You might also like

- Esearch Eport: Riddhi Siddhi Gluco Biols LTDDocument9 pagesEsearch Eport: Riddhi Siddhi Gluco Biols LTDanny2k1No ratings yet

- Jyothy Laboratories LTD Accumulate: Retail Equity ResearchDocument5 pagesJyothy Laboratories LTD Accumulate: Retail Equity Researchkishor_warthi85No ratings yet

- Reliance Industries (RIL IN) : Q1FY21 Result UpdateDocument7 pagesReliance Industries (RIL IN) : Q1FY21 Result UpdatewhitenagarNo ratings yet

- ICICI Securities Galaxy Surfactant Q3FY23 ResultsDocument6 pagesICICI Securities Galaxy Surfactant Q3FY23 Resultssouheet.basuNo ratings yet

- Indian Oil Corporation: Interesting Times AheadDocument9 pagesIndian Oil Corporation: Interesting Times AheadNeelesh KumarNo ratings yet

- Q3FY19 Update Deepak Nitrite's Phenomenal PerformanceDocument6 pagesQ3FY19 Update Deepak Nitrite's Phenomenal Performance4nagNo ratings yet

- Nirmal Bang On United SpiritsDocument6 pagesNirmal Bang On United SpiritsamsukdNo ratings yet

- Godrej Agrovet: Higher Commodity Prices Weigh On PerformanceDocument12 pagesGodrej Agrovet: Higher Commodity Prices Weigh On Performancesonu kumarNo ratings yet

- 1182311122021672glenmark Pharma Q2FY22Document5 pages1182311122021672glenmark Pharma Q2FY22Prajwal JainNo ratings yet

- Gujarat Alkalies and Chemical Init Mar 19 IndiaDocument15 pagesGujarat Alkalies and Chemical Init Mar 19 IndiaDave LiNo ratings yet

- Agri Inputs: Sector Valuations Price in A Good SeasonDocument12 pagesAgri Inputs: Sector Valuations Price in A Good SeasonPrahladNo ratings yet

- Oil and Natural Gas CorporationDocument13 pagesOil and Natural Gas CorporationDHEERAJ RAJNo ratings yet

- Vinati Organics LTD: Expansions and New Project To Drive Earnings GrowthDocument6 pagesVinati Organics LTD: Expansions and New Project To Drive Earnings GrowthBhaveek OstwalNo ratings yet

- BPCL - Q1FY22 - MOStDocument10 pagesBPCL - Q1FY22 - MOStRahul JakhariaNo ratings yet

- Nuvama Initiating Coverage On United Breweries With 22% UPSIDE ADocument53 pagesNuvama Initiating Coverage On United Breweries With 22% UPSIDE Atakemederato1No ratings yet

- Unichem Lab (UNILAB) : On TrackDocument6 pagesUnichem Lab (UNILAB) : On Trackcos.secNo ratings yet

- FMCG 20101112 RelgareDocument6 pagesFMCG 20101112 RelgaremittleNo ratings yet

- Atul LTD Buy Report IIFLDocument6 pagesAtul LTD Buy Report IIFLBhaveek OstwalNo ratings yet

- Upll 2 8 20 PL PDFDocument9 pagesUpll 2 8 20 PL PDFwhitenagarNo ratings yet

- National Maize Equity Research - Jazira CapitalDocument9 pagesNational Maize Equity Research - Jazira CapitalMohamed FahmyNo ratings yet

- Sun Pharma: CMP: INR574 TP: INR675 (+18%)Document10 pagesSun Pharma: CMP: INR574 TP: INR675 (+18%)rishab agarwalNo ratings yet

- Aurobindo Pharma Maintains Strong Growth OutlookDocument9 pagesAurobindo Pharma Maintains Strong Growth Outlookjeetu16No ratings yet

- Grasim Industries Q3 Results Exceed Estimates on Higher IncomeDocument7 pagesGrasim Industries Q3 Results Exceed Estimates on Higher Incomecksharma68No ratings yet

- Final Deepak Fertilizers Petrochemicals LTDDocument9 pagesFinal Deepak Fertilizers Petrochemicals LTDbolinjkarvinitNo ratings yet

- GCPL Recovery Likely Q1FY21Document5 pagesGCPL Recovery Likely Q1FY21anjugaduNo ratings yet

- Alkyl Amines Report 2020Document7 pagesAlkyl Amines Report 2020SRINIVASAN TNo ratings yet

- Birla-Corporation-Limited 204 QuarterUpdateDocument8 pagesBirla-Corporation-Limited 204 QuarterUpdatearif420_999No ratings yet

- CEAT Annual Report 2019Document5 pagesCEAT Annual Report 2019Roberto GrilliNo ratings yet

- Confidence Petroleum India 020119Document17 pagesConfidence Petroleum India 020119saran21No ratings yet

