You might also like

- Asia’s Fiscal Challenge: Financing the Social Protection Agenda of the Sustainable Development GoalsFrom EverandAsia’s Fiscal Challenge: Financing the Social Protection Agenda of the Sustainable Development GoalsNo ratings yet

- Aatm Nirbhar Abhiyan: Analysis of Promises and ImplementationDocument8 pagesAatm Nirbhar Abhiyan: Analysis of Promises and ImplementationNeha MakeoversNo ratings yet

- Private Sector Operations in 2019: Report on Development EffectivenessFrom EverandPrivate Sector Operations in 2019: Report on Development EffectivenessNo ratings yet

- Atma Bharat NirmaanDocument5 pagesAtma Bharat Nirmaansimran yadavNo ratings yet

- Union Budget 2015-16 HighlightsDocument8 pagesUnion Budget 2015-16 HighlightsManish MishraNo ratings yet

- Covid 19: Monetary Measures Taken by RBIDocument3 pagesCovid 19: Monetary Measures Taken by RBIPeyush NeneNo ratings yet

- February 28, 2015: Key Features of Budget 2015-2016Document17 pagesFebruary 28, 2015: Key Features of Budget 2015-2016Rajendra Prasad R SNo ratings yet

- Interim Budget 2019: Key Announcements for Farmers, Poor, Middle Class and DefenceDocument5 pagesInterim Budget 2019: Key Announcements for Farmers, Poor, Middle Class and DefenceABHISHEK SINGHNo ratings yet

- AatmaNirbhar Bharat 3.0Document4 pagesAatmaNirbhar Bharat 3.0Vishnu KanthNo ratings yet

- Liquidity Injection - A Real Solution To The Current Crisis in India?Document4 pagesLiquidity Injection - A Real Solution To The Current Crisis in India?CritiNo ratings yet

- Highlights of The Union Budget 2022 Partt 222Document33 pagesHighlights of The Union Budget 2022 Partt 222KUSUMA ANo ratings yet

- QIP Is A Process Which Was Introduced by SEBI So As To Enable The Listed Companies To RaiseDocument5 pagesQIP Is A Process Which Was Introduced by SEBI So As To Enable The Listed Companies To Raisekaviya.vNo ratings yet

- Union Budget 2021 - 22: Anuj JindalDocument20 pagesUnion Budget 2021 - 22: Anuj JindalamritNo ratings yet

- Impact of Atmanirbhar Bharat on Hustler EntrepreneursDocument19 pagesImpact of Atmanirbhar Bharat on Hustler EntrepreneursAnu RadhaNo ratings yet

- Topic: Indian Economy and Issues Relating To Planning, Mobilization of Resources, Growth, Development and EmploymentDocument12 pagesTopic: Indian Economy and Issues Relating To Planning, Mobilization of Resources, Growth, Development and EmploymentRoshni AgarwalNo ratings yet

- Union BudgetDocument9 pagesUnion BudgetsameeraNo ratings yet

- Wealth Management Budget InsightsDocument15 pagesWealth Management Budget InsightsAkash PamnaniNo ratings yet

- The Hindu Review (July 2019)Document23 pagesThe Hindu Review (July 2019)mense vishalNo ratings yet

- The Hindu Review July 2019 PDFDocument23 pagesThe Hindu Review July 2019 PDFSiva ShankarNo ratings yet

- Atmanirbhar Abhiyan PackageDocument17 pagesAtmanirbhar Abhiyan PackageAnkona MondalNo ratings yet

- Interim Budget 2019Document8 pagesInterim Budget 2019Deepansh goyalNo ratings yet

- Government aid and recovery measures during COVID-19 pandemicDocument28 pagesGovernment aid and recovery measures during COVID-19 pandemicGaurav KeswaniNo ratings yet

- Key Highlights of India's $5 Trillion Economy Vision in Union Budget 2019Document42 pagesKey Highlights of India's $5 Trillion Economy Vision in Union Budget 2019fxfdsxshshsdhNo ratings yet

- Key Features of Budget 2015-16 (English)Document14 pagesKey Features of Budget 2015-16 (English)Sunil SharmaNo ratings yet

- Nterim Budget: Submitted By: Vinit Gavhade Roll No.: IC2K14-88Document10 pagesNterim Budget: Submitted By: Vinit Gavhade Roll No.: IC2K14-88Anshika RaiNo ratings yet

