You might also like

- Consignment SettlementDocument10 pagesConsignment Settlementramakrishna100% (1)

- In Tax TP Alert Royalty NoexpDocument5 pagesIn Tax TP Alert Royalty NoexpanandarchayaNo ratings yet

- 13 035Document3 pages13 035Reddy ChandraNo ratings yet

- US GAAP Vs IFRS TelecommDocument52 pagesUS GAAP Vs IFRS Telecommludin00100% (1)

- Commercial Bank of Ethiopian Estimation Manual For Mechanical EquipmentDocument47 pagesCommercial Bank of Ethiopian Estimation Manual For Mechanical EquipmentTekeba BirhaneNo ratings yet

- Computer Maintenace Proposal Cost PDFDocument4 pagesComputer Maintenace Proposal Cost PDFjimoh0% (2)

- Guidelines For Implementation of VTMS v3Document6 pagesGuidelines For Implementation of VTMS v3shafin bpNo ratings yet

- DSMatch (Credit) Trade ConfirmationDocument32 pagesDSMatch (Credit) Trade ConfirmationTanisha FlowersNo ratings yet

- Q4A - 2019 - 1219 Technical NewsletterDocument19 pagesQ4A - 2019 - 1219 Technical NewsletterHayat uchyNo ratings yet

- Retail Section Eugene, Sales Reps, Dealers Retail Section Objectives SummaryDocument3 pagesRetail Section Eugene, Sales Reps, Dealers Retail Section Objectives SummaryTony GatandiNo ratings yet

- Electronic Tax Registers 2Document22 pagesElectronic Tax Registers 2Sigei LeonardNo ratings yet

- x220 Lenovo LaptopsDocument20 pagesx220 Lenovo LaptopsEmmanuel MoyoNo ratings yet

- Department Induction Report - AnirbanDocument14 pagesDepartment Induction Report - AnirbanAnirban BaralNo ratings yet

- Sony Ericsson Mobile ComDocument88 pagesSony Ericsson Mobile ComrksuchindraNo ratings yet

- 7 Case Laws Favoring RPM Over TNMM in Case of Distribution FunctionDocument4 pages7 Case Laws Favoring RPM Over TNMM in Case of Distribution Functionadrian araujoNo ratings yet

- ACR-Honeywell - AY 2020-21Document7 pagesACR-Honeywell - AY 2020-21GauravNo ratings yet

- Terms - Financial ServicesDocument4 pagesTerms - Financial Servicesarunkumar116No ratings yet

- Eastern Africa Power Pool (EAPP) Address: P.O Box 100644, Addis-Ababa (Ethiopia) House 059, Wereda 02, Bole Sub CityDocument12 pagesEastern Africa Power Pool (EAPP) Address: P.O Box 100644, Addis-Ababa (Ethiopia) House 059, Wereda 02, Bole Sub CityRumanNet FirstNo ratings yet

- Magic Quadrant For Energy TR 227079Document29 pagesMagic Quadrant For Energy TR 227079attarehNo ratings yet

- Valuation of Machinery - Some Odd SituationsDocument16 pagesValuation of Machinery - Some Odd SituationsO P VermaNo ratings yet

- Atomic Excellence Case - Marking Key - With Examples of Exhibits and Student Response CompositeDocument16 pagesAtomic Excellence Case - Marking Key - With Examples of Exhibits and Student Response Compositedmcook3No ratings yet

- 12 X 22262RevisedBidOpeningDate&AdditionalBidInformation 1 PDFDocument14 pages12 X 22262RevisedBidOpeningDate&AdditionalBidInformation 1 PDFNico LunaNo ratings yet

- Global Location Number (GLN) Implementation Guide: Executive SummaryDocument13 pagesGlobal Location Number (GLN) Implementation Guide: Executive SummaryGreg AdriaanseNo ratings yet

- Srs RtoDocument14 pagesSrs Rtorhlverma2003No ratings yet

- Technology and LicenorDocument7 pagesTechnology and LicenorahmedNo ratings yet

- ERPLO DeemedExport 200614 0653 1304Document4 pagesERPLO DeemedExport 200614 0653 1304SivaprasadVasireddyNo ratings yet

- 2015 2020 CTRM Market OutlookDocument17 pages2015 2020 CTRM Market OutlookCTRM CenterNo ratings yet

- Guidelines For Participation in Loyalty Card Program/sDocument2 pagesGuidelines For Participation in Loyalty Card Program/sHimanshu DaveNo ratings yet

