You might also like

- Budget 2023-24 and Eco Survey 2022-23 Vivek SinghDocument14 pagesBudget 2023-24 and Eco Survey 2022-23 Vivek SinghSazia AnsariNo ratings yet

- Highlights of The Union Budget 2022-23Document11 pagesHighlights of The Union Budget 2022-23bsaikrishnaNo ratings yet

- Union Budget 2022-23Document3 pagesUnion Budget 2022-23Siddartha ShettyNo ratings yet

- Budget 2022-2023: Sagar Yadav Bhumi Patel Satyam Srivastava Anu Prajapati Vrutiksha Shah Viraj MhatreDocument10 pagesBudget 2022-2023: Sagar Yadav Bhumi Patel Satyam Srivastava Anu Prajapati Vrutiksha Shah Viraj MhatreSagar YadavNo ratings yet

- Key Budget Highlights EconomyDocument5 pagesKey Budget Highlights EconomyVaibhav NarangNo ratings yet

- Union Budget of India 2022 - 23Document14 pagesUnion Budget of India 2022 - 23Murali Krishna ReddyNo ratings yet

- Budget 2022 IIM LucknowDocument39 pagesBudget 2022 IIM LucknowGopanNo ratings yet

- The Union Budget 2022-2023Document19 pagesThe Union Budget 2022-2023Rohit GoyalNo ratings yet

- 2digital University: in Her Budget Speech, Sitharaman Emphasised On Strengthening DigitalDocument4 pages2digital University: in Her Budget Speech, Sitharaman Emphasised On Strengthening DigitalshikharNo ratings yet

- Key Highlights: Union BudgetDocument35 pagesKey Highlights: Union BudgetSherlin NatashaNo ratings yet

- Updated - Union Budget 2022-23 Detailed PDF RBI GR B NABARD GR A 2022 1 Lyst5809 PDFDocument35 pagesUpdated - Union Budget 2022-23 Detailed PDF RBI GR B NABARD GR A 2022 1 Lyst5809 PDFARCHANA PRAKASHNo ratings yet

- ARYAFiscalbudgetDocument10 pagesARYAFiscalbudgetArya RokadeNo ratings yet

- Highlights of Union Budget 2022 Eng 21Document9 pagesHighlights of Union Budget 2022 Eng 21Anna P ANo ratings yet

- Union Budget 22Document7 pagesUnion Budget 22pawani GuptaNo ratings yet

- Commercial Banking Assignment Budget 2022 Highlights - 1) EconomyDocument9 pagesCommercial Banking Assignment Budget 2022 Highlights - 1) EconomyShruti UpadhyayNo ratings yet

- Highlights of The Union Budget 2022 - 2023Document12 pagesHighlights of The Union Budget 2022 - 2023Robin WadhwaNo ratings yet

- Union BudgetDocument14 pagesUnion BudgetAnuj ThapaNo ratings yet

- Highlights of Union Budget 2022 1643772013Document22 pagesHighlights of Union Budget 2022 1643772013Khushboo MehtaNo ratings yet

- Budget 2023Document25 pagesBudget 2023Ankita MishraNo ratings yet

- BUDGET 2022 HighlightsDocument5 pagesBUDGET 2022 HighlightsVivek KuchhalNo ratings yet

- Budget, 2022Document12 pagesBudget, 2022satwik jainNo ratings yet

- Union Budget 2022: 92nd Union Budget 2022-23: Key Highlights of Union BudgetDocument4 pagesUnion Budget 2022: 92nd Union Budget 2022-23: Key Highlights of Union BudgetsiddNo ratings yet

- Fin An Ce Mi No R PR OjDocument13 pagesFin An Ce Mi No R PR OjVignesh SuryadevaraNo ratings yet

- Union Budget 2022Document23 pagesUnion Budget 2022varun lobheNo ratings yet

- Weekly One Liners 31st January To 6th of February 2022Document14 pagesWeekly One Liners 31st January To 6th of February 2022Rajesh ShenoyNo ratings yet

- Union Budget 2022-23Document17 pagesUnion Budget 2022-23gowthamiNo ratings yet

- The Budget Goals For FY2022Document2 pagesThe Budget Goals For FY2022anuragsinghmaurya1234No ratings yet

- Union Budget 2022-23 Lyst4248Document34 pagesUnion Budget 2022-23 Lyst4248Kothamasu RajeshNo ratings yet

- Union Budget 2022enabling India's Big Leap: February 01 2022Document21 pagesUnion Budget 2022enabling India's Big Leap: February 01 2022sruthikaNo ratings yet

- Union Budget 2022enabling India's Big Leap: February 01 2022Document18 pagesUnion Budget 2022enabling India's Big Leap: February 01 2022sruthikaNo ratings yet

- Budget 2022-23Document13 pagesBudget 2022-23fasf asfgrgNo ratings yet

- PM Gati Shakti Transforming India's InfrastrutureDocument21 pagesPM Gati Shakti Transforming India's InfrastrutureAtri JoshiNo ratings yet

- Budget Analysis 2022-23Document9 pagesBudget Analysis 2022-23Dhroov GoyalNo ratings yet

- Summary of Union Budget 2021-22: Health and WellbeingDocument10 pagesSummary of Union Budget 2021-22: Health and WellbeingAtul sharmaNo ratings yet

- Ga MCQ-NSRDocument15 pagesGa MCQ-NSRCREDIT BHARATPURNo ratings yet

- Ga MCQ-NSR-1-7Document7 pagesGa MCQ-NSR-1-7CREDIT BHARATPURNo ratings yet

- Construction - Make in IndiaDocument7 pagesConstruction - Make in IndiaAgila MarichettyNo ratings yet

- Union Budget 22-23.pngDocument5 pagesUnion Budget 22-23.pngRajat saxenaNo ratings yet

- Union Budget 2023 1675312125 PDFDocument12 pagesUnion Budget 2023 1675312125 PDFHafisMohammedSahibNo ratings yet

- Budget 2022-23 Summary - Final For WebsiteDocument20 pagesBudget 2022-23 Summary - Final For WebsiteSubhankar BasakNo ratings yet

- Gati Shakti Master PlanDocument15 pagesGati Shakti Master PlanAgni BanerjeeNo ratings yet

- 392 GKMagazine February 2022 PdffileDocument24 pages392 GKMagazine February 2022 PdffileMudit SinghNo ratings yet

- Budget Highlights 2022-23Document43 pagesBudget Highlights 2022-23Shubhendu VermaNo ratings yet

- NotesDocument2 pagesNotesROTARACT CLUBNo ratings yet

- Union Budget 2022-23Document12 pagesUnion Budget 2022-23Rupam DebsharmaNo ratings yet

- Highlights of The Union Budget 2023-24Document5 pagesHighlights of The Union Budget 2023-24Aspirant AspirantNo ratings yet

- Infrastructure Sector in India: Government Initiative and InvestmentDocument13 pagesInfrastructure Sector in India: Government Initiative and InvestmentShubham AggarwalNo ratings yet

- BUDGET-2021-2022 9563604 PowerpointDocument10 pagesBUDGET-2021-2022 9563604 PowerpointAKAS2451253No ratings yet

- Trinidad and Tobago 2022 Budget HighlightsDocument6 pagesTrinidad and Tobago 2022 Budget Highlightsbrandon davidNo ratings yet

- Mid Term AssignmentDocument11 pagesMid Term AssignmentHarsh JainNo ratings yet

- The State of Indian Economy: Projected GrowthDocument5 pagesThe State of Indian Economy: Projected GrowthMega No01No ratings yet

- Budjet 202222'Document8 pagesBudjet 202222'Shruti JainNo ratings yet

- Union Budget 23Document6 pagesUnion Budget 23SAURAV AJAINo ratings yet

- Budget 2023 SummaryDocument2 pagesBudget 2023 SummarySidhartha Marketing CompanyNo ratings yet

- Yk Gist: - MARCH 2022Document21 pagesYk Gist: - MARCH 2022Yathartha Singh ChauhanNo ratings yet

- Budget 2024Document21 pagesBudget 2024kolkatacareerlauncherNo ratings yet

- KEY Features OF Budget 2019-20Document16 pagesKEY Features OF Budget 2019-20PankajNo ratings yet

- Budget 2022 StudynitiDocument20 pagesBudget 2022 StudynitiAnkita JindalNo ratings yet

- Highlights of The Union Budget 2022 Partt 222Document33 pagesHighlights of The Union Budget 2022 Partt 222KUSUMA ANo ratings yet

- Strengthening Fiscal Decentralization in Nepal’s Transition to FederalismFrom EverandStrengthening Fiscal Decentralization in Nepal’s Transition to FederalismNo ratings yet

- AIR 61 CoachingDocument10 pagesAIR 61 CoachingChinmay JenaNo ratings yet

- Security Mains PYQ 2013-22Document5 pagesSecurity Mains PYQ 2013-22Chinmay JenaNo ratings yet

