You might also like

- Chapter 8 Prob SolutionsDocument9 pagesChapter 8 Prob SolutionsManoj GirigoswamiNo ratings yet

- Determining Cash Flows for Investment AnalysisDocument19 pagesDetermining Cash Flows for Investment AnalysisJack mazeNo ratings yet

- FM09-CH 10.... Im PandeyDocument19 pagesFM09-CH 10.... Im Pandeywarlock83% (6)

- Ch 4: Risk and Return ExplainedDocument4 pagesCh 4: Risk and Return ExplainedMukul KadyanNo ratings yet

- FM09-CH 11Document5 pagesFM09-CH 11Mukul KadyanNo ratings yet

- FM09-CH 03Document14 pagesFM09-CH 03vtiwari2No ratings yet

- FM09-CH 14Document12 pagesFM09-CH 14Mukul KadyanNo ratings yet

- Cash Management Chapter SummaryDocument4 pagesCash Management Chapter SummaryMukul KadyanNo ratings yet

- Calculating the Cost of CapitalDocument12 pagesCalculating the Cost of CapitalMukul KadyanNo ratings yet

- FM09-CH 15Document7 pagesFM09-CH 15Mukul Kadyan100% (1)

- Chapter 3 Prob SolutionsDocument33 pagesChapter 3 Prob SolutionsMehak Ayoub100% (1)

- FM09-CH 29 PDFDocument2 pagesFM09-CH 29 PDFNaveen RaiNo ratings yet

- FM09-CH 03 PDFDocument14 pagesFM09-CH 03 PDFGregNo ratings yet

- FM09-CH 17Document5 pagesFM09-CH 17Mukul KadyanNo ratings yet

- FM09-CH 02Document15 pagesFM09-CH 02دهيرج بهارتي75% (4)

- FM09-CH 27Document6 pagesFM09-CH 27Kritika SwaminathanNo ratings yet

- Ch 5: Risk Return Portfolio Theory Assets PricingDocument4 pagesCh 5: Risk Return Portfolio Theory Assets PricingMukul KadyanNo ratings yet

- Ch. 6: Beta Estimation and The Cost of EquityDocument2 pagesCh. 6: Beta Estimation and The Cost of EquitymallikaNo ratings yet

- Sample TestDocument6 pagesSample TestSajeni50% (2)

- Convertible Debentures and Warrants ExplainedDocument4 pagesConvertible Debentures and Warrants ExplainedMukul KadyanNo ratings yet

- Receivable Management Llustration 1: A Company Has Prepared The Following Projections For A YearDocument6 pagesReceivable Management Llustration 1: A Company Has Prepared The Following Projections For A YearJC Del MundoNo ratings yet

- 1-B-DTU: 2k21/DMBA/95 and Ranjit GaneshDocument4 pages1-B-DTU: 2k21/DMBA/95 and Ranjit GaneshAdityaNo ratings yet

- Are Mergers The Only Solution To Revive Debt Driven BanksDocument3 pagesAre Mergers The Only Solution To Revive Debt Driven BanksKIPKOSKEI MARKNo ratings yet

- Project Finance - Test - QuestionDocument18 pagesProject Finance - Test - QuestionDeepika67% (3)

- CH 22: Lease, Hire Purchase and Project FinancingDocument7 pagesCH 22: Lease, Hire Purchase and Project FinancingMukul KadyanNo ratings yet

- Calculating operating, financial and combined leverageDocument4 pagesCalculating operating, financial and combined leveragek,hbibk,n0% (1)

- Taxable Salary Problem With Solution Part 1Document2 pagesTaxable Salary Problem With Solution Part 1NagadeepaNo ratings yet

- Calculating finance lease accounting entriesDocument7 pagesCalculating finance lease accounting entriessajedulNo ratings yet

- Mini CaseDocument15 pagesMini CaseSammir Malhotra0% (1)

- Problems & Solutions On Fundamental AnalysisDocument8 pagesProblems & Solutions On Fundamental AnalysisAnonymous sTsnRsYlnkNo ratings yet

- Chapter 7 Valuation of Stock & Bond Prasnna ChandraDocument5 pagesChapter 7 Valuation of Stock & Bond Prasnna Chandraحسينبيسواس100% (1)

