You might also like

- Term Sheet Guide: Don't Rely On The Same Counsel As Your InvestorsDocument19 pagesTerm Sheet Guide: Don't Rely On The Same Counsel As Your InvestorsPrerana Rai Bhandari100% (2)

- Statement 517014 78338832 22 Dec 2023Document5 pagesStatement 517014 78338832 22 Dec 2023cressidafunkeadedareNo ratings yet

- Monzo Bank Statement 2022 10 01-2022 10 06 703Document3 pagesMonzo Bank Statement 2022 10 01-2022 10 06 703Monila PunNo ratings yet

- Sample Motion To Plea BargainDocument2 pagesSample Motion To Plea BargainPat BarrugaNo ratings yet

- Vehicle Insurance PDFDocument1 pageVehicle Insurance PDFNiren KsNo ratings yet

- Anchor BoltDocument7 pagesAnchor BoltChris OngNo ratings yet

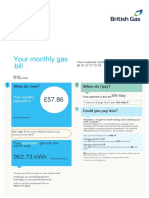

- British-Gas BillDocument1 pageBritish-Gas Bills.934263No ratings yet

- PDF BahramDocument3 pagesPDF Bahramxfzm99mr8rNo ratings yet

- Chabal Laura ClaireDocument4 pagesChabal Laura ClaireITNo ratings yet

- Investigation 3Document1 pageInvestigation 3cressidafunkeadedareNo ratings yet

- 2023 10 14 YourTalkTalkBillDocument2 pages2023 10 14 YourTalkTalkBilldupceleyonut100% (1)

- Movement For TelanganaDocument5 pagesMovement For TelanganaTanu RdNo ratings yet

- Re: Summons (The Bear™ Holdings Ltd. vs. Iamnero vs. Her Majesty The Queen)Document1 pageRe: Summons (The Bear™ Holdings Ltd. vs. Iamnero vs. Her Majesty The Queen)ethan8572No ratings yet

- Silver Account 06 December 2021 To 06 June 2022: Abuzeid Huda AliDocument2 pagesSilver Account 06 December 2021 To 06 June 2022: Abuzeid Huda Alimohamed elmakhzniNo ratings yet

- A Guide To Our HMRC Tax Calculation & Tax Year Overview RequirementsDocument7 pagesA Guide To Our HMRC Tax Calculation & Tax Year Overview RequirementsbswaminaNo ratings yet

- Preview 2Document3 pagesPreview 2g6psbtnb87No ratings yet

- Preview PDFDocument5 pagesPreview PDFUbong UmorenNo ratings yet

- HFHSC Crisis Communication PlanDocument22 pagesHFHSC Crisis Communication PlanJgjbfhbbgbNo ratings yet

- Strategic Management Analysis of PepsiCoDocument23 pagesStrategic Management Analysis of PepsiCoFirewing225No ratings yet

- Dent Eimear LindaDocument4 pagesDent Eimear LindaITNo ratings yet

- SS033790C 52 Ionela Claudia Insuratelu 30-03-2023Document1 pageSS033790C 52 Ionela Claudia Insuratelu 30-03-2023Ionela InsurateluNo ratings yet

- Halifax Statement Jan19Document1 pageHalifax Statement Jan19alexpicary79No ratings yet

- Goods Documents Required Customs Prescriptions Remarks: IrelandDocument4 pagesGoods Documents Required Customs Prescriptions Remarks: IrelandKelz YouknowmynameNo ratings yet

- invoice (с)Document1 pageinvoice (с)OlgaNo ratings yet

- HTTPSWWW - Tvlicensing.co - Ukcsupdateyour Licencedownload Licence - AppDocument1 pageHTTPSWWW - Tvlicensing.co - Ukcsupdateyour Licencedownload Licence - AppmeurialjohnsonNo ratings yet

- A Gas-1-5-2-4-2-1-2-1-1-1-3-1-1Document1 pageA Gas-1-5-2-4-2-1-2-1-1-1-3-1-1Daia SorinNo ratings yet

- 2022 12 23 YourTalkTalkBill-2-2-2Document2 pages2022 12 23 YourTalkTalkBill-2-2-2apple3215522No ratings yet

- Statement PDFDocument7 pagesStatement PDFSamir GhimireNo ratings yet

- FATCA CRS Curing DeclarationDocument1 pageFATCA CRS Curing DeclarationramdpcNo ratings yet

- Hac Ctbill 311139418 044 00021Document2 pagesHac Ctbill 311139418 044 00021esthermabengiNo ratings yet

- UK Driving License - Online Apply For Provisional License UKDocument10 pagesUK Driving License - Online Apply For Provisional License UKelizabethexcited0No ratings yet

- Current-Account-Statement 01032024 BRETTDocument3 pagesCurrent-Account-Statement 01032024 BRETTjohnsonwto15No ratings yet

- The VAT GuideDocument195 pagesThe VAT Guidestingray2No ratings yet

- Filling in Your VAT ReturnDocument28 pagesFilling in Your VAT ReturnkbassignmentNo ratings yet

- Atr Waste Carrier Licence Valid To 25.09.2026Document1 pageAtr Waste Carrier Licence Valid To 25.09.2026Anytime Recycling AccountsNo ratings yet

