You might also like

- Provincial Facilitation for Investment and Trade Index: Measuring Economic Governance for Business Development in the Lao People’s Democratic Republic-Second EditionFrom EverandProvincial Facilitation for Investment and Trade Index: Measuring Economic Governance for Business Development in the Lao People’s Democratic Republic-Second EditionNo ratings yet

- Jurnal Gordev Desmila Reny Sofyan Sinta 4Document14 pagesJurnal Gordev Desmila Reny Sofyan Sinta 4Pras BrisyariahNo ratings yet

- Economic Indicators for East Asia: Input–Output TablesFrom EverandEconomic Indicators for East Asia: Input–Output TablesNo ratings yet

- Financials Infosys Last 5 Years Annual Revenue History and Growth RateDocument7 pagesFinancials Infosys Last 5 Years Annual Revenue History and Growth RateDivyavadan MateNo ratings yet

- Artikel Durrotussilfi PurwokertoDocument14 pagesArtikel Durrotussilfi Purwokertozxxx38000No ratings yet

- 2416-Article Text-7007-1-10-20230112Document15 pages2416-Article Text-7007-1-10-20230112Cakra WicaksonoNo ratings yet

- The Influence of Liquidity and Activities On Company Profitability and Value (Study On Hotel Companies Listed On Indonesia Stock Exchange)Document7 pagesThe Influence of Liquidity and Activities On Company Profitability and Value (Study On Hotel Companies Listed On Indonesia Stock Exchange)International Journal of Innovative Science and Research TechnologyNo ratings yet

- India Russia Economic RelationsDocument6 pagesIndia Russia Economic RelationsFazakh parvaizNo ratings yet

- Ijmss: Keywords: Balance Sheet, Profit and Loss Account, Financial RatiosDocument7 pagesIjmss: Keywords: Balance Sheet, Profit and Loss Account, Financial RatiosAbhimanyu Narayan RaiNo ratings yet

- EJMCM - Volume 7 - Issue 8 - Pages 5089-5094Document6 pagesEJMCM - Volume 7 - Issue 8 - Pages 5089-5094dominic wurdaNo ratings yet

- Team RD-3 Banking & FinanceDocument21 pagesTeam RD-3 Banking & FinancesukeshNo ratings yet

- Dividend PolicyDocument14 pagesDividend PolicyMuhammad Sofyan SyahrirNo ratings yet

- The Effect of Audit Commitee, Liquidity, Profitability, and Leverage On Dividend Policy in Consumer Goods Sector Companies Listed On The Indonesian Stock ExchangeDocument9 pagesThe Effect of Audit Commitee, Liquidity, Profitability, and Leverage On Dividend Policy in Consumer Goods Sector Companies Listed On The Indonesian Stock ExchangeInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Paper PDFDocument9 pagesPaper PDFJai patelNo ratings yet

- IJCRT22A6682Document7 pagesIJCRT22A6682shashikumarb2277No ratings yet

- Size of IT Industry in IndiaDocument10 pagesSize of IT Industry in IndiaSachin KukrejaNo ratings yet

- An Analytical Study On Financial Performance of The ICICI BankDocument4 pagesAn Analytical Study On Financial Performance of The ICICI Bankvidhya vijayanNo ratings yet

- 11 Chapter 3Document47 pages11 Chapter 3lakshman doregolNo ratings yet

- 532 Venture Capital in IndiaDocument22 pages532 Venture Capital in Indiaravi lokareNo ratings yet

- Effect of Results and Inflation On Third Party FunDocument9 pagesEffect of Results and Inflation On Third Party FunBella CapriceNo ratings yet

- ICICI Securities IPO NoteDocument7 pagesICICI Securities IPO NoteKrishna GoyalNo ratings yet

- Armageddon Final Case: Fintech - UPI Payment SolutionsDocument6 pagesArmageddon Final Case: Fintech - UPI Payment SolutionsHimanshu SoniNo ratings yet

- Sapm Term Papr-GyanendraDocument51 pagesSapm Term Papr-GyanendraiamgyanuNo ratings yet

- Annual Report of ITC 2021 UDocument33 pagesAnnual Report of ITC 2021 UAkash Tewari Student, Jaipuria LucknowNo ratings yet

- Comparative Analysis of Financial Performance Before and During The Covid-19 Pandemic at BTPN SyariahDocument16 pagesComparative Analysis of Financial Performance Before and During The Covid-19 Pandemic at BTPN SyariahdesmyNo ratings yet

