeathBinoy TrevadiaNo ratings yet