You might also like

- Insurance, regulations and loss prevention :Basic Rules for the industry Insurance: Business strategy books, #5From EverandInsurance, regulations and loss prevention :Basic Rules for the industry Insurance: Business strategy books, #5No ratings yet

- Risk Management and Insurance - Learn how to Manage Risks and Secure Your FutureFrom EverandRisk Management and Insurance - Learn how to Manage Risks and Secure Your FutureNo ratings yet

- Insurance BusinessDocument23 pagesInsurance BusinessLetsah BrightNo ratings yet

- Warranty LiabilityDocument10 pagesWarranty LiabilityGennelyn Grace PenaredondoNo ratings yet

- Ifrs 17 Reinsurance Contract Held ExampleDocument24 pagesIfrs 17 Reinsurance Contract Held ExampleHesham AlabaniNo ratings yet

- Principle of Insurance Group No-08: ReinsuranceDocument66 pagesPrinciple of Insurance Group No-08: ReinsuranceNayem OpuNo ratings yet

- CompleteHealthInsuranceBrochure PDFDocument16 pagesCompleteHealthInsuranceBrochure PDFRishi AroraNo ratings yet

- Complete Health Insurance-Brochure PDFDocument16 pagesComplete Health Insurance-Brochure PDFRishi AroraNo ratings yet

- Insurance Approach: Mortality Models and Credit Risk +Document6 pagesInsurance Approach: Mortality Models and Credit Risk +Madhusudan RaoNo ratings yet

- Cash Surrender ValueDocument4 pagesCash Surrender ValueChristian MagbanuaNo ratings yet

- Taxation of Insurance Companies RevisedDocument8 pagesTaxation of Insurance Companies RevisedTriila manillaNo ratings yet

- Chapter 3 - Warranty LiabilityDocument3 pagesChapter 3 - Warranty LiabilityMarx Yuri Jayme100% (2)

- Warranty Liability: Start of DiscussionDocument2 pagesWarranty Liability: Start of DiscussionclarizaNo ratings yet

- Original 1489564193 Chapter 1 Principles of ReinsuranceDocument20 pagesOriginal 1489564193 Chapter 1 Principles of ReinsurancemakeshwaranNo ratings yet

- Kelioniu Draudimo Patvirtinimas Anglu (New Visa) 2Document1 pageKelioniu Draudimo Patvirtinimas Anglu (New Visa) 2sigitasNo ratings yet

- B.COM. Sem-5 Insurance ClaimsDocument12 pagesB.COM. Sem-5 Insurance ClaimsDeepeshNo ratings yet

- Conditions Générales D'assurance 1.7.2016 ANGDocument40 pagesConditions Générales D'assurance 1.7.2016 ANGxavo_27No ratings yet

- Great Eastern Life Assurance (Malaysia) Berhad: MR EngineerDocument37 pagesGreat Eastern Life Assurance (Malaysia) Berhad: MR EngineerLeong VicNo ratings yet

- A3. Year End AdjustmentsDocument9 pagesA3. Year End AdjustmentsFrankNo ratings yet

- Insurance Claim AccountDocument26 pagesInsurance Claim AccountAdiNo ratings yet

- Module 2-WARRANTY LIABILITY and PROVISION AND CONTINGENT LIABILITYDocument12 pagesModule 2-WARRANTY LIABILITY and PROVISION AND CONTINGENT LIABILITYJeanivyle CarmonaNo ratings yet

- FormulasDocument35 pagesFormulasgonzalo gutierrezNo ratings yet

- Module 3Document6 pagesModule 3Alextrasza LouiseNo ratings yet

- CertificateDocument2 pagesCertificateMahmut SoyerNo ratings yet

- US and Global MRC Slip Examples.Document49 pagesUS and Global MRC Slip Examples.Yudhisthar SinghNo ratings yet

- Accounts of Insurance Cos ProjectDocument14 pagesAccounts of Insurance Cos ProjectAditya SoodNo ratings yet

- Chapter 2Document54 pagesChapter 2Anonymous WO7vzkjvNNo ratings yet

- Reinsurance Dissertation TopicsDocument5 pagesReinsurance Dissertation TopicsBuyPapersForCollegeOnlineCanada100% (2)

- Celebrating 60 Years of Excellence, Sri Lanka Insurance PresentsDocument2 pagesCelebrating 60 Years of Excellence, Sri Lanka Insurance PresentsSivaneswaran ChandrasekaranNo ratings yet

- Chap 015Document21 pagesChap 015Ahmed El KhateebNo ratings yet

- Jawaban Soal No.1Document2 pagesJawaban Soal No.1Enci UnsriyaniNo ratings yet

- WPLUK Certificate of Insurance Summary EPPL and CAR To 30th May 2019Document1 pageWPLUK Certificate of Insurance Summary EPPL and CAR To 30th May 2019Electro-repairNo ratings yet

