You might also like

- Notes On Management AccountingDocument71 pagesNotes On Management AccountingKartikNo ratings yet

- Analysis of Financial StatementsDocument17 pagesAnalysis of Financial StatementsRajesh PatilNo ratings yet

- Chapter # 5 Financial RatiosDocument30 pagesChapter # 5 Financial RatiosRooh Ullah KhanNo ratings yet

- Unit 2 Ratio Analysis ProblemsDocument14 pagesUnit 2 Ratio Analysis ProblemsGOKUL SNo ratings yet

- Afm - Ratio Analysis TheoryDocument12 pagesAfm - Ratio Analysis TheoryMr. N. KARTHIKEYAN Asst Prof MBANo ratings yet

- Ratio AnalysisDocument16 pagesRatio Analysisabhishekanandsingh123goNo ratings yet

- Ratio AnalysisDocument34 pagesRatio AnalysisAll TrendsNo ratings yet

- Chapter 2 - Financial AnalysisDocument66 pagesChapter 2 - Financial AnalysisRAHKAESH NAIR A L UTHAIYA NAIR100% (1)

- Ratio AnalysisDocument9 pagesRatio AnalysisCrazy electroNo ratings yet

- Liquidity RatiosDocument14 pagesLiquidity RatiosAnon sonNo ratings yet

- Balance SheetDocument20 pagesBalance SheetMarie FeNo ratings yet

- Financial Statements and AnalysisDocument48 pagesFinancial Statements and AnalysiskEBAY100% (1)

- Topic 1 - The Accounting EquationDocument10 pagesTopic 1 - The Accounting Equationgabriellemorgan714No ratings yet

- Befa Unit - VDocument22 pagesBefa Unit - VMahesh BabuNo ratings yet

- Unit 2 Financial Statement AnalysisDocument17 pagesUnit 2 Financial Statement AnalysisalemayehuNo ratings yet

- MA-Ratio AnalysisDocument74 pagesMA-Ratio AnalysisShobhita AgarwalNo ratings yet

- Liquidity NumericalsDocument8 pagesLiquidity Numericalspre.meh21No ratings yet

- Basic Financial StatementsDocument20 pagesBasic Financial StatementsRumel DeyNo ratings yet

- Statement of Financial Position (SFP) : TNHS Main - SHS - Accountancy, Business and ManagementDocument10 pagesStatement of Financial Position (SFP) : TNHS Main - SHS - Accountancy, Business and ManagementPedana RañolaNo ratings yet

- ISEM 530 ManagementDocument6 pagesISEM 530 ManagementNaren ReddyNo ratings yet

- 2203 Week 5 TemplateDocument39 pages2203 Week 5 TemplateHORTENSENo ratings yet

- Statement of Financial PositionDocument10 pagesStatement of Financial Positionmark jim toreroNo ratings yet

- Module 1 Statement of Financial PositionDocument4 pagesModule 1 Statement of Financial PositionWella LozadaNo ratings yet

- Ratio Analysis SRKDocument61 pagesRatio Analysis SRKsrkwin6No ratings yet

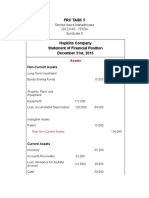

- FRC Task 5Document4 pagesFRC Task 5Denisa Naura MahadhiyasaNo ratings yet

- Financial Statements and Their Analysis - Service and Merchandising BusinessDocument21 pagesFinancial Statements and Their Analysis - Service and Merchandising BusinessJoana Marie DonatoNo ratings yet

- Short Term Liquidity Ratios Activity IIDocument7 pagesShort Term Liquidity Ratios Activity IIZarish AzharNo ratings yet

- Principles of Accounting Second Year, Semester 1Document38 pagesPrinciples of Accounting Second Year, Semester 1Sara Abdelrahim MakkawiNo ratings yet

- Module 4 - Financial Statement Analysis Lecture S23Document25 pagesModule 4 - Financial Statement Analysis Lecture S23Prachi YadavNo ratings yet

- The Accounting Equation (Financial Accounting)Document5 pagesThe Accounting Equation (Financial Accounting)RidwanAbirNo ratings yet

- Liquidity RatioDocument15 pagesLiquidity RatioLovely Joy CruzNo ratings yet

- L02 App of Acc Equation Wo ExerciseDocument7 pagesL02 App of Acc Equation Wo ExercisecalebNo ratings yet

- XII-ACCOUNT L DeshettyDocument5 pagesXII-ACCOUNT L DeshettyL DeshettyNo ratings yet

- Statement of Financial PositionDocument7 pagesStatement of Financial PositionJay KwonNo ratings yet

- Ch02TheAccountingEquation Exercise SolutionsDocument12 pagesCh02TheAccountingEquation Exercise Solutionsobiscarsgovroom123No ratings yet

- CHAPTER 3 - Accounting EquationDocument40 pagesCHAPTER 3 - Accounting EquationLAI WEI,No ratings yet

