You might also like

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- 4 - Financial StatementsDocument40 pages4 - Financial StatementsKei TamundongNo ratings yet

- Chapter 4Document4 pagesChapter 4mayhipolito01No ratings yet

- Chapter 1 - Introduction To Financial AccountingDocument60 pagesChapter 1 - Introduction To Financial Accountingnew rhondaldNo ratings yet

- Wlof Hsac Gnitarepo Gncinfina: Jumble LettersDocument23 pagesWlof Hsac Gnitarepo Gncinfina: Jumble LettersAce Soleil RiegoNo ratings yet

- ACCT CH4Document10 pagesACCT CH4Aseel Al NajraniNo ratings yet

- Financial Accounting BasicsDocument24 pagesFinancial Accounting BasicsMonirHRNo ratings yet

- Topic V - Statement of Cash FlowsDocument8 pagesTopic V - Statement of Cash FlowsSean William CareyNo ratings yet

- 1financial Statements and Financial Statement AnalysisDocument24 pages1financial Statements and Financial Statement AnalysisBenson NjorogeNo ratings yet

- Chapter 2-Accounting 101Document26 pagesChapter 2-Accounting 101Haidee SumampilNo ratings yet

- What Are The Parties Interested in Accounting?Document7 pagesWhat Are The Parties Interested in Accounting?Mohammad Zahirul IslamNo ratings yet

- Alwadi International School Accounting Grade 12 Notes: Statement of Cash FlowsDocument14 pagesAlwadi International School Accounting Grade 12 Notes: Statement of Cash FlowsFarrukhsgNo ratings yet

- 2.0 Accounting Defined: The American Institute of Certified Public Accountant HasDocument31 pages2.0 Accounting Defined: The American Institute of Certified Public Accountant HashellenNo ratings yet

- Finance 5Document3 pagesFinance 5Jheannie Jenly Mia SabulberoNo ratings yet

- Cash Flow AnalysisDocument15 pagesCash Flow AnalysisElvie Abulencia-BagsicNo ratings yet

- Chapter: Measurement and Reporting of Revenues and Expenses, Gains and LossesDocument13 pagesChapter: Measurement and Reporting of Revenues and Expenses, Gains and LossesNayanNo ratings yet

- Chapter 1 NotesDocument36 pagesChapter 1 NotesSina RahimiNo ratings yet

- Accounting Solutions To ExercisesDocument18 pagesAccounting Solutions To ExercisesJaveria SalmanNo ratings yet

- 10 Element of FRDocument12 pages10 Element of FRIloNo ratings yet

- Group 4 - Assignment 2Document14 pagesGroup 4 - Assignment 2Eiffelyn PutriNo ratings yet

- Financial StatementsDocument11 pagesFinancial StatementsMab ShiNo ratings yet

- Cash Flow Analysis GuideDocument15 pagesCash Flow Analysis Guidekyungsoo100% (1)

- Chap 4 - 7 KTTCDocument14 pagesChap 4 - 7 KTTCQuyên NguyễnNo ratings yet

- ACTBAS1 - Lesson 2 (Statement of Financial Position)Document47 pagesACTBAS1 - Lesson 2 (Statement of Financial Position)AyniNuydaNo ratings yet

- Formulas For Calculating FinanceDocument61 pagesFormulas For Calculating FinanceRukshar KhanNo ratings yet

- Accounting Review Material 2018Document10 pagesAccounting Review Material 2018Alex ComelingNo ratings yet

- Mid Term TopicsDocument10 pagesMid Term TopicsТемирлан АльпиевNo ratings yet

- Cash Flow StatemementsDocument31 pagesCash Flow StatemementsTasim Ishraque100% (1)

- Solutions Manual - Chapter 3Document7 pagesSolutions Manual - Chapter 3Renu TharshiniNo ratings yet

- Acc201 Su6Document15 pagesAcc201 Su6Gwyneth LimNo ratings yet

- Finance QuestionsDocument10 pagesFinance QuestionsAkash ChauhanNo ratings yet

- 2600 Legarda St. Sampaloc, Manila: Arellano University Juan Sumulong Campus Senior High School DepartmentDocument7 pages2600 Legarda St. Sampaloc, Manila: Arellano University Juan Sumulong Campus Senior High School DepartmentTrisha TorresNo ratings yet

- Statement of Cash Flow - Simple ExampleDocument5 pagesStatement of Cash Flow - Simple ExampleVinnie VermaNo ratings yet

- Finacial Statement Analysis Ratio AnalysisDocument29 pagesFinacial Statement Analysis Ratio Analysisfaridayeasmin8915No ratings yet

