You might also like

- Electronics Repair Shop Business PlanDocument34 pagesElectronics Repair Shop Business Planummu muthiah83% (6)

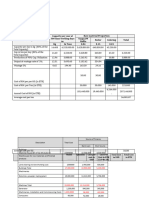

- Prestige Telephone Company (Solutions)Document4 pagesPrestige Telephone Company (Solutions)Joseph Loyola71% (7)

- Akmen AbcDocument3 pagesAkmen AbcSUKMA PUTRI GANDAARUMNo ratings yet

- Ch04 Cost Volume Profit AnalysisDocument21 pagesCh04 Cost Volume Profit AnalysisYee Sook Ying0% (1)

- Mid-Term Revision - Cost AccountingDocument32 pagesMid-Term Revision - Cost AccountingAhmed Rabea50% (2)

- F5PM Revision Question Bank - Sample - D14 J15 PDFDocument56 pagesF5PM Revision Question Bank - Sample - D14 J15 PDFKhawaja Zaid Bin Ahmed50% (2)

- High-Performance Gradient Elution: The Practical Application of the Linear-Solvent-Strength ModelFrom EverandHigh-Performance Gradient Elution: The Practical Application of the Linear-Solvent-Strength ModelNo ratings yet

- Sample Business Plan - Fargo Medical LabDocument30 pagesSample Business Plan - Fargo Medical Labtmw77589% (19)

- MFA - Assignment 2: Management and Financial Accounting - Individual Assignment 2Document9 pagesMFA - Assignment 2: Management and Financial Accounting - Individual Assignment 2Mohan sunderNo ratings yet

- Traditional Vs ABC Costing CaseDocument1 pageTraditional Vs ABC Costing Casesul239No ratings yet

- Standard Costing Example SolutionDocument2 pagesStandard Costing Example SolutionVikas KhuranaNo ratings yet

- Management and Financial Accounting-Assessment - 2 VidharshanaDocument6 pagesManagement and Financial Accounting-Assessment - 2 Vidharshanavidharshana esakkiNo ratings yet

- Solution DEC 19Document8 pagesSolution DEC 19anis izzatiNo ratings yet

- Week 4-Lecture Notes (L2)Document38 pagesWeek 4-Lecture Notes (L2)Kasmira K.Bathu GanesanNo ratings yet

- Chapter 7Document8 pagesChapter 7Erlangga DharmawangsaNo ratings yet

- Pma Test 1 2022Document6 pagesPma Test 1 2022Janielle LambertNo ratings yet

- 2014 - Quiz 3Document12 pages2014 - Quiz 3rohitmahato10No ratings yet

- Project Profile On Ball Pen InkDocument2 pagesProject Profile On Ball Pen Inksavan anvekarNo ratings yet

- CMA Garrison SuggestedSolutions Chap2Document12 pagesCMA Garrison SuggestedSolutions Chap2PIYUSH SINGHNo ratings yet

- MPP Acca Icma Model PaperDocument19 pagesMPP Acca Icma Model PaperDev RajNo ratings yet

- Part-A - Strategic Management Accounting: Multiple Choice Questions (MCQS)Document33 pagesPart-A - Strategic Management Accounting: Multiple Choice Questions (MCQS)ARIF HUSSAIN AN ENGLISH LECTURER FOR ALL CLASSESNo ratings yet

- Costing - English Answer 23.02.2022Document9 pagesCosting - English Answer 23.02.2022Shubham KuberkarNo ratings yet

- LU 3 Workbk Solutions 3.1 - 3.4Document4 pagesLU 3 Workbk Solutions 3.1 - 3.4bison3216No ratings yet

- Coursera Assgn-3 XL SheetDocument2 pagesCoursera Assgn-3 XL SheethNo ratings yet

- Management and Financial Accounting Assessment-2Document6 pagesManagement and Financial Accounting Assessment-2saranyaNo ratings yet

- Joint Products and By-ProductsDocument16 pagesJoint Products and By-ProductsAnmol AgalNo ratings yet

- Besan Manufacturing Unit PDFDocument2 pagesBesan Manufacturing Unit PDFDev MoryaNo ratings yet

- Solutions-Chapter 6Document4 pagesSolutions-Chapter 6Saurabh SinghNo ratings yet

- METU Industrial Engineering - Engineering Economy & Cost Analysis I Case StudyDocument6 pagesMETU Industrial Engineering - Engineering Economy & Cost Analysis I Case StudyOnur YılmazNo ratings yet

- References: WorksheetDocument4 pagesReferences: Worksheetsuruth242No ratings yet