- Bank Financial Statements 2020 SDocument54 pagesBank Financial Statements 2020 SSuvajitLaikNo ratings yet

- Student's Learning Activity in FUNDAMENTALS OF Accountancy Business and Management 2Document5 pagesStudent's Learning Activity in FUNDAMENTALS OF Accountancy Business and Management 2Shelly RhychaelleNo ratings yet

- Accounting Equation (Edited)Document32 pagesAccounting Equation (Edited)Nor Zarina MohamadNo ratings yet

- Statement of Financial Position: Learning CompetenciesDocument9 pagesStatement of Financial Position: Learning CompetenciesJmaseNo ratings yet

- Management Accounting - Fund Flow AnalysisDocument30 pagesManagement Accounting - Fund Flow AnalysisT S Kumar KumarNo ratings yet

- Unit-5 Mefa.Document12 pagesUnit-5 Mefa.Perumalla AkhilNo ratings yet

- Question No. 2 Current RatioDocument4 pagesQuestion No. 2 Current Ratioknvs sivakumarNo ratings yet

- Lesson Eleven-AccountingDocument9 pagesLesson Eleven-AccountingKovács Zsuzsanna BorókaNo ratings yet

- Basic Elements of AccountingDocument10 pagesBasic Elements of AccountingMahmudul Hassan RohidNo ratings yet

- Statement of Financial Position, Also Referred To As The Balance SheetDocument7 pagesStatement of Financial Position, Also Referred To As The Balance SheetRhonamae GabisanNo ratings yet

- R22 Financial Statement Analysis IFT NotesDocument15 pagesR22 Financial Statement Analysis IFT NotesIndustrial Trainig EAGNo ratings yet

- Chap 3 Accounting Classification & Equation (Basic+Expended) - ClassDocument37 pagesChap 3 Accounting Classification & Equation (Basic+Expended) - Classnabkill100% (1)

- Discussion Question #5 Solution-Table 1.0 Shows The Order of Current Assets in Terms of Liquidity (Most To Least) Current AssetsDocument7 pagesDiscussion Question #5 Solution-Table 1.0 Shows The Order of Current Assets in Terms of Liquidity (Most To Least) Current AssetsRijul DUbeyNo ratings yet

- Balance Sheet Practice WorkbookDocument7 pagesBalance Sheet Practice WorkbookBJNo ratings yet

- Management Accounting (BBA32) - Unit - II& III: Accounting For Managerial DecisionDocument30 pagesManagement Accounting (BBA32) - Unit - II& III: Accounting For Managerial DecisionT S Kumar KumarNo ratings yet

- Module 1 - Lesson 4Document6 pagesModule 1 - Lesson 4Mai RuizNo ratings yet

- Lesson 1Document31 pagesLesson 1Rowena HinumlaNo ratings yet

- 2-Balance Sheet PDFDocument44 pages2-Balance Sheet PDFDiane ApostolNo ratings yet

- Accountancy: Shaheen Falcons Pu CollegeDocument13 pagesAccountancy: Shaheen Falcons Pu CollegeMohammed RayyanNo ratings yet

- 2 Understanding Financial Information-1Document32 pages2 Understanding Financial Information-1Tijana DjurdjevicNo ratings yet

- Topic3 S Balance SheetDocument10 pagesTopic3 S Balance SheetWei ZhangNo ratings yet

- Fundamentals of Accounting, Business and Management 2: Most Essential Learning CompetenciesDocument5 pagesFundamentals of Accounting, Business and Management 2: Most Essential Learning CompetenciesHazel ZabellaNo ratings yet

- 1st Assignment - 2023Document15 pages1st Assignment - 2023harmanchahalNo ratings yet

- U3 CostAccountancyDocument57 pagesU3 CostAccountancyvivekprasath soundararajanNo ratings yet

- U5 MarketingDocument70 pagesU5 Marketingvivekprasath soundararajanNo ratings yet

- U4-Company AccountsDocument42 pagesU4-Company Accountsvivekprasath soundararajanNo ratings yet

- U1 FinalAccountsDocument79 pagesU1 FinalAccountsvivekprasath soundararajanNo ratings yet

- MCQ U1 AccDocument3 pagesMCQ U1 Accvivekprasath soundararajanNo ratings yet

- MCQ ASP - NetMVCDocument29 pagesMCQ ASP - NetMVCvivekprasath soundararajanNo ratings yet

- 02536873Document2 pages02536873vivekprasath soundararajanNo ratings yet

- CDocument4 pagesCvivekprasath soundararajanNo ratings yet

- 2 AllRecord Page HTML CodeDocument2 pages2 AllRecord Page HTML Codevivekprasath soundararajanNo ratings yet

- 2 AllRecord Page HTML CodeDocument2 pages2 AllRecord Page HTML Codevivekprasath soundararajanNo ratings yet

- 1 Welcome Page HTML CodeDocument2 pages1 Welcome Page HTML Codevivekprasath soundararajanNo ratings yet

