You might also like

- Dec 15 TuesThurs GradesDocument7 pagesDec 15 TuesThurs GradescsschwarNo ratings yet

- Dec 8 MonWed GradesDocument3 pagesDec 8 MonWed GradescsschwarNo ratings yet

- Dec 12 Tues ThursDocument5 pagesDec 12 Tues ThurscsschwarNo ratings yet

- Tata AIA Life Insurance Sampoorna Raksha Supreme Policy Term TableDocument2 pagesTata AIA Life Insurance Sampoorna Raksha Supreme Policy Term TableAkshay PatilNo ratings yet

- Dec 10 TuesThurs GradesDocument6 pagesDec 10 TuesThurs GradescsschwarNo ratings yet

- Dec 9 MonWed GradesDocument3 pagesDec 9 MonWed GradescsschwarNo ratings yet

- Dec 9 TuesThurs GradesDocument6 pagesDec 9 TuesThurs GradescsschwarNo ratings yet

- Dec 13 MonWed GradesDocument3 pagesDec 13 MonWed GradescsschwarNo ratings yet

- Dec 10 MonWed GradesDocument3 pagesDec 10 MonWed GradescsschwarNo ratings yet

- Tues Thurs GradesDocument12 pagesTues Thurs GradescsschwarNo ratings yet

- Bulan JAN PEB MAR APR MEI JUN JUL AGS Poliklini KDocument2 pagesBulan JAN PEB MAR APR MEI JUN JUL AGS Poliklini KAnonymous q3YIPgmNo ratings yet

- Dec 15 MonWed GradesDocument4 pagesDec 15 MonWed GradescsschwarNo ratings yet

- Cuci Tangan Semester 2 2018Document1 pageCuci Tangan Semester 2 2018NopiNo ratings yet

- Reporte General 6-2Document2 pagesReporte General 6-2Eliodoro Pernet UbarneNo ratings yet

- Life Income Option - Limited PayDocument2 pagesLife Income Option - Limited PayAkshay PatilNo ratings yet

- Production Line Performance ReportDocument4 pagesProduction Line Performance ReportDISEÑO DigitalNo ratings yet

- Users 254878 Active 165479 Active % 65%Document5 pagesUsers 254878 Active 165479 Active % 65%risenalNo ratings yet

- Flamingo Fashions Limited (Lingerie) : C&A Efficiency Report March 2020Document2 pagesFlamingo Fashions Limited (Lingerie) : C&A Efficiency Report March 2020monowaraNo ratings yet

- Waffle Chart 1Document5 pagesWaffle Chart 1risenalNo ratings yet

- Num. de Orden Mat. Prom. Mat. Asist. Soc. Prom. Leng - ESP. Prom. Leng - Esp. Asist. Naturales Prom. Naturales AsistDocument1 pageNum. de Orden Mat. Prom. Mat. Asist. Soc. Prom. Leng - ESP. Prom. Leng - Esp. Asist. Naturales Prom. Naturales Asistargenis de la cruzNo ratings yet

- FYs 2009 2018 Preliminary LGUs Internal Revenue Allotment IRA Dependency Data by MunicipalityDocument118 pagesFYs 2009 2018 Preliminary LGUs Internal Revenue Allotment IRA Dependency Data by MunicipalityKent Elmann CadalinNo ratings yet

- JAN FEB MAR APR MEI JUN JUL AGS SEP OKT NOV DES: NO Nama Desa/Kelurahan Jumlah Penduduk Jumlah Pus Jumlah KB Aktif % KETDocument3 pagesJAN FEB MAR APR MEI JUN JUL AGS SEP OKT NOV DES: NO Nama Desa/Kelurahan Jumlah Penduduk Jumlah Pus Jumlah KB Aktif % KETRidha Dwi Adi NovitasariNo ratings yet

- Hasil Capaian Monitoring Indik Mutu RTM 1Document28 pagesHasil Capaian Monitoring Indik Mutu RTM 1syaiful100% (1)

- Reporte de Avance Global Reductores y Bombas 12 Al 13 Nov. 2017Document6 pagesReporte de Avance Global Reductores y Bombas 12 Al 13 Nov. 2017Alejandro LopezNo ratings yet