- InvoiceDocument3 pagesInvoiceNicole ManriquezNo ratings yet

- Council Tax Bill 2023/24Document2 pagesCouncil Tax Bill 2023/24shahin.imani69No ratings yet

- Assured Shorthold Tenancy AgreementDocument1 pageAssured Shorthold Tenancy Agreementfuddy luziNo ratings yet

- 2023 10 14 YourTalkTalkBillDocument2 pages2023 10 14 YourTalkTalkBilldupceleyonutNo ratings yet

- Ban204 - RegusDocument4 pagesBan204 - Regusshakhawat_cNo ratings yet

- Bill 10296080Document1 pageBill 10296080luminitamihai775No ratings yet

- IndianDocument1 pageIndianxfzm99mr8rNo ratings yet

- Statement 25-MAY-22 AC 43388212 28153934Document7 pagesStatement 25-MAY-22 AC 43388212 28153934cecilia mwangiNo ratings yet

- Deloitte Refund Guide 2011Document186 pagesDeloitte Refund Guide 2011Andrea OrsiNo ratings yet

- Nathan MusondaDocument1 pageNathan MusondaTeam PritomNo ratings yet

- CorrespondenceDocument5 pagesCorrespondenceUsakikamiNo ratings yet

- Civil Service Exam ReviewerDocument23 pagesCivil Service Exam ReviewerVanessa Marie CalitisinNo ratings yet

- AST Tenancy Agreement - TDS - Landlord RentDocument42 pagesAST Tenancy Agreement - TDS - Landlord RentGareth McKnightNo ratings yet

- Countingup Statement 2023 07Document1 pageCountingup Statement 2023 07SophiaNo ratings yet

- Edited - 519896510 Statement 104644 1753353Document2 pagesEdited - 519896510 Statement 104644 1753353contability121.ukNo ratings yet

- Update Letter 244135531Document2 pagesUpdate Letter 244135531Sam VeeversNo ratings yet

- ICON College of Technology and Management Course: Btec HND in Business, Unit 12: TaxationDocument6 pagesICON College of Technology and Management Course: Btec HND in Business, Unit 12: TaxationmuhammadislamkhanNo ratings yet

- United Kingdom Utility Gas StatementDocument2 pagesUnited Kingdom Utility Gas StatementAyilaran EmmanuelNo ratings yet

- Council TaxDocument1 pageCouncil Taxsteve.hartNo ratings yet

- AGREEMENT For Letting Furnished Dwelling House On An Assured ShortholdDocument8 pagesAGREEMENT For Letting Furnished Dwelling House On An Assured Shortholdapi-15458720100% (2)

- CustomInvoice 4642100886Document1 pageCustomInvoice 4642100886cgdgg4xbgs100% (1)

- DCONSCDocument5 pagesDCONSCAnonymous Ih1EEENo ratings yet

- Wise Credit Card StatementDocument1 pageWise Credit Card StatementAr MediaNo ratings yet

- Lesco - Web BillDocument1 pageLesco - Web BillRizwan KhalidNo ratings yet

- 2021.01.27 - Home Sec Reply To Open LetterDocument4 pages2021.01.27 - Home Sec Reply To Open LetterWLNo ratings yet

- Land Registry2Document1 pageLand Registry2Pritom NasirNo ratings yet

- E.ON BIll Dec-Feb 2023Document2 pagesE.ON BIll Dec-Feb 2023Eric CartmanNo ratings yet

- Halifax StatementDocument4 pagesHalifax StatementSW ProjectNo ratings yet

- NinoDocument1 pageNinoSavage GuyNo ratings yet

- E-On Energy 15-Jun-2022Document2 pagesE-On Energy 15-Jun-2022kellyNo ratings yet

- Details To Give Your Employer - GOV - UKDocument1 pageDetails To Give Your Employer - GOV - UKXandeNo ratings yet

- HMRC PDFDocument17 pagesHMRC PDFjohnnybck1125No ratings yet

- Week 9, CT Losses, 2022-23 - TutorDocument32 pagesWeek 9, CT Losses, 2022-23 - Tutorarpita aroraNo ratings yet

- Citric Acid Cycle Fill in The BlankDocument1 pageCitric Acid Cycle Fill in The BlankAntoon LorentsNo ratings yet

- Information Sheet: Liquidity Manager 35 Day Notice AccountDocument2 pagesInformation Sheet: Liquidity Manager 35 Day Notice AccountAntoon LorentsNo ratings yet

- GMP and GDP Certification Programme: Join More Than 4,000 Colleagues in The Academy!Document10 pagesGMP and GDP Certification Programme: Join More Than 4,000 Colleagues in The Academy!Antoon LorentsNo ratings yet

- Curriculum 2019a Briefing Exisiting StudentsDocument44 pagesCurriculum 2019a Briefing Exisiting StudentsAntoon LorentsNo ratings yet

- Questions To Ask Physicians During ShadowingDocument1 pageQuestions To Ask Physicians During ShadowingAntoon LorentsNo ratings yet

