You might also like

- Centrelink Authorisation Form ss313 - 1005enDocument6 pagesCentrelink Authorisation Form ss313 - 1005enWilliam Alister Young0% (1)

- Hyper Launch BrochureDocument22 pagesHyper Launch BrochureQuintin McDonaldNo ratings yet

- Compensating Controls & Preventive ControlsDocument7 pagesCompensating Controls & Preventive ControlsCA Harsh Tulsyan100% (2)

- Auditing Information Systems: Enhancing Performance of the EnterpriseFrom EverandAuditing Information Systems: Enhancing Performance of the EnterpriseNo ratings yet

- Effects of Computers On Internal ControlDocument53 pagesEffects of Computers On Internal ControlPia SurilNo ratings yet

- Financial Statements British English Student Ver2Document4 pagesFinancial Statements British English Student Ver2Paulo AbrantesNo ratings yet

- Upper Intermediate Unit Test 5: Grammar VocabularyDocument2 pagesUpper Intermediate Unit Test 5: Grammar VocabularyAléxia DinizNo ratings yet

- Internal Controls & IT RisksDocument7 pagesInternal Controls & IT RisksjhienellNo ratings yet

- Controlling CBIS Chapter 15Document5 pagesControlling CBIS Chapter 15blackphoenix303No ratings yet

- TranslateDocument5 pagesTranslateBeltsazar AlfeusNo ratings yet

- Topic 10 - The Impact of IT On Audit ProcessDocument34 pagesTopic 10 - The Impact of IT On Audit Process2022930579No ratings yet

- Lecture 8 9-CIS-revisedDocument159 pagesLecture 8 9-CIS-revisedIvanNo ratings yet

- Systems AuditDocument38 pagesSystems AuditSimon RuoroNo ratings yet

- Chapter 12 Solutions ManualDocument30 pagesChapter 12 Solutions ManualAndry Onix33% (3)

- Notes in Acctg 027 PrelimsDocument12 pagesNotes in Acctg 027 PrelimsJenny PadillaNo ratings yet

- Auditing in A Cis Environment: Controls, and Substantive Testing. An IT Audit Focuses On The Computer-Based Aspects ofDocument7 pagesAuditing in A Cis Environment: Controls, and Substantive Testing. An IT Audit Focuses On The Computer-Based Aspects ofPam HerreraNo ratings yet

- Hall Chapter 15Document10 pagesHall Chapter 15DaphneNo ratings yet

- Auditing in A Computer Information Systems (CIS) EnvironmentDocument4 pagesAuditing in A Computer Information Systems (CIS) EnvironmentxernathanNo ratings yet

- AEB14 SM CH12 v1Document32 pagesAEB14 SM CH12 v1RonLiu35No ratings yet

- Information Technology Audit: General PrinciplesDocument26 pagesInformation Technology Audit: General Principlesreema_rao_2No ratings yet

- Final PPT Week 13Document32 pagesFinal PPT Week 13nadxco 1711No ratings yet

- Cis FinalsDocument19 pagesCis FinalsVillena Divina VictoriaNo ratings yet

- Transcript of Chapter 22Document16 pagesTranscript of Chapter 22JoeNo ratings yet

- CHAPTER 7 AuditingDocument15 pagesCHAPTER 7 AuditingSebehat LeEgeziabeherNo ratings yet

- 18955sm Finalnew Isca Cp3Document120 pages18955sm Finalnew Isca Cp3lapogkNo ratings yet

- Auditing - Review Material 3Document9 pagesAuditing - Review Material 3KathleenNo ratings yet

- Third-Party Auditing For Small BusinessDocument4 pagesThird-Party Auditing For Small BusinessShielle AzonNo ratings yet

- Accounting Information System Notes: Collect, Store, Manage & Report Financial DataDocument8 pagesAccounting Information System Notes: Collect, Store, Manage & Report Financial DataIbrahimm Denis FofanahNo ratings yet

- Auditing IT Systems Under 40 CharactersDocument45 pagesAuditing IT Systems Under 40 CharactersRENATO CAPUNONo ratings yet

- S I A (SIA) 14 I A I T E: Tandard On Nternal Udit Nternal Udit in An Nformation Echnology NvironmentDocument12 pagesS I A (SIA) 14 I A I T E: Tandard On Nternal Udit Nternal Udit in An Nformation Echnology NvironmentDivine Epie Ngol'esuehNo ratings yet

- SM-15-new CHAPTER 15Document41 pagesSM-15-new CHAPTER 15psbacloudNo ratings yet

