You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- GO2bank Bank StatementDocument6 pagesGO2bank Bank Statementrebecca greenfieldNo ratings yet

- A Study On Investment Analysis and Portfolio ManagementDocument94 pagesA Study On Investment Analysis and Portfolio ManagementKeerthi100% (2)

- A Project Report On Credit CardDocument26 pagesA Project Report On Credit CardKGF SARTH ARMYNo ratings yet

- Statement of Account: NO 215 BATU 2 3/4 Jalan Bakri 84000 MUAR, JOHORDocument9 pagesStatement of Account: NO 215 BATU 2 3/4 Jalan Bakri 84000 MUAR, JOHORMuhammad ShahidanNo ratings yet

- Unit 14: Banking: Section 1: Reading Pre-Reading Tasks Discussion - Pair WorkDocument9 pagesUnit 14: Banking: Section 1: Reading Pre-Reading Tasks Discussion - Pair WorkThanh TúNo ratings yet

- 3.table of Contents (Index)Document1 page3.table of Contents (Index)KGF SARTH ARMYNo ratings yet

- A Project Report OyDocument28 pagesA Project Report OyKGF SARTH ARMYNo ratings yet

- 1047pm - 55.epra Journals 7968Document5 pages1047pm - 55.epra Journals 7968KGF SARTH ARMYNo ratings yet

- CFPB Consumer Credit Card Market Report 2021Document178 pagesCFPB Consumer Credit Card Market Report 2021KGF SARTH ARMYNo ratings yet

- 4080CDJL956903 Statement of AccountDocument3 pages4080CDJL956903 Statement of AccountJanakiram TammineniNo ratings yet

- Fundamental Accounting Principles Canadian Vol 1 Canadian 14th Edition Larson Test BankDocument39 pagesFundamental Accounting Principles Canadian Vol 1 Canadian 14th Edition Larson Test Bankoxheartpanch07mce100% (22)

- Phung Van Cung: Spend Account StatementDocument2 pagesPhung Van Cung: Spend Account StatementhienvvuNo ratings yet

- UCO Bank - Green Pin Generation Using UCO Mobile BDocument1 pageUCO Bank - Green Pin Generation Using UCO Mobile Bsunny kumarNo ratings yet

- Mobile Payment Indonesia 2018 - MDI Ventures and Mandiri SekuritasDocument47 pagesMobile Payment Indonesia 2018 - MDI Ventures and Mandiri SekuritasAdenia HarahapNo ratings yet

- Case #2Document2 pagesCase #2anneNo ratings yet

- Imfpa TempleteDocument4 pagesImfpa TempleteQip RainzhaNo ratings yet

- Cirrus (Interbank Network) - WikipediaDocument2 pagesCirrus (Interbank Network) - WikipediaSamNo ratings yet

- MGT101 Finalterm Solved Paper#13Document200 pagesMGT101 Finalterm Solved Paper#13Qasim TasawarNo ratings yet

- AdmitereDocument10 pagesAdmitereNicole AdinaNo ratings yet

- Domestic Bank ListDocument18 pagesDomestic Bank Listqqnvt78No ratings yet

- WWW Aubank In/annual-ReportDocument324 pagesWWW Aubank In/annual-ReportKALEEN BHAIYA KING OF MIRZAPURNo ratings yet

- Group 1 Chapter 1 3 Quali Research - Docx REVISEDDocument40 pagesGroup 1 Chapter 1 3 Quali Research - Docx REVISEDLeo EspinoNo ratings yet

- E Shram Card - Online Apply, Check Payment Status, @register - Eshram.gov - inDocument9 pagesE Shram Card - Online Apply, Check Payment Status, @register - Eshram.gov - inAkash guptaNo ratings yet

- Exercises in Acctg 114-Applied Auditing: College of Business Management & AccountancyDocument4 pagesExercises in Acctg 114-Applied Auditing: College of Business Management & Accountancybjay chuyNo ratings yet

- 4.1 Bank Lending Decision ProblemDocument23 pages4.1 Bank Lending Decision ProblemAbhishek mahalungeNo ratings yet

- Interim Project Report of Internship Undertaken atDocument14 pagesInterim Project Report of Internship Undertaken atAnimesh SalhotraNo ratings yet

- Fundamentals of Accounting MODULE 3Document31 pagesFundamentals of Accounting MODULE 3amnesia girlNo ratings yet

- Internship Rahul SBLDocument75 pagesInternship Rahul SBLMùkésh RôyNo ratings yet

- Unit Two General and Subsidiary Ledgers: AU Ethiopian Government Accounting 2019Document10 pagesUnit Two General and Subsidiary Ledgers: AU Ethiopian Government Accounting 2019TIZITAW MASRESHANo ratings yet

- Call Deposit Receipt Meezan BankDocument22 pagesCall Deposit Receipt Meezan BankNabeel KhanNo ratings yet

- Introduction To Financial Systems and Financial MarketsDocument22 pagesIntroduction To Financial Systems and Financial MarketsDiana Rose L. BautistaNo ratings yet

- Fintech in Latin America and The Caribbean A Consolidated EcosystemDocument203 pagesFintech in Latin America and The Caribbean A Consolidated EcosystemMilos MilovanovicNo ratings yet

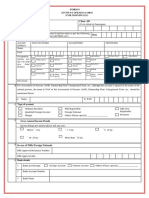

- 05 Circular - ForM 9 - Account Opening Form (Individual)Document4 pages05 Circular - ForM 9 - Account Opening Form (Individual)Sneha bagweNo ratings yet

- Engineering Economics Upm Samples 10Document4 pagesEngineering Economics Upm Samples 10Cesia MontelloNo ratings yet

- Creditreport 2555930042Document60 pagesCreditreport 2555930042nischal.khatri07No ratings yet