You might also like

- Running a Good Business - Book 7: Designing Your Space: Running a Good Business, #7From EverandRunning a Good Business - Book 7: Designing Your Space: Running a Good Business, #7No ratings yet

- Supply Chain Management at IKEADocument15 pagesSupply Chain Management at IKEAAsh VaidyaNo ratings yet

- IKEA Case StudyDocument13 pagesIKEA Case StudyAadil KakarNo ratings yet

- Operations in IKEADocument16 pagesOperations in IKEAMUHAMMAD AFIFNo ratings yet

- Ikea Inventory ManagementDocument5 pagesIkea Inventory ManagementChintan Ramnani100% (1)

- Ikea FinalDocument9 pagesIkea FinalPrasad ChamaraNo ratings yet

- Case Study Ikea 2021Document3 pagesCase Study Ikea 2021Timotius Candra KusumaNo ratings yet

- Abiba Culannay Dagan Enicuela Ferrer Gaoiran Pascual Semana Valdez Valente Mm150-Final-requirement-3Document17 pagesAbiba Culannay Dagan Enicuela Ferrer Gaoiran Pascual Semana Valdez Valente Mm150-Final-requirement-3Nyl ValenteNo ratings yet

- IKEADocument6 pagesIKEAKhoi Nguyen TuanNo ratings yet

- FMCG Sector ChainsDocument35 pagesFMCG Sector ChainsNaman ChaudharyNo ratings yet

- IKEA CompanyDocument3 pagesIKEA CompanyTrifan_DumitruNo ratings yet

- Supply Chain MGMTDocument11 pagesSupply Chain MGMTSudhir Sharan KcNo ratings yet

- Supply Chain ManagementDocument3 pagesSupply Chain ManagementAssignment AccountNo ratings yet

- Ikea Retail ManagementDocument28 pagesIkea Retail ManagementLokendra NaikNo ratings yet

- Question 5: Describe The Distribution Strategies of IKEADocument2 pagesQuestion 5: Describe The Distribution Strategies of IKEAthao phuongNo ratings yet

- Financial Management - InventoryDocument32 pagesFinancial Management - InventoryShsvz SvzuvsvzNo ratings yet

- Optimize Suplly ChainDocument4 pagesOptimize Suplly Chaindidouday didaNo ratings yet

- Case StudyDocument3 pagesCase Studynazia malikNo ratings yet

- Case StudyDocument3 pagesCase Studynazia malikNo ratings yet

- Suplly Chain Detail StragegyDocument4 pagesSuplly Chain Detail Stragegydidouday didaNo ratings yet

- Ikea CaseDocument8 pagesIkea CaseumarzNo ratings yet

- Ikea Supply ChainDocument12 pagesIkea Supply ChainNilesh Vasani80% (5)

- Purchasing StrategyDocument8 pagesPurchasing StrategySergiuStefanNo ratings yet

- Apple Gate Way Case StudyDocument2 pagesApple Gate Way Case Studyas gamingNo ratings yet

- Ika Op ModelDocument3 pagesIka Op Modeldidouday didaNo ratings yet

- Inventory & Types of Inventory: The Materials A Company UsesDocument15 pagesInventory & Types of Inventory: The Materials A Company Usesmani gruhkarinNo ratings yet

- Case 2: Ikea Design & Pricing: I. Problem StatementDocument3 pagesCase 2: Ikea Design & Pricing: I. Problem StatementZed Ladja0% (1)

- Gateway-and-Apple 1111Document5 pagesGateway-and-Apple 1111Khulan Tsetsegmaa100% (3)

- 1 - Gateway SolutionDocument12 pages1 - Gateway SolutionMohammad Adil KhushiNo ratings yet

- Supply ChainDocument39 pagesSupply Chainnhoveem_a4No ratings yet

- Logistics Management CHP 5Document33 pagesLogistics Management CHP 5naaim aliasNo ratings yet

- IKEA Case Study: Q.1 What Are IKEA's Competitive Priorities? Answer 1Document2 pagesIKEA Case Study: Q.1 What Are IKEA's Competitive Priorities? Answer 1Maulesh PatelNo ratings yet

