You might also like

- Satish M: Corporate Finance 2: MBA 2020-22Document49 pagesSatish M: Corporate Finance 2: MBA 2020-22Keerthi PaulNo ratings yet

- PDF Soa 2329022489114 PDFDocument2 pagesPDF Soa 2329022489114 PDFCamille Victoria BacatanNo ratings yet

- 2GO Excel Calculation 1Document60 pages2GO Excel Calculation 1w_fibNo ratings yet

- The Fundamentals of Managerial Economics Answers To Questions and ProblemsDocument42 pagesThe Fundamentals of Managerial Economics Answers To Questions and Problemsrodop82No ratings yet

- 50 Alternatives To LecturingDocument5 pages50 Alternatives To LecturingAbdullateef Mohammed Ahmed AlqasemiNo ratings yet

- Affidavit of 2 Disinterested NestoramorinDocument2 pagesAffidavit of 2 Disinterested NestoramorinAlfie OmegaNo ratings yet

- Business CommunicationDocument288 pagesBusiness Communicationprof.titirNo ratings yet

- Lesson Plan Sample For IGCSEDocument2 pagesLesson Plan Sample For IGCSEIftita Selviana81% (21)

- BP Case StudyDocument12 pagesBP Case Studypyush0786No ratings yet

- C++ Lab PracticeDocument10 pagesC++ Lab PracticeDevendra patidar0% (1)

- Arn32097 Atp - 3 34.22 000 Web 1Document138 pagesArn32097 Atp - 3 34.22 000 Web 1darkghostcNo ratings yet

- EVBN Report Retail Final Report - CompressedDocument52 pagesEVBN Report Retail Final Report - CompressedK57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Sop MSC in Cyber SecurityDocument2 pagesSop MSC in Cyber SecurityMohammad Mannan40% (5)

- Premium Calculator: Select PeriodDocument5 pagesPremium Calculator: Select PeriodDeep DkNo ratings yet

- Cimigo Navigating Vietnams Economic Recovery Post Covid 10-10-21 Wdjw7mDocument20 pagesCimigo Navigating Vietnams Economic Recovery Post Covid 10-10-21 Wdjw7mBaty NeNo ratings yet

- Strategyand Where Next RetailDocument14 pagesStrategyand Where Next RetailMiguel R MoNo ratings yet

- P60 End of Year Certificate: Tax Year To 5 AprilDocument1 pageP60 End of Year Certificate: Tax Year To 5 Apriladrianhooo89No ratings yet

- Deutsche Bank - Maximum Containment, Social Distancing and The Economics of Stoppage 12 Unexpected Market and Economic Themes Defining 2020Document88 pagesDeutsche Bank - Maximum Containment, Social Distancing and The Economics of Stoppage 12 Unexpected Market and Economic Themes Defining 2020AryttNo ratings yet

- Itapp FinalsDocument4 pagesItapp FinalsKenneth TallmanNo ratings yet

- Revenue Dashboard Wireframe v0.3Document13 pagesRevenue Dashboard Wireframe v0.3koddati nithishNo ratings yet

- AFM Mini Exam - SolutionDocument6 pagesAFM Mini Exam - SolutionHamid KhanNo ratings yet

- M-And-S Ar20 Full 200528Document204 pagesM-And-S Ar20 Full 200528ReswinNo ratings yet

- Insurance Premium Calculator 2015 16Document3 pagesInsurance Premium Calculator 2015 16Esteban HernándezNo ratings yet

- DashboardDocument2 pagesDashboardJagoda CzarneckaNo ratings yet

- FRA AssignmentDocument12 pagesFRA AssignmentsomechnitjNo ratings yet

- Rep Leger Jan2024EconConf 12jan2024 AB FINALDocument18 pagesRep Leger Jan2024EconConf 12jan2024 AB FINALCTV Calgary DigitalNo ratings yet

- ECO PPT Team 6Document10 pagesECO PPT Team 6Darshan Changole PCMNo ratings yet

- Mesa Redonda McKinsey I O Novo Consumidor pós-COVID (Winning The Recovery)Document31 pagesMesa Redonda McKinsey I O Novo Consumidor pós-COVID (Winning The Recovery)Aurizio FreitasNo ratings yet