- Types of Financial StatementsDocument18 pagesTypes of Financial Statementsxyz mah100% (1)

- Chapter 8Document6 pagesChapter 8Nor AzuraNo ratings yet

- Accounting For ManagersDocument98 pagesAccounting For Managersutkarshmannu.ismsNo ratings yet

- Accounting EquationDocument36 pagesAccounting EquationZainon Idris100% (1)

- Profit and Loss AccountDocument5 pagesProfit and Loss AccountLanston PintoNo ratings yet

- Cash Flow StatementDocument4 pagesCash Flow Statementmajaykumar1349810No ratings yet

- FMDocument3 pagesFMSwati MaheshwariNo ratings yet

- Chapter 1 - Introduction To Financial AnalysisDocument42 pagesChapter 1 - Introduction To Financial AnalysisMinh Anh NgNo ratings yet

- Accounting 1-4Document37 pagesAccounting 1-4Abed M. SallamNo ratings yet

- Accounting Notes (Week 1)Document9 pagesAccounting Notes (Week 1)junkmail4akhNo ratings yet

- Chapter 2 FarDocument2 pagesChapter 2 FarAdil KaranNo ratings yet

- Financial AccountingDocument13 pagesFinancial AccountingBogdan MorosanNo ratings yet

- Chapter 13 - CashFlow - STUDENTSDocument5 pagesChapter 13 - CashFlow - STUDENTSCalvin Fishy SuNo ratings yet

- Fsav MidDocument12 pagesFsav Midtahsinahmed9462No ratings yet

- Statements of Cash FlowsDocument23 pagesStatements of Cash FlowslesterNo ratings yet

- Module 3 Analysis of Financial StatementsDocument24 pagesModule 3 Analysis of Financial StatementsErick Mequiso100% (1)

- Lesson 1 PDFDocument15 pagesLesson 1 PDFJet SagunNo ratings yet

- Chapter 13 PowerPointDocument89 pagesChapter 13 PowerPointcheuleee100% (1)

- Cash Flow StatementDocument4 pagesCash Flow StatementJENILINE MIZALNo ratings yet

- Week 10 (Learning Materials)Document8 pagesWeek 10 (Learning Materials)CHOI HunterNo ratings yet

- Weekly Discussion 1Document3 pagesWeekly Discussion 1Vivek SharmaNo ratings yet

- Chapter 9 - Financial AnalysisDocument13 pagesChapter 9 - Financial AnalysisNicole Feliz InfanteNo ratings yet

- Financial Acct Midterm Study GuideDocument11 pagesFinancial Acct Midterm Study GuideRobin TNo ratings yet

- Financial Statements for Service BusinessDocument9 pagesFinancial Statements for Service BusinessKarysse Arielle Noel JalaoNo ratings yet

- ACCTG 1 (Assignment 1)Document2 pagesACCTG 1 (Assignment 1)Janine KateNo ratings yet

- LECTURE 1: Accounting ReportsDocument8 pagesLECTURE 1: Accounting ReportscheskaNo ratings yet

- Gross Estate OverviewDocument27 pagesGross Estate OverviewSophia De GuzmanNo ratings yet

- CH 12 Transfer Taxes IntroDocument15 pagesCH 12 Transfer Taxes IntroSophia De GuzmanNo ratings yet

- Relevant Costing Additional ProblemsDocument6 pagesRelevant Costing Additional ProblemsSophia De GuzmanNo ratings yet

- Ae117 Relevant CostingDocument12 pagesAe117 Relevant CostingSophia De GuzmanNo ratings yet

- CH13B Gross Estate of Married DecedentsDocument11 pagesCH13B Gross Estate of Married DecedentsSophia De GuzmanNo ratings yet

- Ch13 Concept of Succession and Estate TaxDocument9 pagesCh13 Concept of Succession and Estate TaxSophia De GuzmanNo ratings yet

- CH 3 Intro To Bus. TaxDocument15 pagesCH 3 Intro To Bus. TaxSophia De GuzmanNo ratings yet

- 6.2 HyperDocument3 pages6.2 HyperSophia De GuzmanNo ratings yet

- MULTIPLE CHOICE BUDGET ASSESSMENTDocument12 pagesMULTIPLE CHOICE BUDGET ASSESSMENTSophia De GuzmanNo ratings yet

- T04 - Long-Term Construction-Type ContractsDocument11 pagesT04 - Long-Term Construction-Type ContractsJudithNo ratings yet