- GandhianMovementPYQ SSDocument3 pagesGandhianMovementPYQ SSChinmay JenaNo ratings yet

- Daf Based QuestionsDocument11 pagesDaf Based QuestionsChinmay JenaNo ratings yet

- Byju Ias BooklistDocument2 pagesByju Ias BooklistChinmay JenaNo ratings yet

- Motion of ThanksDocument1 pageMotion of ThanksChinmay JenaNo ratings yet

- BOOKLISTDocument3 pagesBOOKLISTChinmay JenaNo ratings yet

- Strategy For EssayDocument5 pagesStrategy For EssayChinmay JenaNo ratings yet

- GovernorPYQ SSDocument3 pagesGovernorPYQ SSChinmay JenaNo ratings yet

- Essay PYQsDocument10 pagesEssay PYQsChinmay JenaNo ratings yet

- Governors-General and Viceroys of IndiaDocument9 pagesGovernors-General and Viceroys of IndiaChinmay JenaNo ratings yet

- Block 1Document54 pagesBlock 1Chinmay JenaNo ratings yet

- Foreign TravellersDocument9 pagesForeign TravellersSamaresh HalderNo ratings yet

- INC Annual SessionsDocument5 pagesINC Annual SessionsChinmay JenaNo ratings yet

- SOCIOLOGY STRATEGY - Rank 63, Tanai Sultania, CSE - 2016 - INSIGHTSIASDocument11 pagesSOCIOLOGY STRATEGY - Rank 63, Tanai Sultania, CSE - 2016 - INSIGHTSIASChinmay JenaNo ratings yet

- SOCIOLOGY STRATEGY Garima Lekhwani Rank 136 CSE-2016 Sociology Marks 290Document3 pagesSOCIOLOGY STRATEGY Garima Lekhwani Rank 136 CSE-2016 Sociology Marks 290Chinmay JenaNo ratings yet

- Freedom Struggle at A GlanceDocument3 pagesFreedom Struggle at A GlanceChinmay Jena100% (1)

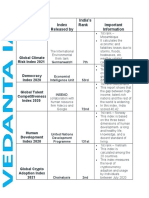

- Rank of India in Different Indexes 2020 21 62c8be12 d136 436a 8d0eDocument5 pagesRank of India in Different Indexes 2020 21 62c8be12 d136 436a 8d0eChinmay JenaNo ratings yet

- Prelims StrategyDocument2 pagesPrelims StrategyChinmay JenaNo ratings yet

- 100 Day Sociology Plan (By reliableANDvalid)Document25 pages100 Day Sociology Plan (By reliableANDvalid)Chinmay JenaNo ratings yet

- SOCIOLOGY STRATEGY Hemant Bhorkhade Rank 424 CSE-2017 Sociology Marks 324Document4 pagesSOCIOLOGY STRATEGY Hemant Bhorkhade Rank 424 CSE-2017 Sociology Marks 324Chinmay JenaNo ratings yet

- Journals & NewspapersDocument2 pagesJournals & NewspapersChinmay JenaNo ratings yet

- Important Chapters From BA & MA SociologyDocument19 pagesImportant Chapters From BA & MA SociologyKevin KevinNo ratings yet

- Soc GS2 ThinkersDocument11 pagesSoc GS2 ThinkersChinmay JenaNo ratings yet

- Art & Culture AptiplusDocument21 pagesArt & Culture AptiplusChinmay JenaNo ratings yet

- History TimelineDocument8 pagesHistory TimelineChinmay JenaNo ratings yet

- Vedanta Ias General ScienceDocument24 pagesVedanta Ias General ScienceChinmay JenaNo ratings yet

- ChemistryDocument22 pagesChemistryChinmay JenaNo ratings yet

- Common Mistakes Done by UPSC Aspirants and How To Avoid Those MistakesDocument5 pagesCommon Mistakes Done by UPSC Aspirants and How To Avoid Those MistakesChinmay JenaNo ratings yet

- SNT PYQs - SHREYA SHREEDocument13 pagesSNT PYQs - SHREYA SHREEChinmay JenaNo ratings yet

- 20240119-AC MV Cable Schedule - R1Document1 page20240119-AC MV Cable Schedule - R1newattelectricNo ratings yet

- The Empire in FlamesDocument73 pagesThe Empire in FlamesSergio Esperalta Gata100% (2)