- The US Outlook: Growth, With Malaise: Michael FeroliDocument46 pagesThe US Outlook: Growth, With Malaise: Michael Ferolidov_zigler2891No ratings yet

- Monthly BudgetDocument1 pageMonthly Budgetapi-395772866No ratings yet

- QC Case StudyDocument6 pagesQC Case StudyHarines WaranNo ratings yet

- Adobe Scan Sep 22, 2023Document4 pagesAdobe Scan Sep 22, 2023romykumar5678No ratings yet

- Life Insurance - Team Shivang ShahDocument12 pagesLife Insurance - Team Shivang ShahSiddharth BhattNo ratings yet

- r20 Strategic-ReportDocument44 pagesr20 Strategic-ReportAlice AliceNo ratings yet

- Energy Companies & Mid-Cycle Profitability: Benchmarking Industry Supply CostsDocument12 pagesEnergy Companies & Mid-Cycle Profitability: Benchmarking Industry Supply CostsForexliveNo ratings yet

- Financial Measures: (Amazon, 2021)Document6 pagesFinancial Measures: (Amazon, 2021)najeeb shajudheenNo ratings yet

- Region: - IV-B MIMAROPA - : MFO 1-A and MFO 1-B - Public Pre-ElementaryDocument1 pageRegion: - IV-B MIMAROPA - : MFO 1-A and MFO 1-B - Public Pre-ElementaryLuzviminda T. TredesNo ratings yet

- The Agony & The Ecstasy 2021Document24 pagesThe Agony & The Ecstasy 2021KimNo ratings yet

- New Normal - Manufacturing - SGS Business RestartDocument13 pagesNew Normal - Manufacturing - SGS Business RestartGolayootNo ratings yet

- Quick / Rapid Fire Batteries Case StudyDocument15 pagesQuick / Rapid Fire Batteries Case StudyMd ShahidullahNo ratings yet

- 4Q 2019 - Quarterly Industry Outlook - MalaysiaDocument91 pages4Q 2019 - Quarterly Industry Outlook - MalaysiaGuan JooNo ratings yet

- What Is SANFDocument17 pagesWhat Is SANFAbizawinnerNo ratings yet

- Model Content: Input Capital Schedules Capital Expenditures & Depreciation Operational Expenses Revenue CalculationDocument41 pagesModel Content: Input Capital Schedules Capital Expenditures & Depreciation Operational Expenses Revenue Calculationavinash singhNo ratings yet

- COVID 19 Outlook For Airlines' Cash BurnDocument12 pagesCOVID 19 Outlook For Airlines' Cash BurnTatiana RokouNo ratings yet

- Income Tax Deductions List - Deductions On Section 80C, 80CCC, 80CCD and 80D - FY 2022-23 (AY 2023-24) - Tax2winDocument26 pagesIncome Tax Deductions List - Deductions On Section 80C, 80CCC, 80CCD and 80D - FY 2022-23 (AY 2023-24) - Tax2winJaydeep DasadiyaNo ratings yet

- Drinking Milk Products in Vietnam ContextDocument2 pagesDrinking Milk Products in Vietnam ContextÂn THiênNo ratings yet

- Class 7Document64 pagesClass 7Христина ЯблоньNo ratings yet

- Inflation: The Macroeconomic EnvironmentDocument1 pageInflation: The Macroeconomic EnvironmentMinhh KhanggNo ratings yet

- Payslip TemplateDocument7 pagesPayslip TemplateAlyani MineNo ratings yet

- Jan. 8, 2024, Presentation To Caddo School Board's Insurance and Finance CommitteeDocument26 pagesJan. 8, 2024, Presentation To Caddo School Board's Insurance and Finance CommitteeCurtis HeyenNo ratings yet

- On FMCG Players ComparisonDocument14 pagesOn FMCG Players ComparisonSHIKHA DWIVEDINo ratings yet

- AFM211 Canada Goose Case Presentation Final (Autosaved)Document26 pagesAFM211 Canada Goose Case Presentation Final (Autosaved)Alice SongNo ratings yet

