You might also like

- CGF ProjectDocument8 pagesCGF ProjectAvaniNo ratings yet

- Islamic Banking Theories and PracticesDocument13 pagesIslamic Banking Theories and PracticesUzmanNo ratings yet

- Meezan Bank LTDDocument53 pagesMeezan Bank LTDim.abid1No ratings yet

- Equality TestDocument17 pagesEquality TestKris Ani MarineNo ratings yet

- Islamic finance principlesDocument8 pagesIslamic finance principlesTopmax Training CollegeNo ratings yet

- Criticism of Fatwa Shopping and Need for Standardization in Islamic BankingDocument18 pagesCriticism of Fatwa Shopping and Need for Standardization in Islamic BankingMuhammad UsmanNo ratings yet

- Principles of Islamic FinanceDocument5 pagesPrinciples of Islamic Financemr basitNo ratings yet

- Fin546 Article ReviewDocument4 pagesFin546 Article ReviewZAINOOR IKMAL MAISARAH MOHAMAD NOORNo ratings yet

- Islamic Finance: and Its Ability To Adapt To Changes in The Outside WorldDocument9 pagesIslamic Finance: and Its Ability To Adapt To Changes in The Outside WorldUsman TallatNo ratings yet

- Islamic Investment PlanningDocument29 pagesIslamic Investment Planningmuhammad arifNo ratings yet

- Islamic Financial SystemDocument13 pagesIslamic Financial SystemMushood AmjadNo ratings yet

- Fin546 Article Review ZainoorDocument4 pagesFin546 Article Review ZainoorZAINOOR IKMAL MAISARAH MOHAMAD NOORNo ratings yet

- Islamic Finance Form 3Document13 pagesIslamic Finance Form 3AbdullahiNo ratings yet

- Article Review ZainoorDocument6 pagesArticle Review ZainoorZAINOOR IKMAL MAISARAH MOHAMAD NOORNo ratings yet

- Islamic Finance Effect On Public Islamic Bank BerhadDocument39 pagesIslamic Finance Effect On Public Islamic Bank BerhadHari Dass100% (1)

- Islamic Financing Arrangements Used in Islamic Banking: Author: Ehsan ZarrokhDocument25 pagesIslamic Financing Arrangements Used in Islamic Banking: Author: Ehsan ZarrokhD'n Hafiz DraegonoidNo ratings yet

- Financial Institutions in the Philippines and the Rise of Islamic BankingDocument7 pagesFinancial Institutions in the Philippines and the Rise of Islamic BankingMhot Rojas UnasNo ratings yet

- Islamic Banking and Shariah Compliance-Habib Ahmed-Drham University-UK-for ULDocument9 pagesIslamic Banking and Shariah Compliance-Habib Ahmed-Drham University-UK-for ULMaha AtifNo ratings yet

- Strategic Marketing Management. The Case of Islamic BankingDocument17 pagesStrategic Marketing Management. The Case of Islamic BankingNabil LahhamNo ratings yet

- Principle of Islamic FinanceDocument6 pagesPrinciple of Islamic FinanceumbreenNo ratings yet

- Islamic FinanceDocument2 pagesIslamic FinanceAkmal JohariNo ratings yet

- Sharia Aspects in Business and Finance (SABFDocument14 pagesSharia Aspects in Business and Finance (SABFSayed Sharif HashimiNo ratings yet

- "Shari'a", and The Exact Literal Translation of "Shari'a" Is "A Clear Path To Be Followed andDocument7 pages"Shari'a", and The Exact Literal Translation of "Shari'a" Is "A Clear Path To Be Followed andJohn Marc ChullNo ratings yet

- Islamic Financial SystemDocument15 pagesIslamic Financial SystemFarfoosh Farfoosh FarfooshNo ratings yet

- Mubashir Ameenudeen IFDocument6 pagesMubashir Ameenudeen IFLebbe PuthaNo ratings yet

- Riba, Profit and Islamic Rate Aand Market EquilibriumDocument31 pagesRiba, Profit and Islamic Rate Aand Market EquilibriumNurhidayatul AqmaNo ratings yet

- Some Issues On Murabahah Practices in Iran and Malaysian Islamic BanksDocument8 pagesSome Issues On Murabahah Practices in Iran and Malaysian Islamic BanksHarsh SonawaneNo ratings yet

- Shadman Haider, Islamiyat, BS 2B PDFDocument4 pagesShadman Haider, Islamiyat, BS 2B PDFShaista KhattakNo ratings yet

- Islamic & Conventional Banking (F)Document17 pagesIslamic & Conventional Banking (F)syedtahaaliNo ratings yet