- Vinati Organics: CMP: INR1,959 at The Threshold of Next-Level GrowthDocument14 pagesVinati Organics: CMP: INR1,959 at The Threshold of Next-Level GrowthVickey KrisNo ratings yet

- Tata Chemicals LTD: 12-Feb-2008 Pioneer Intermediaries PVT LTD - Agarwalla, AshwaniDocument32 pagesTata Chemicals LTD: 12-Feb-2008 Pioneer Intermediaries PVT LTD - Agarwalla, Ashwaniapi-3828752No ratings yet

- BUY Binani Cement LTD.: - Institutional ResearchDocument16 pagesBUY Binani Cement LTD.: - Institutional Researchbsaurabh2002No ratings yet

- Strong operating performance boosts Jyothy Laboratories to BuyDocument4 pagesStrong operating performance boosts Jyothy Laboratories to BuyjeetchauhanNo ratings yet

- UltratechCement Edel 190118Document15 pagesUltratechCement Edel 190118suprabhattNo ratings yet

- Equirus Securities Initiating Coverage GAEX 08.01.2018-Gujarat Ambuja ExportsDocument41 pagesEquirus Securities Initiating Coverage GAEX 08.01.2018-Gujarat Ambuja Exportsrchawdhry123100% (2)

- Hindustan Petroleum Corporation: Strong FootholdDocument9 pagesHindustan Petroleum Corporation: Strong FootholdumaganNo ratings yet

- Greenply Industries: Plywood Business Growing in Single-DigitsDocument8 pagesGreenply Industries: Plywood Business Growing in Single-Digitssaran21No ratings yet

- Hindustan Unilever: Better Performance in An Uncertain EnvironmentDocument7 pagesHindustan Unilever: Better Performance in An Uncertain EnvironmentUTSAVNo ratings yet

- Stock Update: Greaves CottonDocument3 pagesStock Update: Greaves CottonanjugaduNo ratings yet

- United Spirits Report - MotilalDocument12 pagesUnited Spirits Report - Motilalzaheen_1No ratings yet

- Bajaj Hindusthan: Performance HighlightsDocument9 pagesBajaj Hindusthan: Performance HighlightsAshish PokharnaNo ratings yet

- Deepak Nitrite - Initiation Report Asit Mehta Jan 2017Document20 pagesDeepak Nitrite - Initiation Report Asit Mehta Jan 2017divya chawlaNo ratings yet

- SKP Sec-Balrampur (Init Cov) - 2012Document12 pagesSKP Sec-Balrampur (Init Cov) - 2012rchawdhry123No ratings yet

- JKLakshmi Cem Geojit 070218Document5 pagesJKLakshmi Cem Geojit 070218suprabhattNo ratings yet

- Jyothy Laboratories Q4FY17 revenue up 4Document5 pagesJyothy Laboratories Q4FY17 revenue up 4Viju K GNo ratings yet

- Sumitomo Chemicals India LTD: Emerging MNC Proxy in Indian CPC Growth StoryDocument28 pagesSumitomo Chemicals India LTD: Emerging MNC Proxy in Indian CPC Growth StorySasidhar ThamilNo ratings yet

- Group 3 - Praj IndustriesDocument9 pagesGroup 3 - Praj IndustriesAayushi ChandwaniNo ratings yet

- FOCUS - Indofood Sukses Makmur: Saved by The GreenDocument10 pagesFOCUS - Indofood Sukses Makmur: Saved by The GreenriskaNo ratings yet

- Aarti Industries - 3QFY20 Result - RsecDocument7 pagesAarti Industries - 3QFY20 Result - RsecdarshanmaldeNo ratings yet

- Sun Pharma: Promising Specialty PipelineDocument8 pagesSun Pharma: Promising Specialty PipelineDinesh ChoudharyNo ratings yet

- HSIE Results Daily - 04 August 21-202108040822126132901Document9 pagesHSIE Results Daily - 04 August 21-202108040822126132901Michelle CastelinoNo ratings yet

- StarCement Q3FY24ResultReview8Feb24 ResearchDocument9 pagesStarCement Q3FY24ResultReview8Feb24 Researchvarunkul2337No ratings yet

- ERIS LIFESCIENCES Q1 EARNINGS REVIEWDocument6 pagesERIS LIFESCIENCES Q1 EARNINGS REVIEWYogi173No ratings yet

- Escorts: Expectation of Significant Recovery Due To A Better Monsoon BuyDocument7 pagesEscorts: Expectation of Significant Recovery Due To A Better Monsoon BuynnsriniNo ratings yet

- Aarti Industries: All Round Growth ImminentDocument13 pagesAarti Industries: All Round Growth ImminentPratik ChhedaNo ratings yet