- Triple-I Update Economic Briefing: Covid-19 Impact On PC Insurance Market: Business Interruption and PandemicsDocument19 pagesTriple-I Update Economic Briefing: Covid-19 Impact On PC Insurance Market: Business Interruption and PandemicsBipra biswasNo ratings yet

- MAS - PreweekDocument32 pagesMAS - PreweekAzureBlazeNo ratings yet

- 2020 Budget ProposalDocument1 page2020 Budget ProposalFortune Nwachukwu OnweNo ratings yet

- ECON F211 POE - Comprehensive Examination 10th December 2020 at 9 - 00 AmDocument9 pagesECON F211 POE - Comprehensive Examination 10th December 2020 at 9 - 00 AmVedant Chinmaya KhandelwalNo ratings yet

- How To Price-And Sell-In A Pandemic: by Matt Kropp and Phillip AndersenDocument4 pagesHow To Price-And Sell-In A Pandemic: by Matt Kropp and Phillip AndersenViren DeshpandeNo ratings yet

- MEM June 2020 - PPT - 2Document21 pagesMEM June 2020 - PPT - 2Kyaw SithuNo ratings yet

- ConsumerConfidence Apr2009Document1 pageConsumerConfidence Apr2009zezorroNo ratings yet

- FRSHTRP StockReport 20231122 2111Document12 pagesFRSHTRP StockReport 20231122 2111SiddharthNo ratings yet

- Leverage Ratio FIN420 2023Document7 pagesLeverage Ratio FIN420 20232023466162No ratings yet

- An Empirical Study On Financial Risks in Agriculture Sector of BangladeshDocument18 pagesAn Empirical Study On Financial Risks in Agriculture Sector of BangladeshJahangir AlomNo ratings yet

- Auto Post COVID-19 - 052920 - tcm9-249607Document10 pagesAuto Post COVID-19 - 052920 - tcm9-249607Bidyut Bhusan PandaNo ratings yet

- Thesis DefenseDocument17 pagesThesis DefenseJumar RanasNo ratings yet

- The Effect of Sales Promotion and Knowledge On Impulsive Buying of Online Platform ConsumersDocument15 pagesThe Effect of Sales Promotion and Knowledge On Impulsive Buying of Online Platform ConsumersK57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- 3685-Article Text-6899-1-10-20210423Document9 pages3685-Article Text-6899-1-10-20210423K57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Eps2004045org 9058920712 MulderDocument262 pagesEps2004045org 9058920712 MulderK57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Vietnam Internet Resources 2013: Report OnDocument38 pagesVietnam Internet Resources 2013: Report OnK57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Market Pulse Q4 Report - Nielsen Viet Nam: Prepared by Nielsen Vietnam February 2017Document8 pagesMarket Pulse Q4 Report - Nielsen Viet Nam: Prepared by Nielsen Vietnam February 2017K57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- What If I Find It Cheaper Someplace ElseDocument18 pagesWhat If I Find It Cheaper Someplace ElseK57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Study On Online Purchase Decisions On The Online Shopee Selling SiteDocument7 pagesStudy On Online Purchase Decisions On The Online Shopee Selling SiteK57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Impact of Sales Promotion On Consumer Impulse Purchases in Karachi, PakistanDocument32 pagesImpact of Sales Promotion On Consumer Impulse Purchases in Karachi, PakistanK57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- The Consequences of Doing Nothing Inaction InertiaDocument11 pagesThe Consequences of Doing Nothing Inaction InertiaK57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Nielsen Traditional Trade Report FINALDocument20 pagesNielsen Traditional Trade Report FINALK57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Retail Foods Hanoi Vietnam 3-7-2017Document30 pagesRetail Foods Hanoi Vietnam 3-7-2017K57.CTTT BUI NGUYEN HUONG LYNo ratings yet

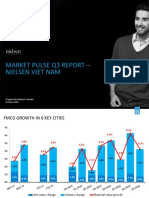

- Nielsen Market Pulse Q3 2017Document2 pagesNielsen Market Pulse Q3 2017K57.CTTT BUI NGUYEN HUONG LYNo ratings yet

