You might also like

- MoLex Leading A Tech StartupDocument8 pagesMoLex Leading A Tech StartupManojKumarGaliNo ratings yet

- Grameen BankDocument5 pagesGrameen BankNitin ChidrawarNo ratings yet

- Art of Investing - Its Simple But Not Easy by Ravi Dharamshi PDFDocument48 pagesArt of Investing - Its Simple But Not Easy by Ravi Dharamshi PDFPranavPillaiNo ratings yet

- Indian Institute of Management Kozhikode:: Roll - No - Name - Section - CoursenameDocument6 pagesIndian Institute of Management Kozhikode:: Roll - No - Name - Section - CoursenameAnushkaNo ratings yet

- Sustainable Finance: The Imperative and The OpportunityDocument70 pagesSustainable Finance: The Imperative and The OpportunityNidia Liliana TovarNo ratings yet

- Comptek Solutions Investor DeckDocument17 pagesComptek Solutions Investor DeckCarl D'heerNo ratings yet

- The Intentional Apartment Developer: A Programmatic Guide for Planning, Designing, Building, Leasing, Managing, and SellingFrom EverandThe Intentional Apartment Developer: A Programmatic Guide for Planning, Designing, Building, Leasing, Managing, and SellingNo ratings yet

- Bank of Nova Scotia Brand AnalysisDocument11 pagesBank of Nova Scotia Brand AnalysisAshik Paul0% (1)

- RESOURCE AUDIT PERFORMA (Tesco)Document2 pagesRESOURCE AUDIT PERFORMA (Tesco)Balogun Temitope100% (1)

- MGM Stock PitchDocument1 pageMGM Stock Pitchapi-545367999No ratings yet

- Xing 1Document45 pagesXing 1tempguy7369No ratings yet

- World Gold Analyst - Zimbabwe Special Report September 2010Document100 pagesWorld Gold Analyst - Zimbabwe Special Report September 2010dshornikovNo ratings yet

- Nubank: Valued at US$25bn in A Series G Raise of US$400mn IPO Ever CloserDocument5 pagesNubank: Valued at US$25bn in A Series G Raise of US$400mn IPO Ever CloserFelipe AreiaNo ratings yet

- Bain IVCA India Venture Capital Report 2022 1648706342Document42 pagesBain IVCA India Venture Capital Report 2022 1648706342Kiran MaadamshettiNo ratings yet

- Deloitte Uk Fs Marketplace LendingDocument44 pagesDeloitte Uk Fs Marketplace LendingCrowdFunding BeatNo ratings yet

- Project and Infrastructure Finance: PressDocument36 pagesProject and Infrastructure Finance: PressmansiNo ratings yet

- Brand Hijack (Review and Analysis of Wipperfurth's Book)From EverandBrand Hijack (Review and Analysis of Wipperfurth's Book)Rating: 1 out of 5 stars1/5 (1)

- Roland Berger Study Banking Myanmar Sept PDFDocument28 pagesRoland Berger Study Banking Myanmar Sept PDFYosia SuhermanNo ratings yet

- Business Week 03 Oct 2005Document82 pagesBusiness Week 03 Oct 2005Anand AgrawalNo ratings yet

- American Cancer Society CaseDocument13 pagesAmerican Cancer Society CaseAnimesh KumarNo ratings yet

- Pleasure Scooter CaseDocument25 pagesPleasure Scooter CaseKabeer KarnaniNo ratings yet

- Financial Ratio DataDocument830 pagesFinancial Ratio DataColin-MatthewRosales100% (1)

- I Used Acorns, Robinhood, and Stash For 2 Years. This Is What I Learned and EarnedDocument8 pagesI Used Acorns, Robinhood, and Stash For 2 Years. This Is What I Learned and Earnedbarakasake300No ratings yet

- Toy Horse Conjoint Experiment: Case AssignmentDocument23 pagesToy Horse Conjoint Experiment: Case AssignmentwillowNo ratings yet

- Varanium 11042019Document25 pagesVaranium 11042019Rahul JainNo ratings yet

- De Clercq, (2006) An Entrepreneur's Guide To The Venture Capital GalaxyDocument7 pagesDe Clercq, (2006) An Entrepreneur's Guide To The Venture Capital GalaxyafghansherNo ratings yet