- Pre 5 - Preliminary ExaminationDocument3 pagesPre 5 - Preliminary ExaminationMarivic TolinNo ratings yet

- Audit in Computerized Environment 2Document10 pagesAudit in Computerized Environment 2Nedelyn PedrenaNo ratings yet

- MODULE 4_Auditing in an IT EnvironmentDocument10 pagesMODULE 4_Auditing in an IT EnvironmentRafael GonzagaNo ratings yet

- IT Audit Basics - The IS Audit ProcessDocument4 pagesIT Audit Basics - The IS Audit ProcessLyle Walt0% (1)

- 20181211005-Rizkania Arum - Tugas SIA II Pert 10Document7 pages20181211005-Rizkania Arum - Tugas SIA II Pert 1020181211005 RIZKANIA ARUM PUTRINo ratings yet

- Lecture 2 - Auditing IT Governance ControlsDocument63 pagesLecture 2 - Auditing IT Governance ControlsLei CasipleNo ratings yet

- Information TechnologyDocument15 pagesInformation Technologyabebe kumelaNo ratings yet

- Auditing in Cis Environment 1Document17 pagesAuditing in Cis Environment 1bonnyme.00No ratings yet

- The Sintoque's move to e-commerce and potential audit challengesDocument3 pagesThe Sintoque's move to e-commerce and potential audit challengesRubiatul AdawiyahNo ratings yet

- Effect of Computers On Internal ControlDocument13 pagesEffect of Computers On Internal ControlAyessa Marie AngelesNo ratings yet

- MF0004 Set1Document5 pagesMF0004 Set1sonygt007No ratings yet

- Auditing in A Computer Information Systems EnvironmentDocument6 pagesAuditing in A Computer Information Systems Environmentdown_d_alley0% (1)

- Lecture 2 Auditing IT Governance ControlsDocument63 pagesLecture 2 Auditing IT Governance ControlsAldwin CalambaNo ratings yet

- AuditDocument3 pagesAuditChloe CataluñaNo ratings yet

- Document (8)Document3 pagesDocument (8)Mharvie Joy ClarosNo ratings yet

- Auditing IT Governance ControlsDocument44 pagesAuditing IT Governance ControlsEdemson NavalesNo ratings yet

- Information Systems Audit (Chapter 1)Document35 pagesInformation Systems Audit (Chapter 1)Usama MunirNo ratings yet

- Internal ControlsDocument11 pagesInternal ControlsEunice GloriaNo ratings yet

- Ethics, Fraud and Internal ControlDocument4 pagesEthics, Fraud and Internal ControlCjay Dolotina0% (1)

- Chapter 3 Covers Ethics, Fraud, and Internal ControlsDocument26 pagesChapter 3 Covers Ethics, Fraud, and Internal ControlsRiviera MehsNo ratings yet

- Structure of The Information Technology Function (SLIDE 4)Document6 pagesStructure of The Information Technology Function (SLIDE 4)WenjunNo ratings yet

- Untitled document-2Document2 pagesUntitled document-2GwynethNo ratings yet

- INFORMATIONS SYSTEMS AUDIT NOTES MucheluleDocument59 pagesINFORMATIONS SYSTEMS AUDIT NOTES MuchelulevortebognuNo ratings yet

- Internal Control and Accounting System DesignDocument3 pagesInternal Control and Accounting System DesignHafidzi DerahmanNo ratings yet

- Qna ch1Document4 pagesQna ch1sweethoney2869No ratings yet

- Chapter 1 Introduction On Is AuditDocument5 pagesChapter 1 Introduction On Is AuditSteffany RoqueNo ratings yet

- Separation of Duties Principles and ApplicationsDocument4 pagesSeparation of Duties Principles and ApplicationsmirmoinulNo ratings yet

- Auditing, Assurance and Internal ControlDocument11 pagesAuditing, Assurance and Internal ControlaminoacidNo ratings yet

- Chapter 7 - Control and Accounting Information SystemsDocument3 pagesChapter 7 - Control and Accounting Information SystemsLouBel100% (5)

- Implementation of a Central Electronic Mail & Filing StructureFrom EverandImplementation of a Central Electronic Mail & Filing StructureNo ratings yet

- Incident Management Process Guide For Information TechnologyFrom EverandIncident Management Process Guide For Information TechnologyNo ratings yet

- Information Systems Auditing: The IS Audit Study and Evaluation of Controls ProcessFrom EverandInformation Systems Auditing: The IS Audit Study and Evaluation of Controls ProcessRating: 3 out of 5 stars3/5 (2)

- Activity in E3 - LiabilitiesDocument9 pagesActivity in E3 - LiabilitiesPaupau100% (1)