- Operaion Case 1Document2 pagesOperaion Case 1Maulesh PatelNo ratings yet

- IKEA Case Study: Q.1 What Are IKEA's Competitive Priorities? Answer 1Document2 pagesIKEA Case Study: Q.1 What Are IKEA's Competitive Priorities? Answer 1Maulesh PatelNo ratings yet

- Case 2. Ikea - FinalDocument3 pagesCase 2. Ikea - FinalKaloy Del PilarNo ratings yet

- Supply Chain End TermDocument17 pagesSupply Chain End TermCHAITRALI DHANANJAY KETKARNo ratings yet

- Essay IkeaDocument6 pagesEssay Ikeadidouday didaNo ratings yet

- Case StudyDocument2 pagesCase StudyNassim NoriqmalNo ratings yet

- Warehousing: Capacity PlanningDocument5 pagesWarehousing: Capacity PlanningAPOORVA GAUR Jaipuria JaipurNo ratings yet

- Supply Suplly IKEADocument3 pagesSupply Suplly IKEAdidouday didaNo ratings yet

- Ikea AnalysisDocument33 pagesIkea AnalysisVinod BridglalsinghNo ratings yet

- Retail Management Que BankDocument11 pagesRetail Management Que BankVaibhav ChavanNo ratings yet

- Operations ManagementDocument20 pagesOperations ManagementLeonardo MercuriNo ratings yet

- Resume Studi Kasus Ikea Kelompok 9Document2 pagesResume Studi Kasus Ikea Kelompok 9Muhammar Ridho MamarNo ratings yet

- The Drivers and Barriers To Sustainable Procurement of IKEADocument6 pagesThe Drivers and Barriers To Sustainable Procurement of IKEAganakhalil37No ratings yet

- IKEA Case Study Read The Following Case Carefully and Answer The Questions at The EndDocument3 pagesIKEA Case Study Read The Following Case Carefully and Answer The Questions at The EndAbdallah Khraim33% (3)

- Case SolvedDocument2 pagesCase SolvedMonjur Morshed RahatNo ratings yet

- Identify The Business Model of IKEADocument3 pagesIdentify The Business Model of IKEAdidouday didaNo ratings yet

- Operations Management Answer 1.: Concept and ApplicationDocument7 pagesOperations Management Answer 1.: Concept and ApplicationkanchanNo ratings yet

- Section 5Document4 pagesSection 5Zatul AqlimaNo ratings yet

- M3. Case - Mohammad Ezykel Pasha - 205040107111009Document2 pagesM3. Case - Mohammad Ezykel Pasha - 205040107111009ezykelpashaaNo ratings yet

- A Case Study On IKEA Giving A Brief by HananDocument52 pagesA Case Study On IKEA Giving A Brief by HananHanan AbdullahNo ratings yet

- Case Study IKEADocument4 pagesCase Study IKEAsiti_syahirah100% (1)

- OSCM-IKEA Case Kel - 1 UpdateDocument29 pagesOSCM-IKEA Case Kel - 1 UpdateOde Majid Al IdrusNo ratings yet

- Understand The Business Model of IKEADocument1 pageUnderstand The Business Model of IKEAdidouday didaNo ratings yet

- Ikea Edition 14 Full PDFDocument4 pagesIkea Edition 14 Full PDFuroojishfaqNo ratings yet

- Evidencia 2.1Document6 pagesEvidencia 2.1Salvador GalindoNo ratings yet

- Group4 IKEADocument21 pagesGroup4 IKEAHardik singal100% (1)

- Jas PDFDocument34 pagesJas PDFJasenriNo ratings yet

- National Income Accounting PPT at MBADocument58 pagesNational Income Accounting PPT at MBABabasab Patil (Karrisatte)No ratings yet

- Sap Fi 4.6 Exercises Financial Accounting - Chapter 29 Appendix 1. Sales & Use TaxDocument3 pagesSap Fi 4.6 Exercises Financial Accounting - Chapter 29 Appendix 1. Sales & Use TaxVaibhavNo ratings yet

