You might also like

- Eng Happiness 02jun14Document2 pagesEng Happiness 02jun14Yani IriawadiNo ratings yet

- 11 IndonesiaDocument2 pages11 IndonesiaYani IriawadiNo ratings yet

- Country Operations Business Plan: IndonesiaDocument13 pagesCountry Operations Business Plan: IndonesiaYani IriawadiNo ratings yet

- 2013 Country Forecast IndonesiaDocument5 pages2013 Country Forecast IndonesiaYani IriawadiNo ratings yet

- 2013 Country Forecast IndonesiaDocument5 pages2013 Country Forecast IndonesiaYani IriawadiNo ratings yet

- Franchise The European Esports MarketDocument40 pagesFranchise The European Esports MarketYani IriawadiNo ratings yet

- Asean GDP ForecastDocument5 pagesAsean GDP ForecastmartinezpujolNo ratings yet

- Indonesia: 2014: Watch This SpaceDocument2 pagesIndonesia: 2014: Watch This SpaceYani IriawadiNo ratings yet

- Brand Identity Manual: © 2011 The Open GroupDocument39 pagesBrand Identity Manual: © 2011 The Open GroupAhmad YNo ratings yet

- Philips GuidelinesDocument8 pagesPhilips Guidelinesjuan aguilarNo ratings yet

- Corporate Identity Manual: The Alberta GovernmentDocument119 pagesCorporate Identity Manual: The Alberta GovernmentYani IriawadiNo ratings yet

- Fedex Corporate Identity Quick ReferenceDocument12 pagesFedex Corporate Identity Quick ReferencePaulo CostaNo ratings yet

- Corporate Identity Guidelines: Guidelines For Using The Markant Brand NameDocument26 pagesCorporate Identity Guidelines: Guidelines For Using The Markant Brand NameYani IriawadiNo ratings yet

- BrandZ 2015 Indonesia Top50 ChartDocument1 pageBrandZ 2015 Indonesia Top50 ChartYani IriawadiNo ratings yet

- Communication Plan Albany ParkDocument31 pagesCommunication Plan Albany ParkYani IriawadiNo ratings yet

- Corporate Identity: July 2006Document17 pagesCorporate Identity: July 2006Yani IriawadiNo ratings yet

- Internalrules UKDocument5 pagesInternalrules UKYani IriawadiNo ratings yet

- Disney USA VS JapanDocument61 pagesDisney USA VS JapanYani IriawadiNo ratings yet

- 4.NPF Training - Procurement Strategy-Procurement PlanDocument42 pages4.NPF Training - Procurement Strategy-Procurement PlanPriyanka MNo ratings yet

- Maria Fitriah@yahoo - Co.idDocument10 pagesMaria Fitriah@yahoo - Co.idathifa finkaNo ratings yet

- Brief Digital Media & Marketing Plan For Theme Parks & Amusement ParksDocument14 pagesBrief Digital Media & Marketing Plan For Theme Parks & Amusement ParksYani IriawadiNo ratings yet

- Digital Image Copyright PaperDocument39 pagesDigital Image Copyright PaperYani IriawadiNo ratings yet

- Cooperation & Investment Proposition SlovakiaDocument21 pagesCooperation & Investment Proposition SlovakiaYani IriawadiNo ratings yet

- Data Management Plan Attachment - 0Document36 pagesData Management Plan Attachment - 0Yani IriawadiNo ratings yet

- Brief Digital Media & Marketing Plan For Theme Parks & Amusement ParksDocument14 pagesBrief Digital Media & Marketing Plan For Theme Parks & Amusement ParksYani IriawadiNo ratings yet

- FORREC Theme ParksDocument72 pagesFORREC Theme ParksKoushali BanerjeeNo ratings yet

- Disney USA VS JapanDocument61 pagesDisney USA VS JapanYani IriawadiNo ratings yet

- 1 Procurement Best Practice Guideline Procurement Planning enDocument13 pages1 Procurement Best Practice Guideline Procurement Planning enYani IriawadiNo ratings yet

- Cooperation & Investment Proposition SlovakiaDocument21 pagesCooperation & Investment Proposition SlovakiaYani IriawadiNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