- 2019 AAA Green Car GuideDocument217 pages2019 AAA Green Car GuideIslam MohamedNo ratings yet

- Dobank Business PlanDocument7 pagesDobank Business PlanSankary CarollNo ratings yet

- Chia Tek YewDocument11 pagesChia Tek Yewherman wahyudiNo ratings yet

- 495 Course SyllabusDocument11 pages495 Course Syllabusmoshe feldmanNo ratings yet

- Behavioral Finance: Jay R. RitterDocument9 pagesBehavioral Finance: Jay R. RitterTehreema KazmiNo ratings yet

- Analysys Mason Country Reports Data SheetDocument2 pagesAnalysys Mason Country Reports Data SheetsmrilNo ratings yet

- RCL Stock PitchDocument1 pageRCL Stock Pitchapi-545367999No ratings yet

- Ritz CarltonDocument17 pagesRitz Carltonwajeeha javedNo ratings yet

- Financial Systems and Service CIA - Component 1Document18 pagesFinancial Systems and Service CIA - Component 1SIRISHA N 2010285No ratings yet

- E-Marketing and Performance of Small and Medium Enterprises in Bauchi MetropolisDocument11 pagesE-Marketing and Performance of Small and Medium Enterprises in Bauchi MetropolisInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- SMRT - Internal Crisis LeadershipDocument27 pagesSMRT - Internal Crisis Leadershipnidhi guptaNo ratings yet

- FP - CTS Report H1.21Document13 pagesFP - CTS Report H1.21William HarrisNo ratings yet

- Alcoholic Drinks in MexicoDocument40 pagesAlcoholic Drinks in MexicomusicrokNo ratings yet

- Case Study AnishaDocument4 pagesCase Study AnishaAnisha KirpalaniNo ratings yet

- Technological Pioneering and Competitive AdvantageDocument27 pagesTechnological Pioneering and Competitive AdvantageManinder KhuranaNo ratings yet

- 2 Kim Prior - FinTechDocument54 pages2 Kim Prior - FinTechSai Charan TejaNo ratings yet

- Marketing Research - Self Driving CarsDocument16 pagesMarketing Research - Self Driving CarsTeama DrockNo ratings yet

- Excetive SummryDocument11 pagesExcetive SummryMuhammad Hassan JavedNo ratings yet

- Stock Pitch AB InBev (1118)Document22 pagesStock Pitch AB InBev (1118)Vinay SohalNo ratings yet

- Fuwang and RAK Ceramics Ratio Analysis - Term Paper (2015-2019)Document28 pagesFuwang and RAK Ceramics Ratio Analysis - Term Paper (2015-2019)Md. Safatul BariNo ratings yet

- TWM WealTech Report - Digital Assets SeriesDocument46 pagesTWM WealTech Report - Digital Assets SeriesTrader CatNo ratings yet

- Public Listed IPO (TCS)Document6 pagesPublic Listed IPO (TCS)SatishNo ratings yet

- Sample ReportDocument25 pagesSample ReportTolga BilgiçNo ratings yet

- TTBS Sip FinalDocument19 pagesTTBS Sip Finalvaibhav chaurasiaNo ratings yet

- TWSS 6-Weeks-Full Time Program Brochure PDFDocument27 pagesTWSS 6-Weeks-Full Time Program Brochure PDFEshanMishraNo ratings yet

- Microsoft CSR CampaignDocument16 pagesMicrosoft CSR CampaignChristopher EckNo ratings yet

- LewisDocument1 pageLewisapi-523877663No ratings yet

- Selling To China Through Cross-Border E-CommerceDocument62 pagesSelling To China Through Cross-Border E-CommerceCNo ratings yet

- Ai PDFDocument65 pagesAi PDFKhadri MohammedNo ratings yet

- CS - Amber IC, Dixon IC - 8 Dec 2020 PDFDocument88 pagesCS - Amber IC, Dixon IC - 8 Dec 2020 PDFRanjan BeheraNo ratings yet

- Elixir CaseDocument11 pagesElixir CaseAnoushkaBanavarNo ratings yet

- Group 1 - Beeplus - CaseDocument13 pagesGroup 1 - Beeplus - CaseAditi JainNo ratings yet