- Financial Services - Sector ReportDocument13 pagesFinancial Services - Sector ReportRajendra BhoirNo ratings yet

- 939pm - 55.EPRA JOURNALS 13951Document4 pages939pm - 55.EPRA JOURNALS 13951Mani kandan.GNo ratings yet

- UntitledDocument13 pagesUntitledAbdul Jaihudin AnwarNo ratings yet

- Financial Performance of Pt. Adhi Karya (Persero) 2015-2020 Based On Kep-Men BumnDocument16 pagesFinancial Performance of Pt. Adhi Karya (Persero) 2015-2020 Based On Kep-Men BumnArif ImamNo ratings yet

- Analysis of The Effect of Stock Prices On Coal SubDocument12 pagesAnalysis of The Effect of Stock Prices On Coal Subtejaguggilam20No ratings yet

- 31 (2) Sbi and IciciDocument6 pages31 (2) Sbi and IciciShyla PascalNo ratings yet

- IDirect Brokerage SectorUpdate Mar23Document10 pagesIDirect Brokerage SectorUpdate Mar23akshaybendal6343No ratings yet

- Wahyu Leman Publikasi Nasional IndonesiaDocument20 pagesWahyu Leman Publikasi Nasional Indonesiaebingsuherdi080603No ratings yet

- ICICI Securities Limited Annual Report 2017 18Document152 pagesICICI Securities Limited Annual Report 2017 18Avengers HeroesNo ratings yet

- IJRCS20200701 HDocument6 pagesIJRCS20200701 HAKHILESH K RNo ratings yet

- The Role of Dividend Policy As Moderating Variable On Determinant of Stock ReturnsDocument10 pagesThe Role of Dividend Policy As Moderating Variable On Determinant of Stock ReturnsInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- 835-Article Text-3588-1-10-20210818Document15 pages835-Article Text-3588-1-10-20210818Widuri PutriNo ratings yet

- The Influence of Leverage Sales Growth A Fae2c17bDocument14 pagesThe Influence of Leverage Sales Growth A Fae2c17bRicalyn VillaneaNo ratings yet

- Mukta Arts (MUKART) : Multiplex Screen Expansion To Drive Revenue..Document4 pagesMukta Arts (MUKART) : Multiplex Screen Expansion To Drive Revenue..Dinesh ChoudharyNo ratings yet

- Uti AmcDocument3 pagesUti AmcDikshita NavaniNo ratings yet

- Year 2018 in Review: Key Policy Developments For Indian Capital MarketsDocument3 pagesYear 2018 in Review: Key Policy Developments For Indian Capital MarketsskNo ratings yet

- Vadilal Industries LTD.: ContentDocument10 pagesVadilal Industries LTD.: ContentSachin NaikNo ratings yet

- Investment Decisions Through Total Asset Growth Toward Price To Book Value On The Jakarta Islamic IndexDocument12 pagesInvestment Decisions Through Total Asset Growth Toward Price To Book Value On The Jakarta Islamic IndexMuhammad Maulidi Ihsan WahidiNo ratings yet

- Financiall Management Cia - 2120883,2120889,2120845Document29 pagesFinanciall Management Cia - 2120883,2120889,2120845GourishNo ratings yet

- IPO Diary January'2021Document19 pagesIPO Diary January'2021Rakshan ShahNo ratings yet

- Effect of Financial Ratio On Stock Price in TelecoDocument9 pagesEffect of Financial Ratio On Stock Price in Telecotejaguggilam20No ratings yet

- 3 PB PDFDocument13 pages3 PB PDFJoellePeiXianNo ratings yet

- 905pm - 10.EPRA JOURNALS 13145Document3 pages905pm - 10.EPRA JOURNALS 13145Mohammed YASEENNo ratings yet

- Services IndustryDocument13 pagesServices IndustryAbhishek pathangeNo ratings yet

- A Study of Financial Performance of NBFCS: Davinder KaurDocument8 pagesA Study of Financial Performance of NBFCS: Davinder KaurUbaid DarNo ratings yet

- L8 - Analysis and Interpretation of Financial Statements (Part 1)Document17 pagesL8 - Analysis and Interpretation of Financial Statements (Part 1)mishabmoomin1524No ratings yet

- Financial Statement Analysis of Rolls Royce Holdings: February 2022Document19 pagesFinancial Statement Analysis of Rolls Royce Holdings: February 2022Param SohalNo ratings yet