- The Chief Audit Executive-Understanding The Role and Professional Obligations of A CAEDocument18 pagesThe Chief Audit Executive-Understanding The Role and Professional Obligations of A CAESophia De GuzmanNo ratings yet

- Regional Mid Year Convention ProceedingsDocument18 pagesRegional Mid Year Convention ProceedingsSophia De GuzmanNo ratings yet

- Acct 2302 Chapter 13 Sample QuestionsDocument4 pagesAcct 2302 Chapter 13 Sample QuestionsSophia De GuzmanNo ratings yet

- Preferential Taxation Module 3Document4 pagesPreferential Taxation Module 3Sophia De GuzmanNo ratings yet

- Module 1 Internal Revenue TaxesDocument11 pagesModule 1 Internal Revenue TaxesSophia De GuzmanNo ratings yet

- PFRS 15 Revenue Recognition Concepts and PrinciplesDocument7 pagesPFRS 15 Revenue Recognition Concepts and PrinciplesXienaNo ratings yet

- Assignment Group Accounts ConsolidationDocument1 pageAssignment Group Accounts ConsolidationSophia De GuzmanNo ratings yet

- Data Management and Statistical ToolsDocument23 pagesData Management and Statistical ToolsSophia De GuzmanNo ratings yet

- 6.2 HyperDocument3 pages6.2 HyperSophia De GuzmanNo ratings yet

- Ifrs 9 - Financial Instruments Ias 38 and Ifrs 7Document43 pagesIfrs 9 - Financial Instruments Ias 38 and Ifrs 7JaaNo ratings yet

- The Chief Audit Executive-Understanding The Role and Professional Obligations of A CAEDocument18 pagesThe Chief Audit Executive-Understanding The Role and Professional Obligations of A CAESophia De GuzmanNo ratings yet

- CH 15 PDFDocument7 pagesCH 15 PDFYohanaNo ratings yet

- Chapter 06Document115 pagesChapter 06Shaikh FarazNo ratings yet

- Chapter 5 - ACTIVITIESDocument9 pagesChapter 5 - ACTIVITIESSophia De GuzmanNo ratings yet

- Mba ProjectDocument40 pagesMba ProjectAlvin TiggaNo ratings yet

- GSMI Report Maps Global Blockchain StandardsDocument37 pagesGSMI Report Maps Global Blockchain StandardsSORY TOURENo ratings yet

- AIG Offer To Buy Maiden Lane II SecuritiesDocument43 pagesAIG Offer To Buy Maiden Lane II Securities83jjmackNo ratings yet

- Acc112 Course Outline - NAJEEBA ALZAIMOORDocument6 pagesAcc112 Course Outline - NAJEEBA ALZAIMOORalaamabood6No ratings yet

- Bank Lacked Proof of Standing in Foreclosure CaseDocument5 pagesBank Lacked Proof of Standing in Foreclosure CaseD. BushNo ratings yet

- WAREHOUSE TO WAREHOUSE CLAUSESDocument5 pagesWAREHOUSE TO WAREHOUSE CLAUSEStinhcoonlineNo ratings yet

- University of Hartford P. O. Box 416362 Boston, MA 02241-6362Document2 pagesUniversity of Hartford P. O. Box 416362 Boston, MA 02241-6362Igor FerreiraNo ratings yet

- Journal Entries For Engineering StudentsDocument9 pagesJournal Entries For Engineering StudentsSreenivas KodamasimhamNo ratings yet

- Lic'S New Jeevan Anand PlanDocument9 pagesLic'S New Jeevan Anand Plannaik4u2002No ratings yet

- Record to Report: The End-to-End Financial Process CycleDocument4 pagesRecord to Report: The End-to-End Financial Process CycleDANIELNo ratings yet

- Crystal Reports - Dunning Letter 01 - CR (GB)Document5 pagesCrystal Reports - Dunning Letter 01 - CR (GB)HILLARY KIRUINo ratings yet

- Analysis of Banking Requirements of Various Business UnitsDocument49 pagesAnalysis of Banking Requirements of Various Business Unitsagr_belaNo ratings yet

- What Is FCCB?: Foreign Currency Convertible Bond Is A Type of ConvertibleDocument8 pagesWhat Is FCCB?: Foreign Currency Convertible Bond Is A Type of ConvertiblesbghargeNo ratings yet

- Big Three Credit Rating AgenciesDocument21 pagesBig Three Credit Rating AgenciesDibesh PadiaNo ratings yet

- DHEA NOVI SummaryDocument1 pageDHEA NOVI SummaryWasis WicaksonoNo ratings yet

- Newzen Mba Finance 2023Document11 pagesNewzen Mba Finance 2023New Zen InfotechNo ratings yet