- CDocument4 pagesCvivekprasath soundararajanNo ratings yet

- ADocument2 pagesAvivekprasath soundararajanNo ratings yet

- 1 Welcome Page HTML CodeDocument2 pages1 Welcome Page HTML Codevivekprasath soundararajanNo ratings yet

- CDocument4 pagesCvivekprasath soundararajanNo ratings yet

- 1 Welcome Page HTML CodeDocument2 pages1 Welcome Page HTML Codevivekprasath soundararajanNo ratings yet

- Create LawDocument47 pagesCreate LawRen Mar CruzNo ratings yet

- Fit Income TaxDocument8 pagesFit Income TaxadrianoedwardjosephNo ratings yet

- Lesson 4 Business Income and Income From Exercise of ProfessionDocument52 pagesLesson 4 Business Income and Income From Exercise of ProfessionAngelica Faith MorcoNo ratings yet

- Solution Manual For Advanced Accounting 14th Edition Joe Ben Hoyle Thomas Schaefer Timothy DoupnikDocument39 pagesSolution Manual For Advanced Accounting 14th Edition Joe Ben Hoyle Thomas Schaefer Timothy DoupnikMariaPetersonewjkf100% (79)

- Cases in Tax ReviewDocument173 pagesCases in Tax ReviewErmawooNo ratings yet

- TAXATION NOTES Partnership To Special CorporationDocument10 pagesTAXATION NOTES Partnership To Special CorporationRose Neil LapuzNo ratings yet

- Income Taxation Manual - CH12Document28 pagesIncome Taxation Manual - CH12Roxan PacsayNo ratings yet

- Interim Financial ReportingDocument4 pagesInterim Financial Reportingbelle crisNo ratings yet

- Particle Board ProjectDocument28 pagesParticle Board ProjectSisay Tesfaye100% (1)

- H06 - Regular Income TaxationDocument7 pagesH06 - Regular Income Taxationnona galidoNo ratings yet

- Roxas v. CTA, 23 SCRA 331 - G.R. No. L-25043Document7 pagesRoxas v. CTA, 23 SCRA 331 - G.R. No. L-25043mhickey babonNo ratings yet

- Allowable Deductions NotesDocument5 pagesAllowable Deductions NotesPaula Mae DacanayNo ratings yet

- G.R. No. 136975. March 31, 2005. Commissioner of Internal Revenue, Petitioner, vs. HANTEX TRADING CO., INC., RespondentDocument33 pagesG.R. No. 136975. March 31, 2005. Commissioner of Internal Revenue, Petitioner, vs. HANTEX TRADING CO., INC., RespondentRae ManarNo ratings yet

- Notes Exam 2Document13 pagesNotes Exam 2Maria GabrielaNo ratings yet

- Sales Forecasting For Foodservice FacilitiesDocument5 pagesSales Forecasting For Foodservice FacilitiesRosemarie FloresNo ratings yet

- Quiz 2 - With AnswersDocument5 pagesQuiz 2 - With AnswersBABY JOY SEGUINo ratings yet

- Lumbera The Tax QueenDocument29 pagesLumbera The Tax QueenKristine MagbojosNo ratings yet

- Gross Income and Net IncomeDocument2 pagesGross Income and Net IncomeJasmine PeraltaNo ratings yet

- Taxation and Land Reform Final ExamDocument8 pagesTaxation and Land Reform Final ExamMeynard MagsinoNo ratings yet

- Other Percentage TaxesDocument34 pagesOther Percentage TaxesRose Diane CabiscuelasNo ratings yet

- Sahil (A.c) Final ProjectDocument57 pagesSahil (A.c) Final ProjectS JimudiyaNo ratings yet

- Bir Ruling Da C 296 727 09Document3 pagesBir Ruling Da C 296 727 09doraemoanNo ratings yet

- Materials For How To Handle BIR Audit Common Issues - 2021 Sept 21Document71 pagesMaterials For How To Handle BIR Audit Common Issues - 2021 Sept 21cool_peach100% (1)

- Business-Finance-Module 3Document8 pagesBusiness-Finance-Module 3Giezell BabiaNo ratings yet

- FY021 Introducttion To Business StudiesDocument13 pagesFY021 Introducttion To Business StudiesKamrul Islam SakibNo ratings yet

- Escudero CaseDocument24 pagesEscudero CaseWendy PeñafielNo ratings yet

- 47 Branch AccountsDocument53 pages47 Branch AccountsShivaram Krishnan70% (10)

- I. RR 4-11 Violates The Following Provisions of The NIRCDocument5 pagesI. RR 4-11 Violates The Following Provisions of The NIRCGabriel EmersonNo ratings yet

- FABM2 Q1 Mod2 Statement-Of-Comprehensive-Income v2Document24 pagesFABM2 Q1 Mod2 Statement-Of-Comprehensive-Income v2Neil Trezley Sunico BalajadiaNo ratings yet

- Ceylom Biscuit LimitedDocument24 pagesCeylom Biscuit LimitedLakshani fernandoNo ratings yet