- Sample TestDocument6 pagesSample TestSajeniNo ratings yet

- Modern Pharma SolnDocument3 pagesModern Pharma SolnSakshiNo ratings yet

- Srinath SirDocument19 pagesSrinath Sirmy Vinay100% (1)

- Indian Electricals Weighs Accepting Trial Order for Vending MachinesDocument8 pagesIndian Electricals Weighs Accepting Trial Order for Vending MachinesJoseph MathewNo ratings yet

- Prasanna Chandra Financial ManagementDocument163 pagesPrasanna Chandra Financial ManagementVamsi GunturuNo ratings yet

- TVM Assignment MBA 2013 - 27 ..... NagendraDocument74 pagesTVM Assignment MBA 2013 - 27 ..... NagendraNaga NagendraNo ratings yet

- Chapter 3: Valuation of Bonds and Shares Problem 1: 0 INT YieldDocument25 pagesChapter 3: Valuation of Bonds and Shares Problem 1: 0 INT YieldPayal ChauhanNo ratings yet

- Solution To QB QuestionsDocument3 pagesSolution To QB QuestionsSurabhi Suman100% (1)

- CH 02 Revised Financial Management by IM PandeyDocument38 pagesCH 02 Revised Financial Management by IM PandeyAnjan Kumar100% (6)

- Dividend DecisionDocument4 pagesDividend DecisionKhushi RaniNo ratings yet

- Solution 1Document8 pagesSolution 1frq qqrNo ratings yet

- Case 27.1: Reliable Texamill Limited: PBF: IDocument2 pagesCase 27.1: Reliable Texamill Limited: PBF: IMukul KadyanNo ratings yet

- Budgetory Control Flexible Budget With SolutionsDocument6 pagesBudgetory Control Flexible Budget With SolutionsJash SanghviNo ratings yet

- Prasanna Chandra Chapter 6 SolutionDocument14 pagesPrasanna Chandra Chapter 6 Solutionnikaro198983% (6)

- 1 Working CapitalDocument63 pages1 Working CapitalDeepika Mittal50% (2)

- Techniques of Capital Budgeting SumsDocument15 pagesTechniques of Capital Budgeting Sumshardika jadavNo ratings yet

- Internal Test - 2 - FSA - QuestionDocument3 pagesInternal Test - 2 - FSA - QuestionSandeep Choudhary40% (5)

- Additional ProblemsDocument21 pagesAdditional Problemsdarshan jain0% (1)

- Valuation of Securities - ASSIGNMENTDocument63 pagesValuation of Securities - ASSIGNMENTNaga Nagendra0% (2)

- Financial ManagementDocument8 pagesFinancial ManagementshrutiNo ratings yet

- Financial Modelling Complete Internal Test 4Document6 pagesFinancial Modelling Complete Internal Test 4vaibhav100% (1)

- Test Your Knowledge: Theoretical QuestionsDocument30 pagesTest Your Knowledge: Theoretical QuestionsRITZ BROWN50% (2)

- Calculating Time Value of Money ProblemsDocument12 pagesCalculating Time Value of Money ProblemsGautamMandalNo ratings yet

- (Rs MN.) : Case 10.1: Hind Petrochemicals CompanyDocument1 page(Rs MN.) : Case 10.1: Hind Petrochemicals Companylefteris82No ratings yet

- Capital BudgetingDocument22 pagesCapital BudgetingKamal GanugulaNo ratings yet

- CF 2Document26 pagesCF 2PUSHKAL AGGARWALNo ratings yet

- Cumulative Cash Flow Discounted Cash Flow Cum Discounted Cash FlowDocument173 pagesCumulative Cash Flow Discounted Cash Flow Cum Discounted Cash FlowAditi OholNo ratings yet

- ES _GROUP 8Document4 pagesES _GROUP 8Papa NketsiahNo ratings yet

- PC Ch. 11 Techniques of Capital BudgetingDocument22 pagesPC Ch. 11 Techniques of Capital BudgetingVinod Mathews100% (2)

- FM09-CH 24Document16 pagesFM09-CH 24namitabijweNo ratings yet

- FM09-CH 16Document12 pagesFM09-CH 16Mukul KadyanNo ratings yet

- FM09-CH 14Document12 pagesFM09-CH 14Mukul KadyanNo ratings yet

- Dividend Policy AnalysisDocument5 pagesDividend Policy AnalysisMukul KadyanNo ratings yet