- Actvity 4 in Auditing 4 - Biological AssetsDocument3 pagesActvity 4 in Auditing 4 - Biological AssetsPaupauNo ratings yet

- Implement Strategy StructureDocument21 pagesImplement Strategy StructurePaupau100% (1)

- Activity - Derivatives and Hedging Accounting (PFRS 9)Document8 pagesActivity - Derivatives and Hedging Accounting (PFRS 9)PaupauNo ratings yet

- Activity - Translation of Foreign Currency Financial Statements (PAS 21 & PAS 29)Document1 pageActivity - Translation of Foreign Currency Financial Statements (PAS 21 & PAS 29)PaupauNo ratings yet

- Accounting for Cash, Receivables and InventoriesDocument12 pagesAccounting for Cash, Receivables and InventoriesPaupau100% (1)

- Assessment No. 6 MAS 06 Standard Costing Multiple Choice Problems: Choose The Letter of The Correct AnswerDocument12 pagesAssessment No. 6 MAS 06 Standard Costing Multiple Choice Problems: Choose The Letter of The Correct AnswerPaupauNo ratings yet

- Audit 4 - Audit in Specialized IndustryDocument7 pagesAudit 4 - Audit in Specialized IndustryPaupauNo ratings yet

- Assignment On PCF and Bank ReconDocument2 pagesAssignment On PCF and Bank ReconPaupauNo ratings yet

- Activity - Consolidated Financial Statement - Part 2 (1) (REVIEWER MIDTERM0Document6 pagesActivity - Consolidated Financial Statement - Part 2 (1) (REVIEWER MIDTERM0PaupauNo ratings yet

- AFAR ReviewDocument11 pagesAFAR ReviewPaupauNo ratings yet

- Activity - Consolidated Financial Statement, Part 1 (REVIEWER MIDTERM)Document12 pagesActivity - Consolidated Financial Statement, Part 1 (REVIEWER MIDTERM)Paupau0% (1)

- Activity On Application ControlDocument5 pagesActivity On Application ControlPaupauNo ratings yet

- Activity 2 Audit On CISDocument4 pagesActivity 2 Audit On CISPaupauNo ratings yet

- Special Purpose Audit Procedures and ReportsDocument6 pagesSpecial Purpose Audit Procedures and ReportsPaupauNo ratings yet

- Answer in Prelim Exam E4.Document12 pagesAnswer in Prelim Exam E4.PaupauNo ratings yet

- Activity - Home Office, Branch Accounting & Business Combination (REVIEWER MIDTERM)Document11 pagesActivity - Home Office, Branch Accounting & Business Combination (REVIEWER MIDTERM)Paupau100% (1)

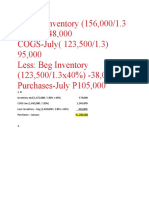

- Ending Inventory (156,000/1.3 x40%) P48,000 COGS-July (123,500/1.3) 95,000 Less: Beg Inventory (123,500/1.3x40%) - 38,000 Purchases-July P105,000Document1 pageEnding Inventory (156,000/1.3 x40%) P48,000 COGS-July (123,500/1.3) 95,000 Less: Beg Inventory (123,500/1.3x40%) - 38,000 Purchases-July P105,000PaupauNo ratings yet

- Activity 3 - CAATsDocument4 pagesActivity 3 - CAATsPaupauNo ratings yet

- Estimated transaction price methods and entries for consignment salesDocument7 pagesEstimated transaction price methods and entries for consignment salesPaupauNo ratings yet

- Answers - Partnership AccountingDocument14 pagesAnswers - Partnership AccountingPaupauNo ratings yet

- Actvity 4 in Auditing 4 - Biological AssetsDocument2 pagesActvity 4 in Auditing 4 - Biological AssetsPaupauNo ratings yet

- Home Office, Agency and Branch AccountingDocument17 pagesHome Office, Agency and Branch AccountingPaupauNo ratings yet

- Answer in Act. 2 For Cash-receivables-InventoriesDocument10 pagesAnswer in Act. 2 For Cash-receivables-InventoriesPaupauNo ratings yet

- MAS-04 Relevant CostingDocument10 pagesMAS-04 Relevant CostingPaupauNo ratings yet

- Management Accounting Techniques CompilationDocument40 pagesManagement Accounting Techniques CompilationGracelle Mae Oraller100% (1)

- 6 Business StrategyDocument27 pages6 Business StrategyPaupauNo ratings yet

- PAULA GOZUN - Activity 2 Accounting For Cash-receivables-InventoriesDocument9 pagesPAULA GOZUN - Activity 2 Accounting For Cash-receivables-InventoriesPaupauNo ratings yet