- 509-Article Text-2135-1-10-20220804Document14 pages509-Article Text-2135-1-10-20220804Fransisco FriadiNo ratings yet

- A Study On Financial Performance Asian Paint LTDDocument4 pagesA Study On Financial Performance Asian Paint LTDLevin OliverNo ratings yet

- 1205am - 30.EPRA JOURNALS-4030Document9 pages1205am - 30.EPRA JOURNALS-4030Julyanto Candra Dwi CahyonoNo ratings yet

- ITC Business ValuationDocument5 pagesITC Business ValuationIshita MakkerNo ratings yet

- The Effect of Financial Performance On Stock PriceDocument5 pagesThe Effect of Financial Performance On Stock Pricetejaguggilam20No ratings yet

- Sea Aud Dea Ipo Market Report 2021Document24 pagesSea Aud Dea Ipo Market Report 2021Sassi BaltiNo ratings yet

- Gearing Up For A Favourable Investment ClimateDocument18 pagesGearing Up For A Favourable Investment ClimateGreen VenturesNo ratings yet

- A Study On Financial Performance Analysis of Bharti Airtel LimitedDocument6 pagesA Study On Financial Performance Analysis of Bharti Airtel LimitedInternational Journal of Business Marketing and ManagementNo ratings yet

- Analysis of Competitiveness of The Agribusiness Sector Companies Using Porter'S Five ForcesDocument11 pagesAnalysis of Competitiveness of The Agribusiness Sector Companies Using Porter'S Five ForceseryNo ratings yet

- Factsheet 210129 34 IdxpropertDocument1 pageFactsheet 210129 34 IdxproperterickabrahamNo ratings yet

- Client InformationDocument23 pagesClient Informationnuraisyahputrisrg11No ratings yet

- No Nama Bank Kode BankDocument4 pagesNo Nama Bank Kode BankMas ChitozNo ratings yet

- Analisis Manajemen Strategi Pada PT. Mayora Indah J SmakkssDocument16 pagesAnalisis Manajemen Strategi Pada PT. Mayora Indah J SmakkssKucing OrenNo ratings yet

- GoTo - Improving Prospects, But Lofty ValuationDocument14 pagesGoTo - Improving Prospects, But Lofty ValuationAnonymous XoUqrqyuNo ratings yet

- Indonesian Economic and Capital MarketDocument19 pagesIndonesian Economic and Capital MarketDahlan Tampubolon100% (1)

- IDX Monthly Aug 2017Document114 pagesIDX Monthly Aug 2017miiekoNo ratings yet

- Profil Perusahaan: The Company's ProfileDocument15 pagesProfil Perusahaan: The Company's ProfilePutri AnjaniNo ratings yet

- IDX Data Services Product Pricelist JANUARI 2022Document22 pagesIDX Data Services Product Pricelist JANUARI 2022Antonia KalisaNo ratings yet

- Conference Proceeding Isbs 2018-FixDocument106 pagesConference Proceeding Isbs 2018-Fixusman dachlanNo ratings yet

- WPDT ExportDocument123 pagesWPDT ExportryanmarestahadiNo ratings yet

- Rank Saham-PasmodDocument97 pagesRank Saham-PasmodDominikus Satria ParetaNo ratings yet

- Laporan Bulanan Maret-April 2022-2Document64 pagesLaporan Bulanan Maret-April 2022-2LailiNo ratings yet

- Jurnal Akuntansi Dan Auditing Indonesia: WWW - Journal.uii - Ac.id/index - Php/jaaiDocument13 pagesJurnal Akuntansi Dan Auditing Indonesia: WWW - Journal.uii - Ac.id/index - Php/jaaiAnis Anjala WidyantiNo ratings yet

- Bata LK TW Iv 2020Document110 pagesBata LK TW Iv 2020galihNo ratings yet

- Peserta Webinar UmkmDocument11 pagesPeserta Webinar UmkmPokja Peradu Rawa DurenNo ratings yet

- Account Statement: Melayani Dengan Setulus HatiDocument1 pageAccount Statement: Melayani Dengan Setulus HatiDonna FriskillaNo ratings yet

- BCA Impor Product Material 2021-13 DesDocument10 pagesBCA Impor Product Material 2021-13 DesCalvinNo ratings yet

- HIRING SALES UNDER TL (Responses)Document4 pagesHIRING SALES UNDER TL (Responses)Gunawan Saefuddin TresnadiNo ratings yet

- BAYU - Annual Report 2019Document148 pagesBAYU - Annual Report 2019Aditia Pranita Hardiani TinyotNo ratings yet