- Cost SheetDocument14 pagesCost SheetSwapnil AbhishekNo ratings yet

- ROI Worksheet - MakinoDocument3 pagesROI Worksheet - MakinoBaskaranNo ratings yet

- Session 25 & 26 - Budgeting and VarianceDocument20 pagesSession 25 & 26 - Budgeting and VarianceVinay PandeyNo ratings yet

- Caf-03 Cma Artt Mock QP With SolDocument16 pagesCaf-03 Cma Artt Mock QP With Solkulhaq29No ratings yet

- SPK GENAP - Silfina WasrilDocument16 pagesSPK GENAP - Silfina WasrilnanaNo ratings yet

- Budgeted Statement ExamDocument11 pagesBudgeted Statement ExamNelz KhoNo ratings yet

- AccountingDocument9 pagesAccountingaarti saxenaNo ratings yet

- Basic STD CostingDocument5 pagesBasic STD CostingSajidZiaNo ratings yet

- Finalcosting NiyazDocument29 pagesFinalcosting Niyazakramshaikh87No ratings yet

- Accounting Assignment CardiffDocument12 pagesAccounting Assignment CardiffpavanihirushaNo ratings yet

- 5) May 2007 Cost ManagementDocument32 pages5) May 2007 Cost Managementshyammy foruNo ratings yet

- Project Profile On Chemical Etching On WoodDocument2 pagesProject Profile On Chemical Etching On Woodquraishi831No ratings yet

- Sols - Mod 9Document31 pagesSols - Mod 9Sakthivel LNo ratings yet

- ClassicPenCompany 2023B2PGPMX012 KshitijDocument3 pagesClassicPenCompany 2023B2PGPMX012 KshitijSuraj KumarNo ratings yet

- ABCQuestionsDocument4 pagesABCQuestionsAdiltufail AdilNo ratings yet

- Assignment 1: Variable CostingDocument4 pagesAssignment 1: Variable CostingWinoah HubaldeNo ratings yet

- Assignment 1: Variable CostingDocument4 pagesAssignment 1: Variable CostingWinoah HubaldeNo ratings yet

- CHAPTER # 7 EXERCISE & PROBLEMS - AnswersDocument5 pagesCHAPTER # 7 EXERCISE & PROBLEMS - AnswersZia UddinNo ratings yet

- Assignment 1: Variable CostingDocument4 pagesAssignment 1: Variable CostingWinoah HubaldeNo ratings yet

- AnswersDocument9 pagesAnswersĐào Thị Thu ThủyNo ratings yet

- Problem - ABC Vs Traditional - AnsDocument3 pagesProblem - ABC Vs Traditional - AnsAbhijit AshNo ratings yet

- MVV - Assignment 1 - ManyaDocument14 pagesMVV - Assignment 1 - ManyaManya SrivastavaNo ratings yet

- 69 Wrought Iron FurnitureDocument3 pages69 Wrought Iron FurnitureRajib StudioNo ratings yet

- Project Profile On Kurkure Type Snacks PDFDocument2 pagesProject Profile On Kurkure Type Snacks PDFSundeep Yadav100% (3)

- General Model For Variable Manufacturing Costs Variance AnalysisDocument19 pagesGeneral Model For Variable Manufacturing Costs Variance AnalysisEyuel SintayehuNo ratings yet

- Total Variance: Required: Compute The Direct Materials, Direct Labor, and Variable Manufacturing Overhead VariancesDocument20 pagesTotal Variance: Required: Compute The Direct Materials, Direct Labor, and Variable Manufacturing Overhead VariancesEyuel SintayehuNo ratings yet

- Product Cost From TraditionalDocument5 pagesProduct Cost From TraditionalPrijulNo ratings yet

- Variance IQ FileDocument34 pagesVariance IQ FileShehrozSTNo ratings yet

- Chapter 2 Homework Manufacturing Economics and Computation Exercise With SolutionDocument9 pagesChapter 2 Homework Manufacturing Economics and Computation Exercise With SolutionPhương NguyễnNo ratings yet

- Project Profile For Coco Log Making UnitDocument6 pagesProject Profile For Coco Log Making UnitRamanjaneyulu PoludasuNo ratings yet

- Question No-1-Solution Traditional Costing Method: Overhead Rate Per Machine HoursDocument3 pagesQuestion No-1-Solution Traditional Costing Method: Overhead Rate Per Machine HoursRiya SharmaNo ratings yet

- Project Profile On Production of Enriched BiodigestedDocument2 pagesProject Profile On Production of Enriched BiodigestedkhsreeharshaNo ratings yet