- Studymaster PitchbookDocument17 pagesStudymaster Pitchbookapi-241338805No ratings yet

- What Is Happening With The API Companies?Document23 pagesWhat Is Happening With The API Companies?Tejesh GoudNo ratings yet

- Groww Digest - 29 July 2021Document6 pagesGroww Digest - 29 July 2021Tejesh GoudNo ratings yet

- Groww Digest - 30 July 2021Document10 pagesGroww Digest - 30 July 2021Tejesh GoudNo ratings yet

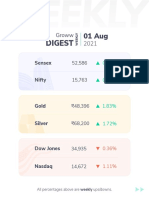

- Groww Digest - 02 August 2021Document8 pagesGroww Digest - 02 August 2021Tejesh GoudNo ratings yet

- Groww Digest - 03 August 2021Document5 pagesGroww Digest - 03 August 2021Tejesh GoudNo ratings yet

- Identify Bad StocksDocument10 pagesIdentify Bad StocksTejesh GoudNo ratings yet

- Digest: Sensex NiftyDocument4 pagesDigest: Sensex NiftyTejesh GoudNo ratings yet

- Globus SpiritsDocument5 pagesGlobus SpiritsTejesh GoudNo ratings yet

- Groww Digest - 28 July 2021Document8 pagesGroww Digest - 28 July 2021Tejesh GoudNo ratings yet

- Rolex Rings IPODocument4 pagesRolex Rings IPOTejesh GoudNo ratings yet

- Globus Con CallDocument15 pagesGlobus Con CallTejesh GoudNo ratings yet

- HDFC MF Yearbook 2022Document88 pagesHDFC MF Yearbook 2022Tejesh GoudNo ratings yet

- Bikaji Foods International Limited DRHPDocument433 pagesBikaji Foods International Limited DRHPTejesh GoudNo ratings yet

- IS Ev Ready?: Anish Moonka, Head of Research, JST InvestmentsDocument30 pagesIS Ev Ready?: Anish Moonka, Head of Research, JST InvestmentsTejesh GoudNo ratings yet

- AGS Transact Technologies LTD - IPO Note - Jan'2022Document10 pagesAGS Transact Technologies LTD - IPO Note - Jan'2022Tejesh GoudNo ratings yet

- ANTONY WASTE HSL Initiating Coverage 190122Document17 pagesANTONY WASTE HSL Initiating Coverage 190122Tejesh GoudNo ratings yet

- Adani Wilmar Limited IpoDocument19 pagesAdani Wilmar Limited IpoTejesh GoudNo ratings yet

- Automobiles SectorDocument45 pagesAutomobiles SectorTejesh GoudNo ratings yet

- Globus SpiritsDocument17 pagesGlobus SpiritsTejesh GoudNo ratings yet

- Budget SpeechDocument38 pagesBudget SpeechNDTVNo ratings yet

- IPO Diary Feb'2022Document89 pagesIPO Diary Feb'2022Tejesh GoudNo ratings yet

- Budget Expectations 2022-23 - Axis Sec - 210122Document25 pagesBudget Expectations 2022-23 - Axis Sec - 210122Tejesh GoudNo ratings yet

- National Stock Exchange of India Limited BSE LimitedDocument2 pagesNational Stock Exchange of India Limited BSE LimitedTejesh GoudNo ratings yet

- Jefferies On Metal StocksDocument36 pagesJefferies On Metal StocksTejesh GoudNo ratings yet

- SBI Cards & Payment Services LTD.: Triple Headwinds Cast Shadow On Growth Momentum Initiate at SellDocument39 pagesSBI Cards & Payment Services LTD.: Triple Headwinds Cast Shadow On Growth Momentum Initiate at SellTejesh GoudNo ratings yet

- INDIAN HOTELS - Initiating CoverageDocument30 pagesINDIAN HOTELS - Initiating CoverageTejesh GoudNo ratings yet

- How To Build A Well-Diversified PortfolioDocument5 pagesHow To Build A Well-Diversified PortfolioTejesh GoudNo ratings yet

- Is It Wise To Invest In: Debt-Free Stocks?Document6 pagesIs It Wise To Invest In: Debt-Free Stocks?Tejesh GoudNo ratings yet