- Activity - Consolidated Financial Statement Part 1Document10 pagesActivity - Consolidated Financial Statement Part 1PaupauNo ratings yet

- Assessment No. 4 MAS-04 Relevant Costing I. Multiple Choice Theory: Choose The Letter of The Best AnswerDocument12 pagesAssessment No. 4 MAS-04 Relevant Costing I. Multiple Choice Theory: Choose The Letter of The Best AnswerPaupauNo ratings yet

- CRT 3rd Year NewDocument232 pagesCRT 3rd Year NewAkshat agrawalNo ratings yet

- 7 Eleven Store Nantun District - Google SearchDocument1 page7 Eleven Store Nantun District - Google SearchArleen MallillinNo ratings yet

- Target Market AnalysisDocument6 pagesTarget Market AnalysisAllyssa LaquindanumNo ratings yet

- New Invt MGT KesoramDocument69 pagesNew Invt MGT Kesoramtulasinad123No ratings yet

- Accounts PaperDocument2 pagesAccounts PaperRohan Ghadge-46No ratings yet

- Asialink Loan Application v7 FillableDocument2 pagesAsialink Loan Application v7 FillableJovelyn MarimonNo ratings yet

- Assessment On The Influence of Tax Education On Tax Compliance The Case Study of Tanzania Revenue Authority - Keko Bora Temeke BranchDocument33 pagesAssessment On The Influence of Tax Education On Tax Compliance The Case Study of Tanzania Revenue Authority - Keko Bora Temeke BranchSikudhani MmbagaNo ratings yet

- CHAPTER 1.1 Basic Concepts of ManagementsDocument15 pagesCHAPTER 1.1 Basic Concepts of ManagementsRay John DulapNo ratings yet

- Finance and Accounting - PPTX For FinalDocument18 pagesFinance and Accounting - PPTX For Finalmuqaddas bibiNo ratings yet

- Tax credit claim form guideDocument2 pagesTax credit claim form guideVivian KongNo ratings yet

- Andhra Pradesh Board Fee Payment FormDocument1 pageAndhra Pradesh Board Fee Payment FormM JEEVARATHNAM NAIDUNo ratings yet

- Critical Challenges Facing Small Business Enterprises in Nigeria A Literature ReviewDocument14 pagesCritical Challenges Facing Small Business Enterprises in Nigeria A Literature ReviewMuhammadNo ratings yet

- Responsibility AccountingDocument4 pagesResponsibility AccountingEllise FreniereNo ratings yet

- The Expenditure Cycle: Purchasing and Cash Disbursements: Magister Akuntansi PerbanasDocument24 pagesThe Expenditure Cycle: Purchasing and Cash Disbursements: Magister Akuntansi PerbanasTitan HerdiantoNo ratings yet

- reading_sample_sap_press_reporting_with_sap_s4hanaDocument32 pagesreading_sample_sap_press_reporting_with_sap_s4hanaCharles SantosNo ratings yet

- Contracts II AssignmentDocument16 pagesContracts II AssignmentIsha PuthettuNo ratings yet

- Befa Question BankDocument9 pagesBefa Question Bank20bd1a6655No ratings yet

- Borrowing Costs: DefinitionsDocument23 pagesBorrowing Costs: DefinitionsAbdul Sami100% (1)

- Communication Plan September 27Document24 pagesCommunication Plan September 27Rosemarie T. BrionesNo ratings yet

- Seminar On Central Bank of IndiaDocument23 pagesSeminar On Central Bank of IndiaHarshkinder SainiNo ratings yet

- Sustainbook PDFDocument225 pagesSustainbook PDFjNo ratings yet

- SHS Research Paper - Final 3Document57 pagesSHS Research Paper - Final 3Jaycee MeerandaNo ratings yet

- Terminate Utilities AccountDocument1 pageTerminate Utilities AccountVimal FranklinNo ratings yet

- Sales Receipt: Company Name 123 Main Street Hamilton, OH 44416 (321) 456-7890 Email AddressDocument1 pageSales Receipt: Company Name 123 Main Street Hamilton, OH 44416 (321) 456-7890 Email AddressParas ShardaNo ratings yet

- Real-Estate Investor's Psychology: Heuristics and Prospect FactorsDocument6 pagesReal-Estate Investor's Psychology: Heuristics and Prospect Factors03217925346No ratings yet

- Sample Paper Speaking BEC PreliminaryDocument2 pagesSample Paper Speaking BEC PreliminaryPham Van Khoa100% (1)