- New Text DocumentDocument4 pagesNew Text DocumentTyler KennNo ratings yet

- Job Profile For The Last Three Years (2012-15)Document3 pagesJob Profile For The Last Three Years (2012-15)venkatraman.pNo ratings yet

- MarkitSERV Preparing For Derivatives Clearing Webinar.10Jun2010Document24 pagesMarkitSERV Preparing For Derivatives Clearing Webinar.10Jun2010senapatiabhijitNo ratings yet

- RMC No. 72-2018Document8 pagesRMC No. 72-2018Larry Tobias Jr.No ratings yet

- The IncotermsDocument6 pagesThe IncotermsAman JoshiNo ratings yet

- Blueprint Doc For Sales: Sales of FG From Mother WarehouseDocument8 pagesBlueprint Doc For Sales: Sales of FG From Mother WarehouseSarfraz MohammedNo ratings yet

- Cases PMTechDocument17 pagesCases PMTechDiptanshu RajNo ratings yet

- The Future of Wireless and Telecom Expense Managed ServicesDocument8 pagesThe Future of Wireless and Telecom Expense Managed ServicesCQHPrincessseNo ratings yet

- Fuel Control and ProcedureDocument10 pagesFuel Control and ProcedureYoga PratamaNo ratings yet

- ASKs 2008Document42 pagesASKs 2008rishijain4No ratings yet

- Case Study AnacompDocument5 pagesCase Study Anacomppiscia1No ratings yet

- EA 2000 Desk Review & ReconciliationDocument43 pagesEA 2000 Desk Review & ReconciliationSushant SaxenaNo ratings yet

- Protection of Intellectual and IndustrialDocument17 pagesProtection of Intellectual and Industrialdanimam01No ratings yet

- IFA WorshopDocument22 pagesIFA WorshophsinhazNo ratings yet

- MM TicketsDocument13 pagesMM Ticketsatesh kumar pandaNo ratings yet

- Terms of Reference (TOR) For Selection of Consulting Audit Firm For Conducting Information Systems Audit of Banglalink Digital Communications LTD PDFDocument5 pagesTerms of Reference (TOR) For Selection of Consulting Audit Firm For Conducting Information Systems Audit of Banglalink Digital Communications LTD PDFফয়সাল হোসেনNo ratings yet

- !C CCCC CCC C C CCCCC C C"CDocument22 pages!C CCCC CCC C C CCCCC C C"CSidharth GoutamNo ratings yet

- Litefinance Client Agreement enDocument26 pagesLitefinance Client Agreement endelcyrodlinNo ratings yet

- NPS Procurement SOP: 1. PurposeDocument4 pagesNPS Procurement SOP: 1. PurposeMohammed Tanjil Morshed remonNo ratings yet

- REVA0511 Murphy PrezDocument19 pagesREVA0511 Murphy PrezAleksa RadosevicNo ratings yet

- White Paper On Fixed Assets Valuation and Fair ValueDocument9 pagesWhite Paper On Fixed Assets Valuation and Fair ValueAmeni WannésNo ratings yet

- G. Spare Parts ManagementDocument12 pagesG. Spare Parts Managementlmn_grssNo ratings yet

- Service Agreement 3.1. Service Scope: Band PrintersDocument7 pagesService Agreement 3.1. Service Scope: Band Printersjaya rajNo ratings yet

- Life 191121Document2,212 pagesLife 191121Mehmood ShahNo ratings yet

- AssignmentDocument5 pagesAssignmentMoin KhanNo ratings yet

- NuanDocument9 pagesNuanmunger649No ratings yet

- Audit ProgDocument7 pagesAudit ProgSara BautistaNo ratings yet

- Opm Gfd165 en 112009 r1 Tubo Amarillo de Rayos XDocument68 pagesOpm Gfd165 en 112009 r1 Tubo Amarillo de Rayos XArides Meneses100% (1)

- Safari PDFDocument2 pagesSafari PDFJairNo ratings yet

- Pioneering Views: Pushing the Limits of Your C/ETRM – Volume 1From EverandPioneering Views: Pushing the Limits of Your C/ETRM – Volume 1No ratings yet

- Pioneering Views: Pushing the Limits of Your C/ETRM - Volume 2From EverandPioneering Views: Pushing the Limits of Your C/ETRM - Volume 2No ratings yet