- The Hindu Review July 2019Document24 pagesThe Hindu Review July 2019Anas HashmiNo ratings yet

- Current Affairs - October 2020 - Indian EconomyDocument25 pagesCurrent Affairs - October 2020 - Indian Economyjaisriramjaisriram651No ratings yet

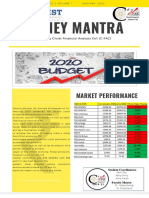

- Money Mantra: Market PerformanceDocument4 pagesMoney Mantra: Market PerformanceAlbin SibyNo ratings yet

- Self-Reliant India Movement - An OpportunityDocument15 pagesSelf-Reliant India Movement - An OpportunitySANTOSH KUMARNo ratings yet

- Write-Up Aatma Nirbhar Bharat - Team JupiterDocument32 pagesWrite-Up Aatma Nirbhar Bharat - Team JupiterRushali AgarwalNo ratings yet

- Indian Budget 2011 Key Features and AnalysisDocument8 pagesIndian Budget 2011 Key Features and AnalysisVaibhav GuptaNo ratings yet

- Government Schemes - GKmojoDocument15 pagesGovernment Schemes - GKmojoVikas TiwariNo ratings yet

- 2020 DecDocument61 pages2020 DecLokeshNo ratings yet

- Highlights of Interim - pdf-37 PDFDocument7 pagesHighlights of Interim - pdf-37 PDFRohit RajNo ratings yet

- Budget 2019Document7 pagesBudget 2019abcd123454321No ratings yet

- FMCGDocument6 pagesFMCGRahul DudejaNo ratings yet

- Major parts of stimulus packages by India and BangladeshDocument6 pagesMajor parts of stimulus packages by India and BangladeshMd. Ashikur Rahman 2016045660No ratings yet

- Pak COVID StimulusDocument6 pagesPak COVID StimulusshNo ratings yet

- Budget and SurveyDocument21 pagesBudget and SurveyNikul ParmarNo ratings yet

- Union Budget 2019-20 Highlights: Top Highlights From 2019 Budget Session by Interim Finance Minister Piyush GoyalDocument3 pagesUnion Budget 2019-20 Highlights: Top Highlights From 2019 Budget Session by Interim Finance Minister Piyush GoyalPrathmesh RathoreNo ratings yet

- AK Gupta 5 PDFDocument38 pagesAK Gupta 5 PDFकायथ रोहितNo ratings yet

- Union Budget 2017-18: Key Highlights SummaryDocument4 pagesUnion Budget 2017-18: Key Highlights SummarySushma KumariNo ratings yet

- Highlights of Budget 2019Document4 pagesHighlights of Budget 2019harisankar sureshNo ratings yet

- Key Features of Budget 2014-2015: The Current Economic Situation and The ChallengesDocument21 pagesKey Features of Budget 2014-2015: The Current Economic Situation and The ChallengesBakrudeen Ali AhamedNo ratings yet

- EconomyDocument10 pagesEconomyjyothisaiswaroop satuluriNo ratings yet

- Indian Union Budget 2020Document11 pagesIndian Union Budget 2020Md DhaniyalNo ratings yet

- Key Features of Union Budget 2015 16Document3 pagesKey Features of Union Budget 2015 16prasannandaNo ratings yet

- Key Features of Budget 2014Document5 pagesKey Features of Budget 2014Roxanne AyalaNo ratings yet

- MsmeDocument10 pagesMsmeFurqan AhmedNo ratings yet

- Budget 22Document4 pagesBudget 22rkNo ratings yet

- Union Budget 2023-24: Why in News?Document11 pagesUnion Budget 2023-24: Why in News?Adil Khan PathanNo ratings yet

- Union Budget 2016 Highlights Under 40 CharactersDocument4 pagesUnion Budget 2016 Highlights Under 40 CharactersArpit NaruNo ratings yet

- General Budget 2013-14Document7 pagesGeneral Budget 2013-14Shibraiz AneesNo ratings yet

- Key Points of The Budget For Financial Year 2012-2013Document2 pagesKey Points of The Budget For Financial Year 2012-2013anurag028No ratings yet

- Aatma Nirbhar Bharat Abhiyaan (2020) - Key Highlights RBI GR B 2020 - NABARD GR A 2020 - SEBI GR A 2020Document9 pagesAatma Nirbhar Bharat Abhiyaan (2020) - Key Highlights RBI GR B 2020 - NABARD GR A 2020 - SEBI GR A 2020avyay sudhakarNo ratings yet