- Overview of Islamic Finance and Banking Principles/TITLEDocument29 pagesOverview of Islamic Finance and Banking Principles/TITLESozia TanNo ratings yet

- Abdullah Nurul Sabri Bin Sulong 2019182261Document2 pagesAbdullah Nurul Sabri Bin Sulong 2019182261Afiq AdnanNo ratings yet

- Islamic Business ContractsDocument15 pagesIslamic Business Contracts_*_+~~>No ratings yet

- Islamic Banking Principles: Modern Justifications For InterestDocument3 pagesIslamic Banking Principles: Modern Justifications For InterestAamir IrfanNo ratings yet

- Islamic Finance SystemDocument4 pagesIslamic Finance SystemShahinNo ratings yet

- MBR 2015 06 Bilal+Ahmad+MalikDocument16 pagesMBR 2015 06 Bilal+Ahmad+MalikMalik Gazi BilalNo ratings yet

- The Role of Islamic Financial Systems and Banking Institutions in Global Economic RecoveryDocument41 pagesThe Role of Islamic Financial Systems and Banking Institutions in Global Economic Recoveryjhulz0763No ratings yet

- Shirkah Partnership by Shoayb JoosubDocument20 pagesShirkah Partnership by Shoayb JoosubRidhwan-ulHaqueNo ratings yet

- Discussion and RecommendationDocument8 pagesDiscussion and RecommendationNuranis QhaleedaNo ratings yet

- Islamic Finance HistoryDocument3 pagesIslamic Finance HistoryAbdul HayeeNo ratings yet

- Interest-Free Banking System: Objections, Reservations and Their EvaluationDocument19 pagesInterest-Free Banking System: Objections, Reservations and Their EvaluationSaqlain KhanNo ratings yet

- Muhammad AyubDocument26 pagesMuhammad AyubMuhammad SheikhNo ratings yet

- The Salient Features of Islamic Financial SystemDocument15 pagesThe Salient Features of Islamic Financial SystemFazli subhan100% (1)

- Interet Free Islamic Banks Vs Interest Based Conventional BanksDocument15 pagesInteret Free Islamic Banks Vs Interest Based Conventional BanksabidhasanNo ratings yet

- Broad Distinction Between Islamic ConventionalDocument18 pagesBroad Distinction Between Islamic ConventionalShoaib CheemaNo ratings yet

- Islamic Finance and Banking SystemDocument9 pagesIslamic Finance and Banking SystemSuhail RajputNo ratings yet

- 2395 5622 1 SMDocument10 pages2395 5622 1 SMzahwa wakhidahNo ratings yet

- 6179-Article Text-15651-1-10-20190217Document10 pages6179-Article Text-15651-1-10-20190217Habib Sultan KhelNo ratings yet

- Concept of Various Islamic Modes of Financing: 2.1.1 Mudarabah As A Mode of FinanceDocument3 pagesConcept of Various Islamic Modes of Financing: 2.1.1 Mudarabah As A Mode of FinancehudaNo ratings yet

- Itroduction BankingDocument8 pagesItroduction BankingusmansulemanNo ratings yet

- Corporate Finance AssignmentDocument4 pagesCorporate Finance AssignmentJogari125No ratings yet

- Social Reporting by Islamic BanksDocument24 pagesSocial Reporting by Islamic BanksAyman Ahmed CheemaNo ratings yet

- Giordano Dell-Amore Foundation Research Center On International Cooperation of The University of BergamoDocument13 pagesGiordano Dell-Amore Foundation Research Center On International Cooperation of The University of BergamoSaveeza Kabsha AbbasiNo ratings yet

- Islamic Finance IntroductionDocument5 pagesIslamic Finance Introductioneshaal naseemNo ratings yet

- 6 Financial Performance Analysis of Islamic BANK PDFDocument12 pages6 Financial Performance Analysis of Islamic BANK PDFakuNo ratings yet

- Islamic Modes of Financing: Mudarabah, Shirkah and Secondary ModesDocument26 pagesIslamic Modes of Financing: Mudarabah, Shirkah and Secondary ModesUmair Ahmed UmiNo ratings yet

- Question 2: Foreign Listing Affect Cost of Capital of Company. Banking Interest FreeDocument8 pagesQuestion 2: Foreign Listing Affect Cost of Capital of Company. Banking Interest FreeAhmed HadiNo ratings yet

- Ariff-Islamic Banking-A Variation of Conventional BankingDocument8 pagesAriff-Islamic Banking-A Variation of Conventional BankingDoha KashNo ratings yet

- Islamic Finance FoundationDocument22 pagesIslamic Finance Foundationapi-3734464No ratings yet