- FM09-CH 25Document9 pagesFM09-CH 25Mukul KadyanNo ratings yet

- CH 22: Lease, Hire Purchase and Project FinancingDocument7 pagesCH 22: Lease, Hire Purchase and Project FinancingMukul KadyanNo ratings yet

- Calculating the Cost of CapitalDocument12 pagesCalculating the Cost of CapitalMukul KadyanNo ratings yet

- Financial Planning and Strategy Problem 1 Bajaj Auto LTDDocument4 pagesFinancial Planning and Strategy Problem 1 Bajaj Auto LTDMukul KadyanNo ratings yet

- FM09-CH 15Document7 pagesFM09-CH 15Mukul Kadyan100% (1)

- FM09-CH 28Document8 pagesFM09-CH 28Nikhil ChitaliaNo ratings yet

- Ch 7: Guide to Option Pricing ConceptsDocument9 pagesCh 7: Guide to Option Pricing ConceptsMukul KadyanNo ratings yet

- FM09-CH 27Document6 pagesFM09-CH 27Kritika SwaminathanNo ratings yet

- Cash Management Chapter SummaryDocument4 pagesCash Management Chapter SummaryMukul KadyanNo ratings yet

- International Financial Management ExplainedDocument7 pagesInternational Financial Management ExplainedMukul KadyanNo ratings yet

- Calculating Asset Beta, Levered Equity Beta, and WACCDocument8 pagesCalculating Asset Beta, Levered Equity Beta, and WACCMukul KadyanNo ratings yet

- Long-term Finance Options for Delite FurnitureDocument4 pagesLong-term Finance Options for Delite FurnitureNaveen RaiNo ratings yet

- FM09-CH 35Document4 pagesFM09-CH 35lefteris82No ratings yet

- Mergers and Acquisitions Chapter: Key Concepts and Valuation TechniquesDocument3 pagesMergers and Acquisitions Chapter: Key Concepts and Valuation TechniquesNaveen RaiNo ratings yet

- Chapter 27Document10 pagesChapter 27Mukul KadyanNo ratings yet

- FM09-CH 03 PDFDocument14 pagesFM09-CH 03 PDFGregNo ratings yet

- Inventory Management Objectives and TechniquesDocument8 pagesInventory Management Objectives and TechniquesMukul KadyanNo ratings yet

- FM09-CH 29 PDFDocument2 pagesFM09-CH 29 PDFNaveen RaiNo ratings yet

- Chapter 07Document8 pagesChapter 07Mukul KadyanNo ratings yet

- FM - Chapter 35Document4 pagesFM - Chapter 35Amit SukhaniNo ratings yet

- Chapter 05Document6 pagesChapter 05danbrowndaNo ratings yet

- FM09-CH 12Document7 pagesFM09-CH 12Mukul KadyanNo ratings yet

- Ch 5: Risk Return Portfolio Theory Assets PricingDocument4 pagesCh 5: Risk Return Portfolio Theory Assets PricingMukul KadyanNo ratings yet

- The Shadow Money Lenders - Significance of Fed's Zirp PolicyDocument8 pagesThe Shadow Money Lenders - Significance of Fed's Zirp Policyasksigma6No ratings yet

- MBA Akshay Arora: SAP ID:80511020627 - : Akshay - Arora27@nmims - Edu.in - Age: 23Document2 pagesMBA Akshay Arora: SAP ID:80511020627 - : Akshay - Arora27@nmims - Edu.in - Age: 23gautam keswaniNo ratings yet

- Free GameDocument1 pageFree GameSC AyuburiNo ratings yet

- Borrowing Costs: DefinitionsDocument23 pagesBorrowing Costs: DefinitionsAbdul Sami100% (1)

- Chapter 9 Intercompany Bond Holdings and Miscellaneous Topics-Consolidated Financial StatementsDocument45 pagesChapter 9 Intercompany Bond Holdings and Miscellaneous Topics-Consolidated Financial StatementsAchmad RizalNo ratings yet

- Final Executive SummaryDocument19 pagesFinal Executive Summarydas_s13No ratings yet