- Chaper 03Document13 pagesChaper 03Consiko leeNo ratings yet

- Insurance Cover For Stays Abroad: What Is Not Insured? What Is Insured?Document8 pagesInsurance Cover For Stays Abroad: What Is Not Insured? What Is Insured?AniaNo ratings yet

- Warranty-WPS OfficeDocument2 pagesWarranty-WPS OfficeJerryca CabadduNo ratings yet

- The Law of Insurance (Exclusive)Document17 pagesThe Law of Insurance (Exclusive)belay abebeNo ratings yet

- 3.4 Alternative Risk Transfer (Art)Document62 pages3.4 Alternative Risk Transfer (Art)david AbotsitseNo ratings yet

- Pruposal - Mrms. ReyesDocument1 pagePruposal - Mrms. ReyesKriza Matro-FloresNo ratings yet

- Lesson 6Document16 pagesLesson 6visiontanzania2022No ratings yet

- Accounting for ProvisionsDocument40 pagesAccounting for Provisionsammad uddinNo ratings yet

- PFRS 17 Insurance ContractsDocument23 pagesPFRS 17 Insurance ContractsCharles MateoNo ratings yet

- Insurance Manual Ver 1Document82 pagesInsurance Manual Ver 1api-3743824No ratings yet

- Sums On Fire Inurance PolicyDocument19 pagesSums On Fire Inurance PolicyPrabhat Kumar GuptaNo ratings yet

- Insurance Claims For Loss of Stock and Loss of Profit 2 PDFDocument22 pagesInsurance Claims For Loss of Stock and Loss of Profit 2 PDFEswari Gk100% (1)

- Info Lec 4Document2 pagesInfo Lec 4mostafa abdoNo ratings yet

- CH - 02 Issue and Redemption of DebenturesDocument7 pagesCH - 02 Issue and Redemption of DebenturesMahathi AmudhanNo ratings yet

- Policy Borislav Vulic 20230301 10014241154Document5 pagesPolicy Borislav Vulic 20230301 10014241154Borislav VulicNo ratings yet

- Toaz - Info Module 2 Warranty Liability and Provision and Contingent Liability PRDocument20 pagesToaz - Info Module 2 Warranty Liability and Provision and Contingent Liability PRHanna RomasantaNo ratings yet

- Risk 3Document35 pagesRisk 3Yisihak SimionNo ratings yet

- Module 2-WARRANTY LIABILITY and PROVISION AND CONTINGENT LIABILITYDocument20 pagesModule 2-WARRANTY LIABILITY and PROVISION AND CONTINGENT LIABILITYKathleen Sales75% (4)

- Advanced Financial Reporting: Module 4: Final Accounts of Insurance CompaniesDocument23 pagesAdvanced Financial Reporting: Module 4: Final Accounts of Insurance CompaniesBijosh ThomasNo ratings yet

- Life and Endowment InsuranceDocument9 pagesLife and Endowment InsuranceAmanuel HabtamuNo ratings yet

- Unit-6C Insurance-ClaimsDocument49 pagesUnit-6C Insurance-Claimsadityaupreti2003No ratings yet

- Insurance: Dr. Andrea LuDocument12 pagesInsurance: Dr. Andrea LuMia RenNo ratings yet

- Risk Management Chapter ThreeDocument8 pagesRisk Management Chapter ThreeDaniel filmonNo ratings yet

- AGUSTIARDocument3 pagesAGUSTIARsophie anastasyaNo ratings yet

- Chapter 2Document54 pagesChapter 2aditi_khot86No ratings yet

- Insurance Claims For Loss of Stock and Loss of Profit 2Document22 pagesInsurance Claims For Loss of Stock and Loss of Profit 2Eswari GkNo ratings yet

- Harrison FA IFRS 11e CH09 SMDocument106 pagesHarrison FA IFRS 11e CH09 SMShako GrdzelidzeNo ratings yet

- IFRS 17 - An Implementation Case Study v6 V ZurichDocument17 pagesIFRS 17 - An Implementation Case Study v6 V ZurichЙоанна ЗNo ratings yet

- IFRS 17 Requirements for Short-Term Insurance ContractsDocument11 pagesIFRS 17 Requirements for Short-Term Insurance ContractsЙоанна ЗNo ratings yet

- Supervisory Implications of IFRS 17 Insurance Contracts - Executive SummaryDocument3 pagesSupervisory Implications of IFRS 17 Insurance Contracts - Executive SummaryЙоанна ЗNo ratings yet

- Deloitte CH en Ifrs 17 Webinar 3febDocument23 pagesDeloitte CH en Ifrs 17 Webinar 3febЙоанна ЗNo ratings yet