- HG CertificateDocument2 pagesHG CertificateAkshay PatilNo ratings yet

- Kpi 040716Document1 pageKpi 040716GENNY ESPAÑANo ratings yet

- Rumus AbsensiDocument1 pageRumus AbsensiNur AzizahNo ratings yet

- Análisis Esp 2017 ZONA 04Document8 pagesAnálisis Esp 2017 ZONA 04Edgar AlcántaraNo ratings yet

- Hasil Monitoring Kepatuhan Pemakaian Apd Semester Ii Tahun 2018Document1 pageHasil Monitoring Kepatuhan Pemakaian Apd Semester Ii Tahun 2018NopiNo ratings yet

- Porcentaje de Ocupacion Hospitalaria 26 Junio 2023Document1 pagePorcentaje de Ocupacion Hospitalaria 26 Junio 2023Ashley CastañedaNo ratings yet

- Notas Sistemas EléctricosDocument4 pagesNotas Sistemas Eléctricosmaxitolol37No ratings yet

- 3.3.3 Ejercicio 2 EstadisticaDocument16 pages3.3.3 Ejercicio 2 Estadisticaleidy agudeloNo ratings yet

- Cálculo de Áreas: R - I R - Ii R - IiiDocument2 pagesCálculo de Áreas: R - I R - Ii R - IiiJose pedro Muñoz cespdesNo ratings yet

- SKP 4 Surgical CheklistDocument12 pagesSKP 4 Surgical Cheklistfajar obreindNo ratings yet

- Peratus Kehadiran MuridDocument9 pagesPeratus Kehadiran MuridSandhrigah KrishnanNo ratings yet

- Updated Incentives Plan - Sheet1Document1 pageUpdated Incentives Plan - Sheet1Shashank RaiNo ratings yet

- 06 - Uas Pai - Ida Ayu Made Dwi PuspitaDocument7 pages06 - Uas Pai - Ida Ayu Made Dwi PuspitaGus TutNo ratings yet

- Diablo 2 Experience ChartDocument6 pagesDiablo 2 Experience ChartStuartNo ratings yet

- Summary PA, DOWN TIME Unit Hyundai, Tonly, Dynapac 2023Document6 pagesSummary PA, DOWN TIME Unit Hyundai, Tonly, Dynapac 2023samsudinnor winataNo ratings yet

- 500 MtrrowmalefemaleDocument3 pages500 MtrrowmalefemaleABNo ratings yet

- Presentasi Management PTIDocument9 pagesPresentasi Management PTIdendy pratamaNo ratings yet

- EfectividadDocument1 pageEfectividadjoseNo ratings yet

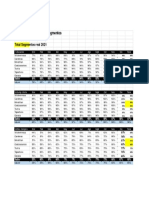

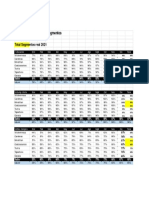

- Reporte de Indicadores por Segmentos 2021Document1 pageReporte de Indicadores por Segmentos 2021joseNo ratings yet

- Lesson 02Document34 pagesLesson 02ROHIT SAININo ratings yet

- UntitledDocument4,843 pagesUntitledSwapnil YamgarNo ratings yet

- Transmutation TableDocument3 pagesTransmutation TableAnjillyn Mae Cruz PerezNo ratings yet

- The XL Academy Excel Percentage Data AnalysisDocument7 pagesThe XL Academy Excel Percentage Data AnalysisROHIT SAININo ratings yet

- RP DBem RDocument112 pagesRP DBem RGiadira Vasquez FollegatiNo ratings yet

- Transmutation Table: Number of Test Items Raw 55 60 65 70 75 80 85 90 95 100 ScoreDocument4 pagesTransmutation Table: Number of Test Items Raw 55 60 65 70 75 80 85 90 95 100 ScoreGrace TaburnalNo ratings yet

- Heat MapDocument11 pagesHeat MapAhlex Van der AllNo ratings yet

- Symbol Roll Over 10/27/2016Document32 pagesSymbol Roll Over 10/27/2016Huge EarnNo ratings yet

- Transmutation table gradesDocument2 pagesTransmutation table gradesCharlie Manahan TemonNo ratings yet

- IRS Allotment Dependency by Philippine Province 2009-2018Document10 pagesIRS Allotment Dependency by Philippine Province 2009-2018Rheii EstandarteNo ratings yet