- Aprons Appendix 3C Framework Agreement Specification Lines Metric Dimensions Final 10022016 PDFDocument1 pageAprons Appendix 3C Framework Agreement Specification Lines Metric Dimensions Final 10022016 PDFAntoon LorentsNo ratings yet

- To Be UN3291 Certificated: Gusseted Bag Diagram Pillow Bag DiagramDocument1 pageTo Be UN3291 Certificated: Gusseted Bag Diagram Pillow Bag DiagramAntoon LorentsNo ratings yet

- VMS002 Adult Body Bag Framework Agreement Specification Lines Metric Dimensions Final 10022016 00F PDFDocument1 pageVMS002 Adult Body Bag Framework Agreement Specification Lines Metric Dimensions Final 10022016 00F PDFAntoon LorentsNo ratings yet

- Fit Testing Solutitons Specifications PDFDocument1 pageFit Testing Solutitons Specifications PDFAntoon LorentsNo ratings yet

- Specification For Chlorine Tablets and Granules: 1. Product DescriptionDocument2 pagesSpecification For Chlorine Tablets and Granules: 1. Product DescriptionAntoon LorentsNo ratings yet

- Hand Wash SpecificationDocument2 pagesHand Wash SpecificationAntoon LorentsNo ratings yet

- User Guidance - Essential Technical Requirements For Personal Protective EquipmentDocument3 pagesUser Guidance - Essential Technical Requirements For Personal Protective EquipmentAntoon LorentsNo ratings yet

- An Overview of Nano/Micro/Meso Scale Manufacturing at NIST: Edward Amatucci Nicholas DagalakisDocument26 pagesAn Overview of Nano/Micro/Meso Scale Manufacturing at NIST: Edward Amatucci Nicholas DagalakisAntoon LorentsNo ratings yet

- LogcatDocument14 pagesLogcatprathmeshmarathe240No ratings yet

- Values and Mission of Coca ColaDocument2 pagesValues and Mission of Coca ColaUjjwal AryalNo ratings yet

- Apos A8 Datasheet Oct20Document2 pagesApos A8 Datasheet Oct20aidara yannickNo ratings yet

- Quarkus 2Document10 pagesQuarkus 2Laszlo KamlerNo ratings yet

- AlgorithmDocument17 pagesAlgorithmMahamad AliNo ratings yet

- Decimal To Binary (By Me)Document4 pagesDecimal To Binary (By Me)Raj Patel100% (1)

- Dodocool DA106 Instruction Manual PDFDocument1 pageDodocool DA106 Instruction Manual PDFginostraNo ratings yet

- Bahasa Inggeris (Penulisan) 014 UPPM 1/ 2018 Tahun 6 1 Jam 15 MinitDocument8 pagesBahasa Inggeris (Penulisan) 014 UPPM 1/ 2018 Tahun 6 1 Jam 15 MinitAli KhanNo ratings yet

- Component Based Software EngineeringDocument21 pagesComponent Based Software Engineeringkarishma10No ratings yet

- Examen Parcial Semana 4 Esp Segundo Bloque Ingles General II Grupo3 PDFDocument12 pagesExamen Parcial Semana 4 Esp Segundo Bloque Ingles General II Grupo3 PDFOmar alvarez FalcoNo ratings yet

- Steady and Unsteady Pressure Measurements in A Transonic Turbine StageDocument1 pageSteady and Unsteady Pressure Measurements in A Transonic Turbine StageVarun Karthikeyan ShettyNo ratings yet

- Immigration: Coming To The UKDocument2 pagesImmigration: Coming To The UKoliverNo ratings yet

- Petrol Heads IIFTDocument4 pagesPetrol Heads IIFTKopalJaiswalNo ratings yet

- Creative Accounting Full EditDocument11 pagesCreative Accounting Full EditHabib MohdNo ratings yet

- 2.2 Brabham Pavilion and Neighbourhood Park Design ReportDocument11 pages2.2 Brabham Pavilion and Neighbourhood Park Design ReportMUSKAANNo ratings yet

- Familiarization With The Basics of Python Programming: Chapter-2Document37 pagesFamiliarization With The Basics of Python Programming: Chapter-2Santosh ShresthaNo ratings yet

- Full Download Microeconomics 6th Edition Hubbard Solutions Manual PDF Full ChapterDocument36 pagesFull Download Microeconomics 6th Edition Hubbard Solutions Manual PDF Full Chapteriatricalremittalf5qe8n100% (18)

- Shogun 2001 Fuel ProblemDocument6 pagesShogun 2001 Fuel ProblemJose GilmerNo ratings yet

- Smartplant Review: Getting Started GuideDocument33 pagesSmartplant Review: Getting Started Guidewill_streetNo ratings yet

- How To Make Value-Based Care Work in CardiologyDocument29 pagesHow To Make Value-Based Care Work in CardiologyPat WilsonNo ratings yet

- Pilipinas Shell Petroleum Corp. vs. Oil Industry BoardDocument2 pagesPilipinas Shell Petroleum Corp. vs. Oil Industry BoardLawrence SantiagoNo ratings yet

- 2015 SOET - Seat PlanDocument37 pages2015 SOET - Seat PlanankitNo ratings yet