- CFA RC 2016 Mongolia National University MongoliaDocument32 pagesCFA RC 2016 Mongolia National University MongoliaoyunnominNo ratings yet

- Nirmal Bang PDFDocument11 pagesNirmal Bang PDFBook MonkNo ratings yet

- Jubilant Life Sciences: CMP: INR809 Across-The-Board Traction Strengthening Growth StoryDocument10 pagesJubilant Life Sciences: CMP: INR809 Across-The-Board Traction Strengthening Growth StorymilandeepNo ratings yet

- Solar Powered Agro Industrial Project of Cassava Based Bioethanol Processing UnitFrom EverandSolar Powered Agro Industrial Project of Cassava Based Bioethanol Processing UnitNo ratings yet

- Reaching Zero with Renewables: Biojet FuelsFrom EverandReaching Zero with Renewables: Biojet FuelsNo ratings yet

- Groww Digest - 02 August 2021Document8 pagesGroww Digest - 02 August 2021Tejesh GoudNo ratings yet

- Groww Digest - 29 July 2021Document6 pagesGroww Digest - 29 July 2021Tejesh GoudNo ratings yet

- Groww Digest - 28 July 2021Document8 pagesGroww Digest - 28 July 2021Tejesh GoudNo ratings yet

- Identify Bad StocksDocument10 pagesIdentify Bad StocksTejesh GoudNo ratings yet

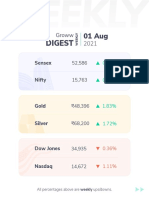

- Digest: Sensex NiftyDocument4 pagesDigest: Sensex NiftyTejesh GoudNo ratings yet

- Groww Digest - 03 August 2021Document5 pagesGroww Digest - 03 August 2021Tejesh GoudNo ratings yet

- What Is Happening With The API Companies?Document23 pagesWhat Is Happening With The API Companies?Tejesh GoudNo ratings yet

- Groww Digest - 30 July 2021Document10 pagesGroww Digest - 30 July 2021Tejesh GoudNo ratings yet

- Bikaji Foods International Limited DRHPDocument433 pagesBikaji Foods International Limited DRHPTejesh GoudNo ratings yet

- Globus SpiritsDocument5 pagesGlobus SpiritsTejesh GoudNo ratings yet

- Rolex Rings IPODocument4 pagesRolex Rings IPOTejesh GoudNo ratings yet

- IPO Diary Feb'2022Document89 pagesIPO Diary Feb'2022Tejesh GoudNo ratings yet

- Globus Con CallDocument15 pagesGlobus Con CallTejesh GoudNo ratings yet

- IS Ev Ready?: Anish Moonka, Head of Research, JST InvestmentsDocument30 pagesIS Ev Ready?: Anish Moonka, Head of Research, JST InvestmentsTejesh GoudNo ratings yet

- HDFC MF Yearbook 2022Document88 pagesHDFC MF Yearbook 2022Tejesh GoudNo ratings yet

- AGS Transact Technologies LTD - IPO Note - Jan'2022Document10 pagesAGS Transact Technologies LTD - IPO Note - Jan'2022Tejesh GoudNo ratings yet

- Budget Expectations 2022-23 - Axis Sec - 210122Document25 pagesBudget Expectations 2022-23 - Axis Sec - 210122Tejesh GoudNo ratings yet

- ANTONY WASTE HSL Initiating Coverage 190122Document17 pagesANTONY WASTE HSL Initiating Coverage 190122Tejesh GoudNo ratings yet

- Paytm by MacquarieDocument8 pagesPaytm by MacquarieTejesh GoudNo ratings yet

- Budget SpeechDocument38 pagesBudget SpeechNDTVNo ratings yet

- Adani Wilmar IPO NoteDocument19 pagesAdani Wilmar IPO NoteTejesh GoudNo ratings yet

- Automobiles SectorDocument45 pagesAutomobiles SectorTejesh GoudNo ratings yet

- Jefferies On Metal StocksDocument36 pagesJefferies On Metal StocksTejesh GoudNo ratings yet

- National Stock Exchange of India Limited BSE LimitedDocument2 pagesNational Stock Exchange of India Limited BSE LimitedTejesh GoudNo ratings yet

- How To Calculate Your Actual: Return On Investment For Sips?Document5 pagesHow To Calculate Your Actual: Return On Investment For Sips?Tejesh GoudNo ratings yet

- Is It Wise To Invest In: Debt-Free Stocks?Document6 pagesIs It Wise To Invest In: Debt-Free Stocks?Tejesh GoudNo ratings yet

- INDIAN HOTELS - Initiating CoverageDocument30 pagesINDIAN HOTELS - Initiating CoverageTejesh GoudNo ratings yet