- Budget 2019-20: Full HighlightsDocument11 pagesBudget 2019-20: Full Highlightsrupasree deyNo ratings yet

- Union Budget 2015-16Document15 pagesUnion Budget 2015-16InvesTrekkNo ratings yet

- Key Features of Budget 2016-2017Document15 pagesKey Features of Budget 2016-2017DikshaNo ratings yet

- Union State BudgetDocument10 pagesUnion State BudgetSrikanth KatariNo ratings yet

- S&A KS - MSME Stimulus - UpdateV7Document5 pagesS&A KS - MSME Stimulus - UpdateV7Shatir LaundaNo ratings yet

- Atmanirbhar Bharat Abhiyan: (Relief Package by Government of India)Document27 pagesAtmanirbhar Bharat Abhiyan: (Relief Package by Government of India)Ayushi SrivastavaNo ratings yet

- Law of Diminishing Manageral EconomicsDocument5 pagesLaw of Diminishing Manageral Economicsrajamech30No ratings yet

- Management and Business Finance AssignmentDocument5 pagesManagement and Business Finance Assignmentrajamech30No ratings yet

- About En19Document1 pageAbout En19ramanamurtytv7176No ratings yet

- Agent or Agency AgreementDocument8 pagesAgent or Agency AgreementMMNo ratings yet

- In Re: Michael Allen Frates Carla Jean Frates, 9th Cir. BAP (2014)Document16 pagesIn Re: Michael Allen Frates Carla Jean Frates, 9th Cir. BAP (2014)Scribd Government DocsNo ratings yet

- The Merger of American Airlines and US AirwaysDocument11 pagesThe Merger of American Airlines and US AirwaysGregNo ratings yet

- Certificate of NoticeDocument4 pagesCertificate of NoticeChapter 11 DocketsNo ratings yet

- Geokinetics Files For Chapter 11 Bankruptcy Protection, Enters Into Asset Purchase AgreementDocument1 pageGeokinetics Files For Chapter 11 Bankruptcy Protection, Enters Into Asset Purchase Agreementrenatogeo14No ratings yet

- A gmc999Document341 pagesA gmc999Brian BockNo ratings yet

- Solitude - Lockett - BOA 2-13 PDFDocument3 pagesSolitude - Lockett - BOA 2-13 PDFDarian MooreNo ratings yet

- Does FRIA Cover BanksDocument2 pagesDoes FRIA Cover BanksPing KyNo ratings yet

- Bankruptcy Law GuideDocument41 pagesBankruptcy Law GuideKhanh MiNo ratings yet

- Natalie Khawam Voluntary Chapter 7 Bankruptcy PetitionDocument53 pagesNatalie Khawam Voluntary Chapter 7 Bankruptcy PetitionStaci ZaretskyNo ratings yet

- 1 IbcDocument32 pages1 IbcChandreshNo ratings yet

- Understanding NovationDocument47 pagesUnderstanding NovationNeb GarcNo ratings yet

- Siemens AG - COMI Fertig PDFDocument8 pagesSiemens AG - COMI Fertig PDFAnna WojcieszakNo ratings yet

- Shell acted in bad faith by secretly transferring CALI creditDocument2 pagesShell acted in bad faith by secretly transferring CALI creditAudrey GuimteNo ratings yet

- Deductions from Gross EstateDocument68 pagesDeductions from Gross EstateKat Miranda100% (1)

- Lipana vs. Development Bank of The Philippines G.R. No. 73884, September 24, 1987Document1 pageLipana vs. Development Bank of The Philippines G.R. No. 73884, September 24, 1987ariel_080503No ratings yet

- ComplaintDocument170 pagesComplaintmonitorNo ratings yet

- BTM 2014 - MBA SEM IV - Chapter 01 - Introductory Concepts in BTMDocument75 pagesBTM 2014 - MBA SEM IV - Chapter 01 - Introductory Concepts in BTMKuladeepa KrNo ratings yet

- Case Study On Bhushan Steel Resolution Plan: Symbiosis Law School, Hyderabad Symbiosis International University, PUNEDocument7 pagesCase Study On Bhushan Steel Resolution Plan: Symbiosis Law School, Hyderabad Symbiosis International University, PUNERithik AanandNo ratings yet