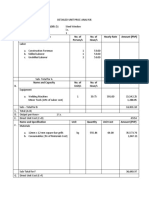

- DETAILED UNIT PRICE ANALYSIS CadDocument7 pagesDETAILED UNIT PRICE ANALYSIS CadIan Kirby RedondoNo ratings yet

- Macroeconomics 6th Edition Hall Test Bank DownloadDocument47 pagesMacroeconomics 6th Edition Hall Test Bank DownloadSang Proper100% (22)

- Pestel Analysis of Cleaning Service IndustryDocument23 pagesPestel Analysis of Cleaning Service IndustryThilinaAbhayarathneNo ratings yet

- M1 24Document18 pagesM1 24Sarah LawrenceNo ratings yet

- National Income AssignmentDocument12 pagesNational Income AssignmentMaher SrivastavaNo ratings yet

- Measuring Economic Activity: Measuring Economic ActivityDocument42 pagesMeasuring Economic Activity: Measuring Economic ActivityWAC_BADSECTORNo ratings yet

- Vat OptDocument24 pagesVat OptCharity Venus100% (1)

- And Inclusion Law) Revenue Regulations 13-2018Document2 pagesAnd Inclusion Law) Revenue Regulations 13-2018Rnemcdg100% (1)

- Financial Accounting For Managers Author: Sanjay Dhamija Financial Accounting For Managers Author: Sanjay DhamijaDocument23 pagesFinancial Accounting For Managers Author: Sanjay Dhamija Financial Accounting For Managers Author: Sanjay Dhamijashweta sarafNo ratings yet

- Productivity of Cement Industry of PakistanDocument37 pagesProductivity of Cement Industry of Pakistansyed usman wazir100% (9)

- Cost Sheets Road Constructionxlsx PDF FreeDocument765 pagesCost Sheets Road Constructionxlsx PDF FreemggmlrdgNo ratings yet

- Main Course Recipe CostingDocument22 pagesMain Course Recipe Costingbigbrownmoolah0% (1)

- 5.1 - Raymond Monroe - SFSADocument8 pages5.1 - Raymond Monroe - SFSAAnonymous iztPUhIiNo ratings yet

- In The High Court of Delhi at New Delhi W.P. (C) No. 11569/2016Document29 pagesIn The High Court of Delhi at New Delhi W.P. (C) No. 11569/2016Bhan WatiNo ratings yet

- Chapter 23 Measuring A Nations IncomeDocument37 pagesChapter 23 Measuring A Nations IncomeNazeNo ratings yet

- Macro Eco Complete Ques+NotesDocument117 pagesMacro Eco Complete Ques+NotesPiyush ChhajerNo ratings yet

- Siklus Akuntansi Laporan KeuanganDocument67 pagesSiklus Akuntansi Laporan KeuanganAlya AdeliaNo ratings yet

- Statistical Appendix in English PDFDocument176 pagesStatistical Appendix in English PDFHari KishanNo ratings yet

- 2006 ArDocument176 pages2006 ArMoch Rifki HartantoNo ratings yet

- 12 SM Economics PDFDocument204 pages12 SM Economics PDFMukund BansalNo ratings yet

- Value Added ReportingDocument6 pagesValue Added ReportingnindywahyuNo ratings yet

- GDP GNP NNPDocument7 pagesGDP GNP NNPAmjad KhanNo ratings yet

- ECON140-Chapter 25-Measuring Domestic Output and National IncomeDocument18 pagesECON140-Chapter 25-Measuring Domestic Output and National IncomeI GuessNo ratings yet

- 07 X07 A ResponsibilityDocument12 pages07 X07 A ResponsibilityMark Anthony Bulahan100% (1)

- POW Road Safety 2.0Document107 pagesPOW Road Safety 2.0Jay RickNo ratings yet

- VAT Exempt TransactionsDocument11 pagesVAT Exempt TransactionsChristine AceronNo ratings yet

- IES I-O Report Draft v2 20221103Document40 pagesIES I-O Report Draft v2 20221103Jovan ZubovicNo ratings yet