- Google+ Insights: Meaningful Metrics To Optimize Your Google+ StrategyDocument2 pagesGoogle+ Insights: Meaningful Metrics To Optimize Your Google+ StrategyЙоанна ЗNo ratings yet

- IFRS in Your Pocket 2019 PDFDocument116 pagesIFRS in Your Pocket 2019 PDFzahid hameedNo ratings yet

- MPDF PDFDocument3 pagesMPDF PDFЙоанна ЗNo ratings yet

- Company Registration Status As On 10.12.2019Document1 pageCompany Registration Status As On 10.12.2019Vishav JindalNo ratings yet

- 2018-19 - Part B - 1Document4 pages2018-19 - Part B - 1Shivam DixitNo ratings yet

- DieMax XL Springs PDFDocument30 pagesDieMax XL Springs PDFthefernandomanNo ratings yet

- Guidelines - 35 (2AB) OF IT ACT 1961 - May2014Document29 pagesGuidelines - 35 (2AB) OF IT ACT 1961 - May2014rupesh.srivastavaNo ratings yet

- STUDENT'S PROVISIONAL LLB RESULTSDocument1 pageSTUDENT'S PROVISIONAL LLB RESULTSMukiibi DuncanNo ratings yet

- BEC 3 Outline - 2015 Becker CPA ReviewDocument4 pagesBEC 3 Outline - 2015 Becker CPA ReviewGabrielNo ratings yet

- Legal and Regulatory Aspects of Money Laundering: Presented byDocument80 pagesLegal and Regulatory Aspects of Money Laundering: Presented byHema MehtaNo ratings yet

- The Survival Strategies of Singapore Contractors in Prolonged RecessionDocument17 pagesThe Survival Strategies of Singapore Contractors in Prolonged RecessionKsenia BriliantNo ratings yet

- Ch-2 Strategy OMDocument8 pagesCh-2 Strategy OMAditya AgrawalNo ratings yet

- BBC Knowledge Magazine 2017Document97 pagesBBC Knowledge Magazine 2017Le Do Ngoc Hang100% (1)

- Feasibility Study Guide USDA1Document24 pagesFeasibility Study Guide USDA1Jessica Ddw FianzaNo ratings yet

- Radhuni - 6Document33 pagesRadhuni - 6api-2602743880% (5)

- Major Rights As An Air PassengerDocument6 pagesMajor Rights As An Air PassengerSunStar Philippine NewsNo ratings yet

- PT Synergy Specialist Engineeringii-Ilovepdf-CompressedDocument5 pagesPT Synergy Specialist Engineeringii-Ilovepdf-CompressedAnonymous waSxJGoNo ratings yet

- Franchise FormDocument2 pagesFranchise FormHani Rocks100% (1)

- BI ApplicationsDocument18 pagesBI ApplicationsSumit JhaNo ratings yet

- B2B Branding A Financial Burden For ShareholdersDocument8 pagesB2B Branding A Financial Burden For ShareholdersVinothNo ratings yet

- Red BullDocument17 pagesRed BullKishore DevisettyNo ratings yet

- Curriculum Vitae: Umamahesh .MavuluriDocument3 pagesCurriculum Vitae: Umamahesh .MavuluriUmamahesh MavuluriNo ratings yet

- Marketing Management BasicsDocument10 pagesMarketing Management BasicsNikhil MendaNo ratings yet

- Keeling Braves Lawsuit626Document48 pagesKeeling Braves Lawsuit626Michael KingNo ratings yet

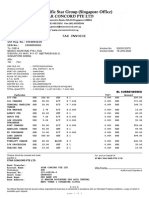

- Invoice SII22012979Document2 pagesInvoice SII22012979Summersky9333No ratings yet

- Cfas ReviewerDocument10 pagesCfas ReviewershaylieeeNo ratings yet

- Oracle Fusion Middleware Developer GuideDocument1,422 pagesOracle Fusion Middleware Developer GuideahsunNo ratings yet

- Organizational BehaviorDocument10 pagesOrganizational BehaviorOvi KumariNo ratings yet

- Ra 10863 - CmtaDocument134 pagesRa 10863 - CmtaRobert MaestreNo ratings yet

- Econ2020a 14 ps04Document4 pagesEcon2020a 14 ps04samuelifamilyNo ratings yet

- Scopia Capital Presentation On Forest City Realty Trust, Aug. 2016Document19 pagesScopia Capital Presentation On Forest City Realty Trust, Aug. 2016Norman OderNo ratings yet

- Thc109 Week 9 LessonDocument4 pagesThc109 Week 9 LessonBella MariaNo ratings yet

- Ethical Dillema in BusinessDocument2 pagesEthical Dillema in BusinesscharlesNo ratings yet