- As Such, Oral Communication Helps Us To Form Stronger Relationships and Build TrustDocument1 pageAs Such, Oral Communication Helps Us To Form Stronger Relationships and Build Trustsiti nadhirahNo ratings yet

- Greenbook Worldwide DirectoryDocument1 pageGreenbook Worldwide Directorysiti nadhirahNo ratings yet

- SOLE PROPRIETOR VS LLP VS COMPANY: COMPARING BUSINESS ENTITIES IN MALAYSIADocument4 pagesSOLE PROPRIETOR VS LLP VS COMPANY: COMPARING BUSINESS ENTITIES IN MALAYSIAsiti nadhirahNo ratings yet

- Tutorial Quiz ArchiveDocument4 pagesTutorial Quiz Archivesiti nadhirahNo ratings yet

- Additional Notes Accounting For AssociatesDocument14 pagesAdditional Notes Accounting For Associatessiti nadhirahNo ratings yet

- sc10 1Document2 pagessc10 1siti nadhirahNo ratings yet

- Harry Group Consolidated Statement of Financial Position As at 31.12.X7 RM'000 RM'000Document5 pagesHarry Group Consolidated Statement of Financial Position As at 31.12.X7 RM'000 RM'000siti nadhirahNo ratings yet

- Relationship of Partners and Outsiders (Third Parties) : Partner'S Authority To Bind The FirmDocument1 pageRelationship of Partners and Outsiders (Third Parties) : Partner'S Authority To Bind The Firmsiti nadhirahNo ratings yet

- Partnershi P Law: DefinitionDocument1 pagePartnershi P Law: Definitionsiti nadhirahNo ratings yet

- Exercise Chapter 1Document4 pagesExercise Chapter 1siti nadhirahNo ratings yet

- Company LAW: Classification of CompaniesDocument1 pageCompany LAW: Classification of Companiessiti nadhirah100% (1)

- Partnership Self Check KelipDocument1 pagePartnership Self Check Kelipsiti nadhirahNo ratings yet

- Dear Sir Abdul AzizDocument3 pagesDear Sir Abdul Azizsiti nadhirahNo ratings yet

- New Microsoft Word DocumentDocument1 pageNew Microsoft Word Documentsiti nadhirahNo ratings yet

- Q15 17Document2 pagesQ15 17siti nadhirahNo ratings yet

- Greenbook Worldwide DirectoryDocument1 pageGreenbook Worldwide Directorysiti nadhirahNo ratings yet

- Individual QDocument2 pagesIndividual Qsiti nadhirahNo ratings yet

- Podcast Outline ImprovementDocument2 pagesPodcast Outline Improvementsiti nadhirahNo ratings yet

- Exercise 20-12Document2 pagesExercise 20-12siti nadhirahNo ratings yet

- Dear Sir Abdul AzizDocument3 pagesDear Sir Abdul Azizsiti nadhirahNo ratings yet

- Exercise Chapter 1 Answer SheetDocument1 pageExercise Chapter 1 Answer Sheetsiti nadhirahNo ratings yet

- Corrigan Enterprises electrical component insertion system selection and breakeven analysisDocument1 pageCorrigan Enterprises electrical component insertion system selection and breakeven analysissiti nadhirahNo ratings yet

- Dear Sir Abdul AzizDocument3 pagesDear Sir Abdul Azizsiti nadhirahNo ratings yet

- Company LAW: Classification of CompaniesDocument1 pageCompany LAW: Classification of Companiessiti nadhirah100% (1)

- Calgary Paper Company Produces Paper For PhotocopiersDocument1 pageCalgary Paper Company Produces Paper For Photocopierssiti nadhirahNo ratings yet

- LawnMate Company Manufactures Power Mowers That Are Sold Throughout The United States andDocument2 pagesLawnMate Company Manufactures Power Mowers That Are Sold Throughout The United States andsiti nadhirahNo ratings yet

- Company LAW: Classification of CompaniesDocument1 pageCompany LAW: Classification of Companiessiti nadhirah100% (1)

- Calgary Paper Company Produces Paper For PhotocopiersDocument1 pageCalgary Paper Company Produces Paper For Photocopierssiti nadhirahNo ratings yet

- Partnership Self Check KelipDocument1 pagePartnership Self Check Kelipsiti nadhirahNo ratings yet

- Assessment Review - Corporate Finance Institute-21-40Document27 pagesAssessment Review - Corporate Finance Institute-21-40刘宝英No ratings yet

- Access Data: Statistic As Excel Data FileDocument5 pagesAccess Data: Statistic As Excel Data FileAKSHAT MITTALNo ratings yet