- Co Kim Chan vs. Valdez Tan Keh GR. No. Date G.R. No. L-5 November 16, 1945 Respondent PETITIONER / Amici CuriaeDocument4 pagesCo Kim Chan vs. Valdez Tan Keh GR. No. Date G.R. No. L-5 November 16, 1945 Respondent PETITIONER / Amici CuriaeDEAN JASPERNo ratings yet

- Sample Loan With REMDocument14 pagesSample Loan With REMYcel CastroNo ratings yet

- Insolvency Law ExplainedDocument33 pagesInsolvency Law ExplainedElizar JoseNo ratings yet

- Contracts For The Sale of Motor VehicleDocument6 pagesContracts For The Sale of Motor VehiclecefuneslpezNo ratings yet

- globalCOAL SCoTADocument42 pagesglobalCOAL SCoTAzoroluffy2d10208No ratings yet

- 10000001816Document42 pages10000001816Chapter 11 DocketsNo ratings yet

- Hariharan PDFDocument10 pagesHariharan PDFHariharan ShekarNo ratings yet

- Introduction UCC What All Need To KnowDocument18 pagesIntroduction UCC What All Need To KnowI have rejoined myself with the cause by Charles W. Iseley/Isley for personal reasons. I'll follow the Sun.100% (9)

- Vetting SOPDocument29 pagesVetting SOPMashfiq SohrabNo ratings yet

- Doc. 154 - Pla MTN Def JGMT - Frank E. WildeDocument28 pagesDoc. 154 - Pla MTN Def JGMT - Frank E. WildeR. Lance FloresNo ratings yet

- Syllabus - Credit Transactions (2014)Document16 pagesSyllabus - Credit Transactions (2014)IvoryAthenaPalarcaPosposNo ratings yet

- The Power of Our Supreme Court: How Supreme Court Cases Shape DemocracyFrom EverandThe Power of Our Supreme Court: How Supreme Court Cases Shape DemocracyRating: 5 out of 5 stars5/5 (2)

- Social Anxiety and Shyness: The definitive guide to learn How to Become Self-Confident with Self-Esteem and Cognitive Behavioral Therapy. Stop Being Dominated by ShynessFrom EverandSocial Anxiety and Shyness: The definitive guide to learn How to Become Self-Confident with Self-Esteem and Cognitive Behavioral Therapy. Stop Being Dominated by ShynessRating: 5 out of 5 stars5/5 (11)

- Economics for Kids - Understanding the Basics of An Economy | Economics 101 for Children | 3rd Grade Social StudiesFrom EverandEconomics for Kids - Understanding the Basics of An Economy | Economics 101 for Children | 3rd Grade Social StudiesNo ratings yet

- Teacher Guide for Three Feathers: Exploring Healing and Justice Through Graphic Storytelling in Grades 7–12From EverandTeacher Guide for Three Feathers: Exploring Healing and Justice Through Graphic Storytelling in Grades 7–12No ratings yet

- Indigenous Storywork: Educating the Heart, Mind, Body, and SpiritFrom EverandIndigenous Storywork: Educating the Heart, Mind, Body, and SpiritNo ratings yet

- World Geography - Time & Climate Zones - Latitude, Longitude, Tropics, Meridian and More | Geography for Kids | 5th Grade Social StudiesFrom EverandWorld Geography - Time & Climate Zones - Latitude, Longitude, Tropics, Meridian and More | Geography for Kids | 5th Grade Social StudiesRating: 5 out of 5 stars5/5 (2)

- Comprehensive Peace Education: Educating for Global ResponsibilityFrom EverandComprehensive Peace Education: Educating for Global ResponsibilityNo ratings yet

- A Student's Guide to Political PhilosophyFrom EverandA Student's Guide to Political PhilosophyRating: 3.5 out of 5 stars3.5/5 (18)

- Conversation Skills: Learn How to Improve your Conversational Intelligence and Handle Fierce, Tough or Crucial Social Interactions Like a ProFrom EverandConversation Skills: Learn How to Improve your Conversational Intelligence and Handle Fierce, Tough or Crucial Social Interactions Like a ProNo ratings yet

- U.S. History Skillbook: Practice and Application of Historical Thinking Skills for AP U.S. HistoryFrom EverandU.S. History Skillbook: Practice and Application of Historical Thinking Skills for AP U.S. HistoryNo ratings yet

- World Geography Puzzles: Countries of the World, Grades 5 - 12From EverandWorld Geography Puzzles: Countries of the World, Grades 5 - 12No ratings yet