- La Part 3 PDFDocument23 pagesLa Part 3 PDFShubhaNo ratings yet

- Private Sector Development Task Force Final Report and Way ForwardDocument11 pagesPrivate Sector Development Task Force Final Report and Way ForwardSobia AhmedNo ratings yet

- Presentation - Sacli 2018Document10 pagesPresentation - Sacli 2018Marius OosthuizenNo ratings yet

- List of Topics For A Research Paper EconomicsDocument4 pagesList of Topics For A Research Paper Economicstitamyg1p1j2100% (1)

- GSTR1 Stupl 08ABFCS1229J1Z9 November 2021 BusyDocument92 pagesGSTR1 Stupl 08ABFCS1229J1Z9 November 2021 BusyYathesht JainNo ratings yet

- Accounting EquationDocument2 pagesAccounting Equationmeenagoyal9956No ratings yet

- Jun 16 Bill-AnandDocument1 pageJun 16 Bill-AnandanandNo ratings yet

- The Mastercard Index of Women EntrepreneursDocument118 pagesThe Mastercard Index of Women EntrepreneursxuetingNo ratings yet

- Jurnal Metana TPADocument8 pagesJurnal Metana TPARiska Fauziah AsyariNo ratings yet

- Macro Unit 2 WorksheetDocument5 pagesMacro Unit 2 WorksheetSeth KillianNo ratings yet

- Filt RosDocument6 pagesFilt RosSalva SalazarNo ratings yet

- Thurstone Interest Test by Marie ReyDocument9 pagesThurstone Interest Test by Marie Reymarie annNo ratings yet

- Cola Wars PresentationDocument13 pagesCola Wars PresentationkvnikhilreddyNo ratings yet

- AMT4SAP - Junio26 - Red - v3 PDFDocument30 pagesAMT4SAP - Junio26 - Red - v3 PDFCarlos Eugenio Lovera VelasquezNo ratings yet

- Game Theory (2) - Mechanism Design With TransfersDocument60 pagesGame Theory (2) - Mechanism Design With Transfersjm15yNo ratings yet

- Indraneel N M.com SBKDocument3 pagesIndraneel N M.com SBKJared MartinNo ratings yet

- Invitation To Bid: Dvertisement ArticularsDocument2 pagesInvitation To Bid: Dvertisement ArticularsBDO3 3J SolutionsNo ratings yet

- Firth, Raymond (Ed.) (1964) Capital, Savings and Credit in Peasant Societies (Só o Índice!)Document2 pagesFirth, Raymond (Ed.) (1964) Capital, Savings and Credit in Peasant Societies (Só o Índice!)Felipe SilvaNo ratings yet

- Business StudiesDocument2 pagesBusiness StudiesSonal JhaNo ratings yet

- Joint Stock CompanyDocument2 pagesJoint Stock CompanybijuNo ratings yet

- Manta Aji Coroko Sungsang ASLIDocument1 pageManta Aji Coroko Sungsang ASLIFarhan HumamNo ratings yet

- LP BrochureDocument2 pagesLP BrochureSyed Abdul RafeyNo ratings yet

- Paul Buchanan - Traffic in Towns and Transport in CitiesDocument20 pagesPaul Buchanan - Traffic in Towns and Transport in CitiesRaffaeleNo ratings yet

- EcoTourism Unit 8Document20 pagesEcoTourism Unit 8Mark Angelo PanisNo ratings yet

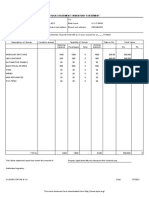

- Stock Statement Format For Bank LoanDocument1 pageStock Statement Format For Bank Loanpsycho Neha40% (5)

- Pune MetroDocument11 pagesPune MetroGanesh NichalNo ratings yet

- Buyer Questionnaire: General QuestionsDocument3 pagesBuyer Questionnaire: General Questionsshweta meshramNo ratings yet

- PPSAS 28 - Financial Instruments - Presentation 3-18-2013Document3 pagesPPSAS 28 - Financial Instruments - Presentation 3-18-2013Christian Ian LimNo ratings yet

- EVALUATION OF BANK OF MAHARASTRA-DevanshuDocument7 pagesEVALUATION OF BANK OF MAHARASTRA-DevanshuDevanshu sharma100% (2)

- Economy of BangladeshDocument22 pagesEconomy of BangladeshRobert DunnNo ratings yet