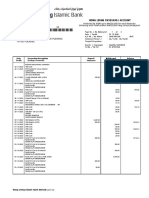

- Schedule of Fees & ChargesDocument9 pagesSchedule of Fees & ChargesJamesNo ratings yet

- High Yield Bonds Market Structure, Valuation, and Portfolio StrategiesDocument689 pagesHigh Yield Bonds Market Structure, Valuation, and Portfolio StrategiesFurqaan Syah100% (1)

- Bank Reconciliation Statement:: Unit - 6Document4 pagesBank Reconciliation Statement:: Unit - 6deepshrmNo ratings yet

- Business Finance Week 7 Basic Long-Term Financial ConceptsDocument16 pagesBusiness Finance Week 7 Basic Long-Term Financial ConceptsJessa Gallardo0% (1)

- Milton Friedman (1975) There's No Such Thing As A Free LunchDocument340 pagesMilton Friedman (1975) There's No Such Thing As A Free Lunchislasoy100% (1)

- Mgt101-5 - Ledger - Books of Secondary Entries and Trial BalanceDocument69 pagesMgt101-5 - Ledger - Books of Secondary Entries and Trial BalanceSaqib MalghaniNo ratings yet

- KPMG Flash News Hitesh Satishchandra DoshiDocument7 pagesKPMG Flash News Hitesh Satishchandra DoshiHimanshuNo ratings yet

- Annual Report 2 PDFDocument156 pagesAnnual Report 2 PDFSassy TanNo ratings yet

- 1 T1TOL - Overview - R10.1Document55 pages1 T1TOL - Overview - R10.1Tanaka Machana100% (1)

- 01 03 Accretion Dilution AfterDocument3 pages01 03 Accretion Dilution AfterДоминик КоббNo ratings yet

- Individual Assignment OneDocument3 pagesIndividual Assignment OnefeyselNo ratings yet

- Contemporary Financial Management 14th Edition Moyer Solutions ManualDocument7 pagesContemporary Financial Management 14th Edition Moyer Solutions Manualbenjaminnelsonijmekzfdos100% (13)

- Chapter 1:-The Nature of Capital MarketDocument9 pagesChapter 1:-The Nature of Capital MarketJaideep SharmaNo ratings yet

- Certificate in International Payment Systems BangaloreDocument4 pagesCertificate in International Payment Systems BangaloreMakarand LonkarNo ratings yet

- Hill CountryDocument8 pagesHill CountryAtif Raza AkbarNo ratings yet

- Shreve Stochcal4fin 1Document52 pagesShreve Stochcal4fin 1Daniel HeNo ratings yet

- RBI Branch and ATM Expansion LiberalizedDocument9 pagesRBI Branch and ATM Expansion LiberalizedbistamasterNo ratings yet

- Reuters Islamic Finance Development Report2018Document44 pagesReuters Islamic Finance Development Report2018Rehan Farhat100% (1)

- NHB Vishal GoyalDocument24 pagesNHB Vishal GoyalSky walkingNo ratings yet

- What Is Credit AnalysisDocument7 pagesWhat Is Credit AnalysisAbyotBeyechaNo ratings yet

- HLB Receipt 289062Document3 pagesHLB Receipt 289062devanboy 2007No ratings yet

- 1 Investment F PDFDocument35 pages1 Investment F PDFShrikant Mahajan100% (2)

- Account Titles UsedDocument40 pagesAccount Titles Usedmaria cacaoNo ratings yet

- Nit11 PDFDocument239 pagesNit11 PDFexecutive engineerNo ratings yet

- ValuationDocument3 pagesValuationBryan IbarrientosNo ratings yet

- Market Analysis November 2020Document21 pagesMarket Analysis November 2020Lau Wai KentNo ratings yet

- Stock Market and Trading Mechanism: Chapter - 2Document77 pagesStock Market and Trading Mechanism: Chapter - 2Nidhi JajodiaNo ratings yet

- Cca CPP HcaDocument1 pageCca CPP Hcahusse fokNo ratings yet

- Jason Matheson Paystub 2Document1 pageJason Matheson Paystub 2wadewilliamsperling1992No ratings yet