- SBI Cards & Payment Services LTD.: Triple Headwinds Cast Shadow On Growth Momentum Initiate at SellDocument39 pagesSBI Cards & Payment Services LTD.: Triple Headwinds Cast Shadow On Growth Momentum Initiate at SellTejesh GoudNo ratings yet

- How To Build A Well-Diversified PortfolioDocument5 pagesHow To Build A Well-Diversified PortfolioTejesh GoudNo ratings yet

- Rosario + Vampire JumpchainDocument16 pagesRosario + Vampire Jumpchaind7an7pijpker100% (1)

- Experiment vs experience guideDocument30 pagesExperiment vs experience guideNandar Min HtetNo ratings yet

- Behind The HaloDocument2 pagesBehind The HaloGiang Nguyễn TrườngNo ratings yet

- International Dairy Journal: Sabrina P. Van Den Oever, Helmut K. MayerDocument21 pagesInternational Dairy Journal: Sabrina P. Van Den Oever, Helmut K. MayerwulanesterNo ratings yet

- Course Catalog: Specialty Coffee AssociationDocument14 pagesCourse Catalog: Specialty Coffee AssociationWael KhatibNo ratings yet

- Anita Herbert Food Swap Table UPDATE 0621-210712-191020Document18 pagesAnita Herbert Food Swap Table UPDATE 0621-210712-191020Theresa CostelloNo ratings yet

- Cookery Lesson PlanDocument6 pagesCookery Lesson PlanLaine AcainNo ratings yet

- The Penguin Book of Japanese Short Stories (PDFDrive) - 159-164Document6 pagesThe Penguin Book of Japanese Short Stories (PDFDrive) - 159-164Prita Setya MaharaniNo ratings yet

- Case Study-CoffeeDocument13 pagesCase Study-CoffeeMalik ArslanNo ratings yet

- Pathfinder Honor On PoultryDocument14 pagesPathfinder Honor On Poultryjustus nyakundiNo ratings yet

- Nptanc Assignment 3Document7 pagesNptanc Assignment 3Nu Ngoc Nhu TranNo ratings yet

- Consumer Trends 2023Document88 pagesConsumer Trends 2023Rafael AguiarNo ratings yet

- Biological Molecules 2 QPDocument12 pagesBiological Molecules 2 QPApdiweli AliNo ratings yet

- EL111 Vocabulary ListDocument7 pagesEL111 Vocabulary Listyoussef.turki2001No ratings yet

- Frozen DessertsDocument27 pagesFrozen DessertsMA. NECOLE JEREMIAH GONZALESNo ratings yet

- DIRTY LAZY KETO Getting StartedDocument131 pagesDIRTY LAZY KETO Getting StartedGabriel Johnson80% (5)

- Name: Grade: Phone: SMPN 23 Kota BekasiDocument4 pagesName: Grade: Phone: SMPN 23 Kota BekasiAditya AndikaNo ratings yet

- Adobe Scan 13-Jul-2021Document22 pagesAdobe Scan 13-Jul-2021Poonam SinghNo ratings yet

- Ocloo Lily Project Work HND 23Document30 pagesOcloo Lily Project Work HND 23Eugene Amarh AmarteyNo ratings yet

- YS1 Consolidation Unit7 PDFDocument2 pagesYS1 Consolidation Unit7 PDFLouise F. de CastroNo ratings yet

- Lesson 1 Baking IngredientsDocument33 pagesLesson 1 Baking IngredientsLovely Sunga-AlboroteNo ratings yet

- Project Report On Agri Tourism: Submitted byDocument16 pagesProject Report On Agri Tourism: Submitted bysaumikdebNo ratings yet

- Bing 2022Document6 pagesBing 2022Elisa NovianiNo ratings yet

- Poverty Estimation Methods in Rural IndiaDocument9 pagesPoverty Estimation Methods in Rural IndiaVenkateswaran RamaswamyNo ratings yet

- Foam Mat Drying TechniqueDocument22 pagesFoam Mat Drying TechniqueMariah SadafNo ratings yet

- Kompotensi Dasar: Explanation TextDocument21 pagesKompotensi Dasar: Explanation TextSakina UtinaNo ratings yet

- Raw Vegan IndianDocument57 pagesRaw Vegan IndianallyaNo ratings yet

- The Digestive System and Body Metabolism: Part BDocument29 pagesThe Digestive System and Body Metabolism: Part Bim. EliasNo ratings yet

- Ruminal Acidosis Aetiopathogenesis Prevention and TreatmentDocument60 pagesRuminal Acidosis Aetiopathogenesis Prevention and TreatmentDavid uribeNo ratings yet

- Please Purchase The Apple Cider Vinegar in Glass Containers: Why Stomach Acid Deficiency HappensDocument3 pagesPlease Purchase The Apple Cider Vinegar in Glass Containers: Why Stomach Acid Deficiency HappensyahyoushNo ratings yet