- Kode TK KPJ Nomor Identitas Nama LengkapDocument10 pagesKode TK KPJ Nomor Identitas Nama LengkapHari ApriNo ratings yet

- Excel RezaDocument6 pagesExcel RezaArif Nur MuntohaNo ratings yet

- Inv BLN 7fixDocument12 pagesInv BLN 7fixherry blackNo ratings yet

- PT Trakindo Utama: QuotationDocument2 pagesPT Trakindo Utama: QuotationHuda HudaNo ratings yet

- Pengaruh-Lingkungan-Kerja-Terhadap-KinerDocument8 pagesPengaruh-Lingkungan-Kerja-Terhadap-KinerferdiantiNo ratings yet

- Daftar Saham - Consumer Cyclicals - 20231129Document8 pagesDaftar Saham - Consumer Cyclicals - 20231129hfvqddx9bdNo ratings yet

- GLInqueryDocument36 pagesGLInquerynada cintakuNo ratings yet

- Fs Idx30 2023 01Document4 pagesFs Idx30 2023 01jatipuro23No ratings yet

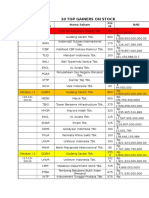

- 10 Top Gainers On Stock: Bulan/Min Ggu Kode Saham Nama Saham Poi NT NABDocument6 pages10 Top Gainers On Stock: Bulan/Min Ggu Kode Saham Nama Saham Poi NT NABFajRin WiCaksonoNo ratings yet

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (15)

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- Your First CFO: The Accounting Cure for Small Business OwnersFrom EverandYour First CFO: The Accounting Cure for Small Business OwnersRating: 4 out of 5 stars4/5 (2)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsFrom EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsNo ratings yet

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineFrom EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineNo ratings yet

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- Beyond the E-Myth: The Evolution of an Enterprise: From a Company of One to a Company of 1,000!From EverandBeyond the E-Myth: The Evolution of an Enterprise: From a Company of One to a Company of 1,000!Rating: 4.5 out of 5 stars4.5/5 (8)

- Financial Accounting For Dummies: 2nd EditionFrom EverandFinancial Accounting For Dummies: 2nd EditionRating: 5 out of 5 stars5/5 (10)

- The Intelligent Investor, Rev. Ed: The Definitive Book on Value InvestingFrom EverandThe Intelligent Investor, Rev. Ed: The Definitive Book on Value InvestingRating: 4.5 out of 5 stars4.5/5 (760)

- Radically Simple Accounting: A Way Out of the Dark and Into the ProfitFrom EverandRadically Simple Accounting: A Way Out of the Dark and Into the ProfitRating: 4.5 out of 5 stars4.5/5 (9)

- Taxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingFrom EverandTaxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingRating: 5 out of 5 stars5/5 (3)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- The Everything Accounting Book: Balance Your Budget, Manage Your Cash Flow, And Keep Your Books in the BlackFrom EverandThe Everything Accounting Book: Balance Your Budget, Manage Your Cash Flow, And Keep Your Books in the BlackRating: 1 out of 5 stars1/5 (1)

- Excel 2019: The Best 10 Tricks To Use In Excel 2019, A Set Of Advanced Methods, Formulas And Functions For Beginners, To Use In Your SpreadsheetsFrom EverandExcel 2019: The Best 10 Tricks To Use In Excel 2019, A Set Of Advanced Methods, Formulas And Functions For Beginners, To Use In Your SpreadsheetsNo ratings yet

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsFrom EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsRating: 5 out of 5 stars5/5 (1)

- The Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceFrom EverandThe Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceRating: 4 out of 5 stars4/5 (1)

- Project Control Methods and Best Practices: Achieving Project SuccessFrom EverandProject Control Methods and Best Practices: Achieving Project SuccessNo ratings yet

- Accounting All-in-One For Dummies, with Online PracticeFrom EverandAccounting All-in-One For Dummies, with Online PracticeRating: 3 out of 5 stars3/5 (1)

- Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetFrom EverandRatio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetRating: 4.5 out of 5 stars4.5/5 (14)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- CDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsFrom EverandCDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsRating: 4 out of 5 stars4/5 (4)

- How to Measure Anything: Finding the Value of "Intangibles" in BusinessFrom EverandHow to Measure Anything: Finding the Value of "Intangibles" in BusinessRating: 4.5 out of 5 stars4.5/5 (28)