- 2021 Remaining Ongoing CasesDocument2,517 pages2021 Remaining Ongoing CasesJulia Mar Antonete Tamayo AcedoNo ratings yet

- Target Market AnalysisDocument6 pagesTarget Market AnalysisAllyssa LaquindanumNo ratings yet

- CV-Agus Nugraha (For IUWASH PLUS - RC Surakarta)Document11 pagesCV-Agus Nugraha (For IUWASH PLUS - RC Surakarta)Agus NugrahaNo ratings yet

- Masinde Muliro University of Science & Technology: School of Computing & InformaticsDocument2 pagesMasinde Muliro University of Science & Technology: School of Computing & InformaticsBrandon JaphetNo ratings yet

- SSRN Id4207171Document39 pagesSSRN Id4207171Nhat LinhNo ratings yet

- BGC Internship Job Description On LetterheadDocument4 pagesBGC Internship Job Description On Letterheadgadija ishahNo ratings yet

- Implementation OF "Smart Street Lighting" For Spine Roads in Guwahati OnDocument78 pagesImplementation OF "Smart Street Lighting" For Spine Roads in Guwahati OnDhirajGogoiNo ratings yet

- CHAPTER 1.1 Basic Concepts of ManagementsDocument15 pagesCHAPTER 1.1 Basic Concepts of ManagementsRay John DulapNo ratings yet

- Visa Wizard - France-VisasDocument2 pagesVisa Wizard - France-VisasAbthal Tenore Al-fasnaNo ratings yet

- The Prevention of Corruption Act, 1988: A Critical StudyDocument33 pagesThe Prevention of Corruption Act, 1988: A Critical StudyRAJARAJESHWARI M GNo ratings yet

- Marketing Plan Guidelines:: Bus314 Marketing Management (Ncy)Document2 pagesMarketing Plan Guidelines:: Bus314 Marketing Management (Ncy)Murgi kun :3No ratings yet

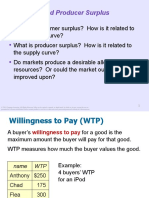

- CS, PS and EfficiencyDocument45 pagesCS, PS and EfficiencySubodh MohapatroNo ratings yet

- College Fees StructureDocument1 pageCollege Fees StructureVijay MNo ratings yet

- Equity CrowdfundingDocument13 pagesEquity CrowdfundingantonyNo ratings yet

- SW One DXP Cost Sheet (4.5BHK+Utility) Phase 2Document1 pageSW One DXP Cost Sheet (4.5BHK+Utility) Phase 2assetcafe7No ratings yet

- Quiz Manajemen Pengadaan - Nisrina Zalfa Farida - 21B505041003Document5 pagesQuiz Manajemen Pengadaan - Nisrina Zalfa Farida - 21B505041003Kuro DitNo ratings yet

- ES 301 Assignment #1 engineering economy problems and solutionsDocument2 pagesES 301 Assignment #1 engineering economy problems and solutionsErika Rez LapatisNo ratings yet

- Agile Development: © Lpu:: Cap437: Software Engineering Practices: Ashwani Kumar TewariDocument28 pagesAgile Development: © Lpu:: Cap437: Software Engineering Practices: Ashwani Kumar TewariAnanth KallamNo ratings yet

- Understanding Cryptocurrencies: Bitcoin, Ethereum, and Altcoins As An Asset ClassDocument24 pagesUnderstanding Cryptocurrencies: Bitcoin, Ethereum, and Altcoins As An Asset ClassCharlene KronstedtNo ratings yet

- Methods of Valuation of FirmsDocument90 pagesMethods of Valuation of Firmsmuskaan bhadadaNo ratings yet

- Goldsavers Food Enterprises - Business PlanDocument50 pagesGoldsavers Food Enterprises - Business PlanAyie Rose HernandezNo ratings yet

- Account Usage and Recharge Statement From 01-Jan-2023 To 29-Jan-2023Document9 pagesAccount Usage and Recharge Statement From 01-Jan-2023 To 29-Jan-2023Shubham VishwakarmaNo ratings yet

- FIN 5001 - Course Outline 2022Document8 pagesFIN 5001 - Course Outline 2022adharsh veeraNo ratings yet