- Test Bank For Auditing A Practical Approach With Data Analytics 1st Edition Raymond N Johnson Laura Davis Wiley Robyn Moroney Fiona Campbell Jane HamiltonDocument11 pagesTest Bank For Auditing A Practical Approach With Data Analytics 1st Edition Raymond N Johnson Laura Davis Wiley Robyn Moroney Fiona Campbell Jane Hamiltonironerpaijama.pe2ddu100% (44)

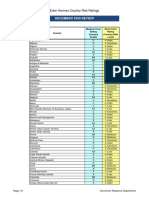

- December 2020 Review: Euler Hermes Country Risk RatingsDocument5 pagesDecember 2020 Review: Euler Hermes Country Risk RatingsLFNo ratings yet

- CGC - 2.2.1 Study - 8FDLaelerDocument7 pagesCGC - 2.2.1 Study - 8FDLaelerCaleb Gonzalez CruzNo ratings yet

- Account Statement 01 Feb 2023-30 Apr 2023Document4 pagesAccount Statement 01 Feb 2023-30 Apr 2023PRONAB MAJHINo ratings yet

- Guide To FCNR Loan - Advantages & DisadvantagesDocument5 pagesGuide To FCNR Loan - Advantages & Disadvantagesavinash singhNo ratings yet

- Optimal Cash Levels with Baumol and Miller-Orr ModelsDocument19 pagesOptimal Cash Levels with Baumol and Miller-Orr ModelsHimanshu DuttaNo ratings yet

- Analyzing Consolidated Financial StatementsDocument3 pagesAnalyzing Consolidated Financial StatementsBryle Jay LapeNo ratings yet

- Chapter 9 Practice Questions PDFDocument6 pagesChapter 9 Practice Questions PDFleili fallahNo ratings yet

- Topic 1 (Simple Interest)Document28 pagesTopic 1 (Simple Interest)Nanteni Ganesan100% (1)

- North South University Summer Class AssignmentDocument15 pagesNorth South University Summer Class AssignmentMd.sabir 1831620030No ratings yet

- Sole Trader'S Final AccountsDocument12 pagesSole Trader'S Final AccountsSheikh Mass Jah0% (1)

- Theory On Dissolution of Partnership FirmDocument7 pagesTheory On Dissolution of Partnership FirmTanisha PoddarNo ratings yet

- Gautam NayakDocument10 pagesGautam Nayakdivya chawlaNo ratings yet

- Book-Keeping & AccountancyDocument70 pagesBook-Keeping & AccountancyIstiaqueNo ratings yet

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (12)

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantFrom EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantRating: 4.5 out of 5 stars4.5/5 (146)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyFrom EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyRating: 5 out of 5 stars5/5 (1)

- Financial Accounting For Dummies: 2nd EditionFrom EverandFinancial Accounting For Dummies: 2nd EditionRating: 5 out of 5 stars5/5 (10)

- Profit First for Therapists: A Simple Framework for Financial FreedomFrom EverandProfit First for Therapists: A Simple Framework for Financial FreedomNo ratings yet

- Bookkeeping: A Beginner’s Guide to Accounting and Bookkeeping for Small BusinessesFrom EverandBookkeeping: A Beginner’s Guide to Accounting and Bookkeeping for Small BusinessesRating: 5 out of 5 stars5/5 (4)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsFrom EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsRating: 4 out of 5 stars4/5 (7)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- The Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyFrom EverandThe Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyRating: 4 out of 5 stars4/5 (4)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetFrom EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetNo ratings yet

- Full Charge Bookkeeping, For the Beginner, Intermediate & Advanced BookkeeperFrom EverandFull Charge Bookkeeping, For the Beginner, Intermediate & Advanced BookkeeperRating: 5 out of 5 stars5/5 (3)

- NLP:The Essential Handbook for Business: The Essential Handbook for Business: Communication Techniques to Build Relationships, Influence Others, and Achieve Your GoalsFrom EverandNLP:The Essential Handbook for Business: The Essential Handbook for Business: Communication Techniques to Build Relationships, Influence Others, and Achieve Your GoalsRating: 4.5 out of 5 stars4.5/5 (4)

- Ledger Legends: A Bookkeeper's Handbook for Financial Success: Navigating the World of Business Finances with ConfidenceFrom EverandLedger Legends: A Bookkeeper's Handbook for Financial Success: Navigating the World of Business Finances with ConfidenceNo ratings yet

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- Accounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)From EverandAccounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)Rating: 4.5 out of 5 stars4.5/5 (5)