- Analysis of December 2019 performanceDocument1 pageAnalysis of December 2019 performanceLuis CastilloNo ratings yet

- Copia de INFORME GENERAL VA. AGREGADO 2021 AL 07-04-2022Document70 pagesCopia de INFORME GENERAL VA. AGREGADO 2021 AL 07-04-2022Kevin BohórquezNo ratings yet

- Nilai Bahasa IndonesiaDocument17 pagesNilai Bahasa Indonesiarinawati721No ratings yet

- New TransmutedDocument33 pagesNew TransmutedSenry ScentNo ratings yet

- Cuadro de Porcentajes de Descuento de ColegiaturaDocument211 pagesCuadro de Porcentajes de Descuento de ColegiaturaUnidad Educativa Particular LatinoamericanoNo ratings yet

- Social Security Break Even CalculatorDocument50 pagesSocial Security Break Even Calculatormasum mahdyNo ratings yet

- Lead Scoring Subjective QuestionsDocument3 pagesLead Scoring Subjective QuestionsAkshay PatilNo ratings yet

- Lead Scoring Assignment SummaryDocument4 pagesLead Scoring Assignment SummaryAkshay PatilNo ratings yet

- Lead Scoring Case StudyDocument14 pagesLead Scoring Case StudyAkshay PatilNo ratings yet

- CLAIM DOCUMENT LISTDocument2 pagesCLAIM DOCUMENT LISTAkshay PatilNo ratings yet

- CTL CertificateDocument2 pagesCTL CertificateAkshay PatilNo ratings yet

- HG CertificateDocument2 pagesHG CertificateAkshay PatilNo ratings yet

- CLAIM DOCUMENT LISTDocument2 pagesCLAIM DOCUMENT LISTAkshay PatilNo ratings yet

- Lead Scoring Case Study PresentationDocument16 pagesLead Scoring Case Study PresentationAkshay PatilNo ratings yet

- PLG CertificateDocument2 pagesPLG CertificateAkshay PatilNo ratings yet

- CTL CertificateDocument2 pagesCTL CertificateAkshay PatilNo ratings yet

- Honda CertificateDocument2 pagesHonda CertificateAkshay PatilNo ratings yet

- Guaranteed Surrender Value Factors: Life Plus Plan Option - Single PayDocument2 pagesGuaranteed Surrender Value Factors: Life Plus Plan Option - Single PayAkshay PatilNo ratings yet

- HG CertificateDocument2 pagesHG CertificateAkshay PatilNo ratings yet

- Policy Years/Term 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70Document3 pagesPolicy Years/Term 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70Akshay PatilNo ratings yet

- Honda CertificateDocument2 pagesHonda CertificateAkshay PatilNo ratings yet

- Honda CertificateDocument2 pagesHonda CertificateAkshay PatilNo ratings yet

- MG CertificateDocument2 pagesMG CertificateAkshay PatilNo ratings yet

- Life Income Option - Limited PayDocument2 pagesLife Income Option - Limited PayAkshay PatilNo ratings yet

- PLG CertificateDocument2 pagesPLG CertificateAkshay PatilNo ratings yet

- TATA AIA LIFE SAMPOORNA RAKSHA SUPREME, Non-Linked, Non-Participating Individual Life Insurance PlanDocument73 pagesTATA AIA LIFE SAMPOORNA RAKSHA SUPREME, Non-Linked, Non-Participating Individual Life Insurance PlanAkshay PatilNo ratings yet

- Tata AIA Life Insurance Sampoorna Raksha Supreme (UIN: 110N160V02) - IRDA of India Regn No. 110Document3 pagesTata AIA Life Insurance Sampoorna Raksha Supreme (UIN: 110N160V02) - IRDA of India Regn No. 110Akshay PatilNo ratings yet

- HG CertificateDocument2 pagesHG CertificateAkshay PatilNo ratings yet

- Part E 6. Part F: Tata AIA Life Insurance Sampoorna Raksha Supreme (UIN: 110N160V02) - IRDA of India Regn No. 110Document3 pagesPart E 6. Part F: Tata AIA Life Insurance Sampoorna Raksha Supreme (UIN: 110N160V02) - IRDA of India Regn No. 110Akshay PatilNo ratings yet