- How To Calculate Your Actual: Return On Investment For Sips?Document5 pagesHow To Calculate Your Actual: Return On Investment For Sips?Tejesh GoudNo ratings yet

- Clause 49 of Listing AgreementDocument18 pagesClause 49 of Listing AgreementJatin AhujaNo ratings yet

- My Cash: Balance TotalDocument9 pagesMy Cash: Balance TotalDahlan MuksinNo ratings yet

- MODULE 14 Insurance Law EDITEDDocument25 pagesMODULE 14 Insurance Law EDITEDJocelyn GarnadoNo ratings yet

- Financial Planning and ForecastingDocument20 pagesFinancial Planning and ForecastingSyedMaazNo ratings yet

- Partnership AccountDocument9 pagesPartnership AccountBamidele AdegboyeNo ratings yet

- TENANCY AGREEMENT Pasar SegarDocument4 pagesTENANCY AGREEMENT Pasar SegarFade ChannelNo ratings yet

- Credit Union Performance - L Dean Odle 2Document2 pagesCredit Union Performance - L Dean Odle 2api-413534603No ratings yet

- Money: Money Is Any Item or Verifiable Record That Is Generally AcceptedDocument2 pagesMoney: Money Is Any Item or Verifiable Record That Is Generally AcceptedMokshi shahNo ratings yet

- City Limits Magazine, November 1979 IssueDocument24 pagesCity Limits Magazine, November 1979 IssueCity Limits (New York)No ratings yet

- SA13 Consulting Services WednesdayDocument31 pagesSA13 Consulting Services WednesdayAhmed AlyaniNo ratings yet

- CFA - Student PresentationDocument17 pagesCFA - Student PresentationJasmine Kaur100% (1)

- SP PaperDocument11 pagesSP Paper9137373282abcdNo ratings yet

- BUSI 3309 W24 Assignment 1Document6 pagesBUSI 3309 W24 Assignment 1faridahrushdy5No ratings yet

- Integrated Review Ceu PDFDocument28 pagesIntegrated Review Ceu PDFHello Kitty100% (1)

- Lembar Jawaban 2-BUKU BESARDocument13 pagesLembar Jawaban 2-BUKU BESAREnrico Jovian S SNo ratings yet

- Fauji Fertilizer Company LimitedDocument16 pagesFauji Fertilizer Company Limitedkhan izharNo ratings yet

- Mis 442Document9 pagesMis 442mirfaiyazkabir2000No ratings yet

- Security Bank V Cuenca DigestDocument3 pagesSecurity Bank V Cuenca DigestJermone MuaripNo ratings yet

- LJK UkkDocument55 pagesLJK UkkSaepul RohmanNo ratings yet

- Berkshire's Corporate Performance vs. The S&P 500Document23 pagesBerkshire's Corporate Performance vs. The S&P 500FirstpostNo ratings yet

- Report of Checks Issued 2023Document1 pageReport of Checks Issued 2023Jahzeel RubioNo ratings yet

- Print Reciept RequestDocument1 pagePrint Reciept RequestOgbesetuyi seun AugustineNo ratings yet

- Tata Steel - Q2FY23 Result Update - 02112022 - 02-11-2022 - 12Document9 pagesTata Steel - Q2FY23 Result Update - 02112022 - 02-11-2022 - 12AnirudhNo ratings yet

- Alanis Parks Department: Analyze and Chart Financial DataDocument7 pagesAlanis Parks Department: Analyze and Chart Financial DataJacob SheridanNo ratings yet

- Basic Details: Indian Oil Corporation Eprocurement PortalDocument3 pagesBasic Details: Indian Oil Corporation Eprocurement PortalamitjustamitNo ratings yet

- New Investment Supports SkySparc Growth StrategyDocument3 pagesNew Investment Supports SkySparc Growth StrategyPR.comNo ratings yet

- The Weekly Profile Guide - VDocument19 pagesThe Weekly Profile Guide - VJean TehNo ratings yet

- Lesson 1 ExtendDocument6 pagesLesson 1 ExtendRoel Cababao50% (2)

- Basic Property Cashflow SimulatorDocument2 pagesBasic Property Cashflow SimulatorBen BieberNo ratings yet

- PGI Sample QuestionDocument4 pagesPGI Sample QuestionleoneseNo ratings yet