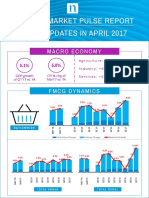

- Agriculture: +2.0% Industry: +4.2% Services: +6.5%: Unit Value Change Volume Change Nominal GrowthDocument2 pagesAgriculture: +2.0% Industry: +4.2% Services: +6.5%: Unit Value Change Volume Change Nominal GrowthK57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Nielsen Market Pulse Q3 2016Document8 pagesNielsen Market Pulse Q3 2016K57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Nielsen Market Pulse Q2 2018Document6 pagesNielsen Market Pulse Q2 2018K57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Academic vs. Professional WritingDocument28 pagesAcademic vs. Professional WritingEmelou Lisbo DumasNo ratings yet

- KITSEN IF Fastform Slab Formworks SolutionDocument15 pagesKITSEN IF Fastform Slab Formworks SolutionLuis Gustavo Rodrigues PereiraNo ratings yet

- Es S.C Om: Exclusive Computer Mcqs For Ibps RRB Po/Clerk MainDocument40 pagesEs S.C Om: Exclusive Computer Mcqs For Ibps RRB Po/Clerk MainSidharth SharmaNo ratings yet

- Essay PDFDocument8 pagesEssay PDFbcarthel169No ratings yet

- Ngọc 31201022522 - Nguyễn Phan Bảo: Câu HỏiDocument4 pagesNgọc 31201022522 - Nguyễn Phan Bảo: Câu HỏiNGỌC NGUYỄN PHAN BẢONo ratings yet

- Navi NeethuDocument3 pagesNavi NeethuNeethu AppireddygariNo ratings yet

- Public Debt 2014eDocument73 pagesPublic Debt 2014elankaCnewsNo ratings yet

- Gaurav Sharma: Curriculum VitaeDocument2 pagesGaurav Sharma: Curriculum Vitaejassi7nishadNo ratings yet

- UTI Asset Management Company Limited - DRHP - 20191223130106Document393 pagesUTI Asset Management Company Limited - DRHP - 20191223130106SubscriptionNo ratings yet

- Outline Dimensions and Main ParametersDocument9 pagesOutline Dimensions and Main ParametersdovaleramosNo ratings yet

- M.K.Bhavnagar Univesity Department of EnglishDocument22 pagesM.K.Bhavnagar Univesity Department of EnglishKB BalochNo ratings yet

- Network Monitor - Get PasswordDocument2 pagesNetwork Monitor - Get PasswordCodeModeNo ratings yet

- Reso - Grant of Assistance To TyphoonDocument2 pagesReso - Grant of Assistance To TyphoonMario Roldan Jr.No ratings yet

- Research Project Furniture Showroom.Document12 pagesResearch Project Furniture Showroom.kit katNo ratings yet

- Oct 07th Kingfoodmart Pitching DeckDocument22 pagesOct 07th Kingfoodmart Pitching DeckQuynh Anh Dang NuNo ratings yet

- ShtrigaDocument2 pagesShtrigaStanislavNo ratings yet

- World Cup of Hockey Marketing PlanDocument26 pagesWorld Cup of Hockey Marketing Planapi-394353406No ratings yet

- Study Material Dialogue Writing 2022 2Document3 pagesStudy Material Dialogue Writing 2022 2ghghghgNo ratings yet

- Career Path EssayDocument2 pagesCareer Path Essayapi-481729188No ratings yet

- Compilation of Tools, Equipments and Materials: Use in Fashion Accessories in The PhilippinesDocument44 pagesCompilation of Tools, Equipments and Materials: Use in Fashion Accessories in The PhilippinesAizel Nova Fermilan ArañezNo ratings yet

- NDRI Technology Booklet 21 2022Document124 pagesNDRI Technology Booklet 21 2022GurdeepNo ratings yet

- Study Materials: Vedantu Innovations Pvt. Ltd. Score High With A Personal Teacher, Learn LIVE Online!Document73 pagesStudy Materials: Vedantu Innovations Pvt. Ltd. Score High With A Personal Teacher, Learn LIVE Online!MansiNo ratings yet

- Sinking Fund BondsDocument8 pagesSinking Fund BondsKunal MaheshwariNo ratings yet