- 1 IntroductionDocument25 pages1 IntroductionNida I. FarihahNo ratings yet

- Service ManualDocument9 pagesService ManualgibonulNo ratings yet

- Economic ResponsibilityDocument1 pageEconomic ResponsibilityLovely Shyra SalcesNo ratings yet

- Well Control Daily Checklist Procedure VDocument13 pagesWell Control Daily Checklist Procedure VmuratNo ratings yet

- Boiler I.B.R. CalculationDocument10 pagesBoiler I.B.R. CalculationGurinder Jit Singh100% (1)

- Pharmaceutics Exam 3 - This SemesterDocument6 pagesPharmaceutics Exam 3 - This Semesterapi-3723612100% (1)

- Advantages of Solid-State Relays Over Electro-Mechanical RelaysDocument11 pagesAdvantages of Solid-State Relays Over Electro-Mechanical RelaysKen Dela CernaNo ratings yet

- Msds NitobenzeneDocument5 pagesMsds NitobenzeneAnngie Nove SimbolonNo ratings yet

- Sample Theory With Ques. - Organometallic Compounds (NET CH UNIT-3) PDFDocument26 pagesSample Theory With Ques. - Organometallic Compounds (NET CH UNIT-3) PDFPriyanshi VermaNo ratings yet

- Clippers and ClampersDocument8 pagesClippers and Clamperspuneeth kumarNo ratings yet

- LANCNC Display Mount Plate Installation v5Document10 pagesLANCNC Display Mount Plate Installation v5Maquina EspecialNo ratings yet

- Laporan Hasil Praktik Bahasa Inggris Dengan Tamu Asing Di Pantai KutaDocument12 pagesLaporan Hasil Praktik Bahasa Inggris Dengan Tamu Asing Di Pantai KutaEnal MegantaraNo ratings yet

- DISCOMs PresentationDocument17 pagesDISCOMs PresentationR&I HVPN0% (1)

- Spare Parts Quotation For Scba & Eebd - 2021.03.19Document14 pagesSpare Parts Quotation For Scba & Eebd - 2021.03.19byhf2jgqprNo ratings yet

- Inheritance: Compiled By: Brandon Freel Stolen and Edited From: IMS and Dr. Kyle Stutts (SHSU)Document25 pagesInheritance: Compiled By: Brandon Freel Stolen and Edited From: IMS and Dr. Kyle Stutts (SHSU)Mary Ann DimacaliNo ratings yet

- Differential Release of Mast Cell Mediators and The Pathogenesis of InflammationDocument14 pagesDifferential Release of Mast Cell Mediators and The Pathogenesis of InflammationklaumrdNo ratings yet

- Hydraulic and Irrigation EnggDocument9 pagesHydraulic and Irrigation EnggUmar Farooq 175-17 CNo ratings yet

- Transportation Law SyllabusDocument17 pagesTransportation Law SyllabusIchimaru TokugawaNo ratings yet

- Nuclear Energy Today PDFDocument112 pagesNuclear Energy Today PDFDaniel Bogdan DincaNo ratings yet

- Nsejs Exam Solutions Paper 2019 PDFDocument27 pagesNsejs Exam Solutions Paper 2019 PDFMrinalini SinghNo ratings yet

- Fluidization - Expansion Equations For Fluidized Solid Liquid Systems (Akgiray and Soyer, 2006)Document10 pagesFluidization - Expansion Equations For Fluidized Solid Liquid Systems (Akgiray and Soyer, 2006)Moisés MachadoNo ratings yet

- Ant WorldDocument17 pagesAnt WorldGerardo TorresNo ratings yet

- T 703Document4 pagesT 703Marcelo RojasNo ratings yet

- Chapter 1 Tutorial IlluminationDocument9 pagesChapter 1 Tutorial IlluminationFemi PrinceNo ratings yet

- International Journal of Technical Innovation in Modern Engineering & Science (IJTIMES)Document13 pagesInternational Journal of Technical Innovation in Modern Engineering & Science (IJTIMES)pavan kumar tNo ratings yet

- SC3 User Manual - V1.06 PDFDocument196 pagesSC3 User Manual - V1.06 PDFJoeNo ratings yet

- OCDM2223 Tutorial7solvedDocument5 pagesOCDM2223 Tutorial7solvedqq727783No ratings yet

- Technical Specifications For LT/HT, XLPE Insulated Aluminium/Copper CablesDocument49 pagesTechnical Specifications For LT/HT, XLPE Insulated Aluminium/Copper CablesAjay KumarNo ratings yet