- Mediclaim Policy Premium ReceiptsDocument4 pagesMediclaim Policy Premium ReceiptsAkshay PatilNo ratings yet

- Mediclaim Policy Premium ReceiptsDocument4 pagesMediclaim Policy Premium ReceiptsAkshay PatilNo ratings yet

- Mediclaim Policy Premium ReceiptsDocument4 pagesMediclaim Policy Premium ReceiptsAkshay PatilNo ratings yet

- Part E 6. Part F: Tata AIA Life Insurance Sampoorna Raksha Supreme (UIN: 110N160V02) - IRDA of India Regn No. 110Document3 pagesPart E 6. Part F: Tata AIA Life Insurance Sampoorna Raksha Supreme (UIN: 110N160V02) - IRDA of India Regn No. 110Akshay PatilNo ratings yet

- Wall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementFrom EverandWall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementRating: 4.5 out of 5 stars4.5/5 (20)

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingFrom EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingRating: 4.5 out of 5 stars4.5/5 (97)

- AI For Lawyers: How Artificial Intelligence is Adding Value, Amplifying Expertise, and Transforming CareersFrom EverandAI For Lawyers: How Artificial Intelligence is Adding Value, Amplifying Expertise, and Transforming CareersNo ratings yet

- Learn the Essentials of Business Law in 15 DaysFrom EverandLearn the Essentials of Business Law in 15 DaysRating: 4 out of 5 stars4/5 (13)

- IFRS 9 and CECL Credit Risk Modelling and Validation: A Practical Guide with Examples Worked in R and SASFrom EverandIFRS 9 and CECL Credit Risk Modelling and Validation: A Practical Guide with Examples Worked in R and SASRating: 3 out of 5 stars3/5 (5)

- Buffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorFrom EverandBuffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorRating: 4.5 out of 5 stars4.5/5 (132)

- How to Win a Merchant Dispute or Fraudulent Chargeback CaseFrom EverandHow to Win a Merchant Dispute or Fraudulent Chargeback CaseNo ratings yet

- The Business Legal Lifecycle US Edition: How To Successfully Navigate Your Way From Start Up To SuccessFrom EverandThe Business Legal Lifecycle US Edition: How To Successfully Navigate Your Way From Start Up To SuccessNo ratings yet

- Getting Through: Cold Calling Techniques To Get Your Foot In The DoorFrom EverandGetting Through: Cold Calling Techniques To Get Your Foot In The DoorRating: 4.5 out of 5 stars4.5/5 (63)

- Introduction to Negotiable Instruments: As per Indian LawsFrom EverandIntroduction to Negotiable Instruments: As per Indian LawsRating: 5 out of 5 stars5/5 (1)

- Disloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpFrom EverandDisloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpRating: 4 out of 5 stars4/5 (214)

- The Shareholder Value Myth: How Putting Shareholders First Harms Investors, Corporations, and the PublicFrom EverandThe Shareholder Value Myth: How Putting Shareholders First Harms Investors, Corporations, and the PublicRating: 5 out of 5 stars5/5 (1)

- Competition and Antitrust Law: A Very Short IntroductionFrom EverandCompetition and Antitrust Law: A Very Short IntroductionRating: 5 out of 5 stars5/5 (3)

- The Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesWhite Collar CriminalsFrom EverandThe Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesWhite Collar CriminalsRating: 5 out of 5 stars5/5 (24)

- Indian Polity with Indian Constitution & Parliamentary AffairsFrom EverandIndian Polity with Indian Constitution & Parliamentary AffairsNo ratings yet

- California Employment Law: An Employer's Guide: Revised and Updated for 2024From EverandCalifornia Employment Law: An Employer's Guide: Revised and Updated for 2024No ratings yet

- The Real Estate Investing Diet: Harnessing Health Strategies to Build Wealth in Ninety DaysFrom EverandThe Real Estate Investing Diet: Harnessing Health Strategies to Build Wealth in Ninety DaysNo ratings yet

- LLC: LLC Quick start guide - A beginner's guide to Limited liability companies, and starting a businessFrom EverandLLC: LLC Quick start guide - A beginner's guide to Limited liability companies, and starting a businessRating: 5 out of 5 stars5/5 (1)