You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (843)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5810)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (346)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Chapter 31 - Lower of Cost and Net Realizable Value: Purchase CommitmentDocument21 pagesChapter 31 - Lower of Cost and Net Realizable Value: Purchase CommitmentKimberly Claire Atienza100% (5)

- Corpo LawDocument20 pagesCorpo LawKaren Ronquillo0% (1)

- Afar 01 P'ship Formation QuizDocument3 pagesAfar 01 P'ship Formation QuizJohn Laurence Loplop0% (1)

- Cost of CapitalDocument39 pagesCost of CapitalAnonymous ibmeej9No ratings yet

- Summary of Business - Strategy - Application - Level - Question - Bank - With Immediate AnswersDocument221 pagesSummary of Business - Strategy - Application - Level - Question - Bank - With Immediate AnswersIQBAL MAHMUDNo ratings yet

- Banking Law Reviewer Hot JuristDocument27 pagesBanking Law Reviewer Hot Juristgrego centillas100% (1)

- Risk and Return: 1. Chapter 11 (Textbook) : 7, 13, 14, 24Document3 pagesRisk and Return: 1. Chapter 11 (Textbook) : 7, 13, 14, 24anon_355962815100% (1)

- It Governance TechnologyDocument5 pagesIt Governance TechnologyIQBAL MAHMUDNo ratings yet

- It Governance Technology-Chapter 01Document4 pagesIt Governance Technology-Chapter 01IQBAL MAHMUDNo ratings yet

- Summary of Business Strategy Application Level - Self Test With Immediate AnswerDocument177 pagesSummary of Business Strategy Application Level - Self Test With Immediate AnswerIQBAL MAHMUDNo ratings yet

- Summary of Audit & Assurance Application Level - Self Test With Immediate AnswerDocument72 pagesSummary of Audit & Assurance Application Level - Self Test With Immediate AnswerIQBAL MAHMUDNo ratings yet

- Summary of Business Strategy Application Level Interactive Questions With Immediate AnswerDocument118 pagesSummary of Business Strategy Application Level Interactive Questions With Immediate AnswerIQBAL MAHMUDNo ratings yet

- Summary of Audit & Assurance Application Level - Interactive Questions With Immediate AnswersDocument46 pagesSummary of Audit & Assurance Application Level - Interactive Questions With Immediate AnswersIQBAL MAHMUDNo ratings yet

- Summary of Audit & Assurance Application Level - Worked ExampleDocument22 pagesSummary of Audit & Assurance Application Level - Worked ExampleIQBAL MAHMUDNo ratings yet

- Summary of Audit & Assurance - Application - Level - Question - Bank - With Immediate AnswersDocument161 pagesSummary of Audit & Assurance - Application - Level - Question - Bank - With Immediate AnswersIQBAL MAHMUDNo ratings yet

- Ca Ipcc - ItDocument82 pagesCa Ipcc - ItIQBAL MAHMUDNo ratings yet

- Question - Analysis Audit and Assurance Application LevelDocument28 pagesQuestion - Analysis Audit and Assurance Application LevelIQBAL MAHMUDNo ratings yet

- Professional and Advanced Level Oct 2019Document20 pagesProfessional and Advanced Level Oct 2019IQBAL MAHMUDNo ratings yet

- Inestment Appraisal Synopsis 1 2Document8 pagesInestment Appraisal Synopsis 1 2IQBAL MAHMUDNo ratings yet

- The Potential of Blockchain Technology and DigitalDocument10 pagesThe Potential of Blockchain Technology and DigitalIQBAL MAHMUDNo ratings yet

- PL M17 Financial ManagementDocument9 pagesPL M17 Financial ManagementIQBAL MAHMUDNo ratings yet

- Investment CriteriaDocument23 pagesInvestment Criteriaiqbal irfaniNo ratings yet

- Buku Nota PertnershipDocument33 pagesBuku Nota PertnershipmaiNo ratings yet

- NISM VA Chapter Wise QuestionsDocument45 pagesNISM VA Chapter Wise QuestionsAvinash JainNo ratings yet

- Cost Notes PDF FreeDocument6 pagesCost Notes PDF FreeDark PrincessNo ratings yet

- Date Particulars DR Amount CR Amount Ledger Folio NoDocument23 pagesDate Particulars DR Amount CR Amount Ledger Folio NoHarmeet kapoorNo ratings yet

- Reaction Paper - The Big Short MovieDocument9 pagesReaction Paper - The Big Short MovieArlene Gomez100% (3)

- Unit 3 ID - CBDocument62 pagesUnit 3 ID - CBASHISH KUMARNo ratings yet

- Finacct Mock Exam 1Document7 pagesFinacct Mock Exam 1Joseph Gerald M. ArcegaNo ratings yet

- Chapter 16Document30 pagesChapter 16Yui LeeNo ratings yet

- Statement of Comprehensive IncomeDocument4 pagesStatement of Comprehensive IncomeVeronica BaileyNo ratings yet

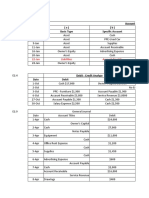

- Account Debited (A) (B) Date Basic Type Specific AccountDocument12 pagesAccount Debited (A) (B) Date Basic Type Specific AccountVALENCIA TORENTHANo ratings yet

- Dissertation 6 - ZimmailDocument2 pagesDissertation 6 - ZimmailNaison Shingirai PfavayiNo ratings yet

- PAS 34 Interim ReportingDocument5 pagesPAS 34 Interim Reportingjapvivi ceceNo ratings yet

- Nature and Formation of A PartnershipDocument26 pagesNature and Formation of A PartnershipNazarene Kate PunzalanNo ratings yet

- De Leon Solman 2014 2 CostDocument95 pagesDe Leon Solman 2014 2 CostgabrielleNo ratings yet

- BCG ApproachDocument2 pagesBCG ApproachAdhityaNo ratings yet

- Business Combi Part 2Document20 pagesBusiness Combi Part 2Rica Joy RuzgalNo ratings yet

- Perpetual Non Cumulative Preference ShareDocument11 pagesPerpetual Non Cumulative Preference ShareSiddhartha YadavNo ratings yet

- Mutual Fund 1Document3 pagesMutual Fund 1Lyra Joy CalayanNo ratings yet

- Shikhar CourierDocument13 pagesShikhar CourierKESHAV JAINNo ratings yet

- Sidrah Rakhangi - TP059572Document11 pagesSidrah Rakhangi - TP059572Sidrah RakhangeNo ratings yet

- Answers Biological AssetsDocument4 pagesAnswers Biological AssetsJanella Gail ArenasNo ratings yet

- Fundamental Analysis Rohan 110421 j4v4dfc1r520210410Document60 pagesFundamental Analysis Rohan 110421 j4v4dfc1r520210410miserable1995No ratings yet

- Taxation of Dividend: Change in Dividend Taxation Regime Under Finance Act, 2020Document4 pagesTaxation of Dividend: Change in Dividend Taxation Regime Under Finance Act, 2020Swapnil SudhanshuNo ratings yet