- Intimex Xuan Loc - Porfolio - 2022 (Autosaved)Document11 pagesIntimex Xuan Loc - Porfolio - 2022 (Autosaved)VyDangNo ratings yet

- Business Management - Study and Revision Guide - Paul Hoang - Hodder 2016Document194 pagesBusiness Management - Study and Revision Guide - Paul Hoang - Hodder 2016Cecy Vallejo LeónNo ratings yet

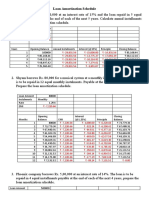

- Solution Time Value of Money 5 Loan Amortization Schedule and PV of Perpetual Annuity and PV Growing Annuity 3PVyvICyHiDocument5 pagesSolution Time Value of Money 5 Loan Amortization Schedule and PV of Perpetual Annuity and PV Growing Annuity 3PVyvICyHiShareshth JainNo ratings yet

- Week 1 - Introduction, Ethical and Legal IssuesDocument3 pagesWeek 1 - Introduction, Ethical and Legal IssuesTaneisha McLeanNo ratings yet

- Marketing Plan Final ReMarketing Plan of ACME Agrovet Beverage LTD PortDocument84 pagesMarketing Plan Final ReMarketing Plan of ACME Agrovet Beverage LTD PortNafiz FahimNo ratings yet

- Astral Records LTDDocument16 pagesAstral Records LTDMbavhalelo100% (2)

- ARBURG Customer Service Contact List 2021Document2 pagesARBURG Customer Service Contact List 2021Moises GeberNo ratings yet

- Girish KSDocument3 pagesGirish KSSudha PrintersNo ratings yet

- E-Commerce Website Using MERN StackDocument5 pagesE-Commerce Website Using MERN StackIJRASETPublicationsNo ratings yet

- Selling Groceries Through The Cloud in A Tier II City in IndiaDocument12 pagesSelling Groceries Through The Cloud in A Tier II City in IndiaFathima HeeraNo ratings yet

- Solution Manufacturing Prob. GRT ManufacturingDocument15 pagesSolution Manufacturing Prob. GRT ManufacturingCarmi FeceroNo ratings yet

- Business IdeaDocument5 pagesBusiness IdeaKarina SNo ratings yet

- AXIS BANK NDocument20 pagesAXIS BANK Nankit5849733% (3)

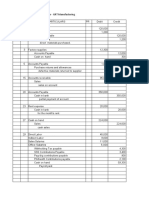

- Jayesh Gogri 170618 Records Payment PDFDocument72 pagesJayesh Gogri 170618 Records Payment PDFMadhur BihaniNo ratings yet

- Global Eyewear Market InsightsDocument2 pagesGlobal Eyewear Market InsightsAnshul NataniNo ratings yet

- Engineering Economics Questions Problem SolvingDocument4 pagesEngineering Economics Questions Problem SolvingLouie Jay LayderosNo ratings yet

- 2,3,8,10Document2 pages2,3,8,10SzaeNo ratings yet

- Week 3 ModuleDocument14 pagesWeek 3 ModuleSofia Biangca M. BalderasNo ratings yet

- Curriculum VitaeDocument2 pagesCurriculum Vitaeapi-628389548No ratings yet

- (VIP 90 - Tuần Số 14) Ngày 10.6 - Cụm Động Từ Nâng Cao (Buổi 2)Document3 pages(VIP 90 - Tuần Số 14) Ngày 10.6 - Cụm Động Từ Nâng Cao (Buổi 2)Nhân NguyễnNo ratings yet

- 773531Document38 pages773531Mohammed Khaja MohinuddinNo ratings yet

- Questionnaire SummaryDocument7 pagesQuestionnaire Summaryinfo -ADDMASNo ratings yet

- Business Implications of Sustainability Practices in Supply ChainsDocument25 pagesBusiness Implications of Sustainability Practices in Supply ChainsBizNo ratings yet

- Amigo Manufacturing V. Cluett Peabody CoDocument3 pagesAmigo Manufacturing V. Cluett Peabody CoShiela Arboleda MagnoNo ratings yet

- 4bs1 02 Que 20231122Document24 pages4bs1 02 Que 20231122supercoolhashir100% (1)

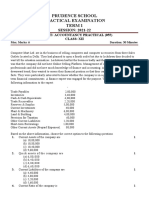

- Prudence School Accountancy Practical ExamDocument2 pagesPrudence School Accountancy Practical Examicarus fallsNo ratings yet

- Doles Vs AngelesDocument2 pagesDoles Vs Angelesfermo ii ramosNo ratings yet

- Booking Invoice - M06AI23I17058515 - LTADocument1 pageBooking Invoice - M06AI23I17058515 - LTANishant DuggalNo ratings yet