- AsratDocument27 pagesAsratMechal Awerka SmammoNo ratings yet

- Ama Set 37Document7 pagesAma Set 37uroojfatima21299No ratings yet

- GL Labour:: (Rs.630/42 HRS)Document12 pagesGL Labour:: (Rs.630/42 HRS)AnkitaNo ratings yet

- Noise and Signal Interference in Optical Fiber Transmission Systems: An Optimum Design ApproachFrom EverandNoise and Signal Interference in Optical Fiber Transmission Systems: An Optimum Design ApproachNo ratings yet

- Atmanirbhar Bharat AbhiyanDocument9 pagesAtmanirbhar Bharat Abhiyanrajamech30No ratings yet

- Atmanirbhar Bharat Abhiyan: (Relief Package by Government of India)Document27 pagesAtmanirbhar Bharat Abhiyan: (Relief Package by Government of India)Ayushi SrivastavaNo ratings yet

- Law of Diminishing Manageral EconomicsDocument5 pagesLaw of Diminishing Manageral Economicsrajamech30No ratings yet

- About En19Document1 pageAbout En19ramanamurtytv7176No ratings yet

- Entrepreneurship DevelopmentDocument18 pagesEntrepreneurship DevelopmentMiru JugNo ratings yet

- Nam NamDocument50 pagesNam NamDaNn UyNo ratings yet

- Project Appraisal SystemDocument75 pagesProject Appraisal Systempoo22187No ratings yet

- BFC 3227 Cost Accounting - 4Document7 pagesBFC 3227 Cost Accounting - 4karashinokov siwoNo ratings yet

- GrutzenDocument28 pagesGrutzenGhafoor MerajNo ratings yet

- Compsa - ReviewerDocument5 pagesCompsa - ReviewerCARMONA, Monique Angel DapitanNo ratings yet

- CVP Analysis Additional Exercise - SolutionsDocument17 pagesCVP Analysis Additional Exercise - Solutionsaryan bhandariNo ratings yet

- Variable Costing: A Decision-Making Perspective: True-False StatementsDocument8 pagesVariable Costing: A Decision-Making Perspective: True-False StatementsJanina Marie GarciaNo ratings yet

- 1st Choice-Marketing Plan of Tata Nano For UK MarketDocument7 pages1st Choice-Marketing Plan of Tata Nano For UK MarketLouis RNo ratings yet

- DAIBB SME Short NoteDocument12 pagesDAIBB SME Short NoteRumana AfrozNo ratings yet

- Calculus and Its ApplicationDocument12 pagesCalculus and Its ApplicationDONALD INONDANo ratings yet

- Week 3 Notes On Budgeting and Break-EvenDocument9 pagesWeek 3 Notes On Budgeting and Break-EvenEmily SroczynskiNo ratings yet

- Practical 21 PDFDocument4 pagesPractical 21 PDFchandu tidakeNo ratings yet

- Channel Selection Process and CriteriaDocument17 pagesChannel Selection Process and CriteriaAngita Kumari0% (1)

- M B A PDFDocument169 pagesM B A PDFAshwini ketkariNo ratings yet

- Short-Run Decision Making and CVP AnalysisDocument43 pagesShort-Run Decision Making and CVP AnalysisHy Tang100% (1)

- Breakeven in Units Contribuiton Margin RatioDocument11 pagesBreakeven in Units Contribuiton Margin RatioCookies And CreamNo ratings yet

- As 462Document6 pagesAs 462ziabuttNo ratings yet

- FinMan AssignmentDocument11 pagesFinMan AssignmentCzarise Krichelle Mendoza SosaNo ratings yet

- Raw Material Consumed Rs 15,000 Direct Labour Charges Rs 9,000 Machine Hours Worked 900 Machine Hours Rate 5. Units Produced 17,100Document5 pagesRaw Material Consumed Rs 15,000 Direct Labour Charges Rs 9,000 Machine Hours Worked 900 Machine Hours Rate 5. Units Produced 17,100Jagadeish jagaNo ratings yet

- U 17 18 19 20 21 Business IgcseDocument1 pageU 17 18 19 20 21 Business Igcsejosefina.delosreyesNo ratings yet

- MAT100 - MT-previous ExamDocument1 pageMAT100 - MT-previous Examclara2300181No ratings yet

- CH 8 Sales MixDocument12 pagesCH 8 Sales MixNikki Coleen SantinNo ratings yet

- Cost-Volume-Profit Analysis: Managerial Accounting 14eDocument39 pagesCost-Volume-Profit Analysis: Managerial Accounting 14ecykenNo ratings yet