You might also like

- Cost Terminologies and ClassficationsDocument51 pagesCost Terminologies and ClassficationsLim Jie XiNo ratings yet

- Chapter 2 - Managerial Acc. & Cost ConceptsDocument23 pagesChapter 2 - Managerial Acc. & Cost ConceptsMuhammad Ali KazmiNo ratings yet

- Management Accounting: Product CostingDocument22 pagesManagement Accounting: Product CostingDaksh AnejaNo ratings yet

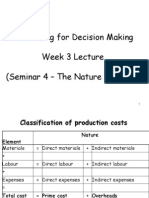

- Accounting For Decision Making Week 3 Lecture (Seminar 4 - The Nature of Costs)Document51 pagesAccounting For Decision Making Week 3 Lecture (Seminar 4 - The Nature of Costs)nwcbenny337No ratings yet

- Chapter 2-Cost ClassificationDocument66 pagesChapter 2-Cost Classification040404.anniNo ratings yet

- Chapter 7.process Costing - For Students - Part1Document13 pagesChapter 7.process Costing - For Students - Part1DAN NGUYEN THENo ratings yet

- Manufacturing CostDocument22 pagesManufacturing CostadaneNo ratings yet

- Chapter 02 - Cost Term and Concepts FinalDocument60 pagesChapter 02 - Cost Term and Concepts FinalAminaMatinNo ratings yet

- Topic 2 IDocument16 pagesTopic 2 Iami zawaniNo ratings yet

- Managerial Accounting Reviewer PDFDocument17 pagesManagerial Accounting Reviewer PDFMicah UbaldoNo ratings yet

- Chapter 2 Cost Accounting ConceptsDocument22 pagesChapter 2 Cost Accounting ConceptsRosliana RazabNo ratings yet

- Job-Order Costing Flow CaloniaDocument18 pagesJob-Order Costing Flow CaloniaLaurever CaloniaNo ratings yet

- (Revised) Week 13 - ReviewDocument94 pages(Revised) Week 13 - ReviewCheuk Ling SoNo ratings yet

- Cost Accounting Concepts: Prof. Dr. Farid MoharamDocument90 pagesCost Accounting Concepts: Prof. Dr. Farid Moharammohamed el kadyNo ratings yet

- Week 2-Basic Cost ManagementDocument21 pagesWeek 2-Basic Cost ManagementRichard Oliver CortezNo ratings yet

- Lec 04 - Managerial Accounting (Concepts & Principles)Document36 pagesLec 04 - Managerial Accounting (Concepts & Principles)Sakib RafeeNo ratings yet

- Lec 03 - Managerial Accounting (Concepts & Principles)Document36 pagesLec 03 - Managerial Accounting (Concepts & Principles)ABDUL HASIB HASAN ZAYEDNo ratings yet

- Managerial Accounting and Cost ConceptsDocument6 pagesManagerial Accounting and Cost ConceptsJUST KINGNo ratings yet

- Ilovepdf MergedDocument34 pagesIlovepdf Mergeddivyanshi singhNo ratings yet

- Introduction To Cost and Management AccountingDocument31 pagesIntroduction To Cost and Management AccountingTestNo ratings yet

- Management Accounting Session 2 Cost Terms & Purposes: Indian Institute of Management RohtakDocument58 pagesManagement Accounting Session 2 Cost Terms & Purposes: Indian Institute of Management RohtakSiddharthNo ratings yet

- Cost Terms, Concepts, and ClassificationDocument27 pagesCost Terms, Concepts, and ClassificationParadise VillageNo ratings yet

- Managerial Accounting and Cost ConceptsDocument50 pagesManagerial Accounting and Cost ConceptsGigo Kafare BinoNo ratings yet

- Managerial Accounting and Cost Concepts: Mcgraw-Hill/IrwinDocument55 pagesManagerial Accounting and Cost Concepts: Mcgraw-Hill/IrwinWaqas HussainNo ratings yet

- Acfm CH - Four 2022Document182 pagesAcfm CH - Four 2022mihiretche0No ratings yet

- Cost Analysis & Elements of CostDocument14 pagesCost Analysis & Elements of CostvamsikskNo ratings yet

- MACC MAKSI - ACCUMULATING AND ASSIGNING COSTS To PRODUCTDocument30 pagesMACC MAKSI - ACCUMULATING AND ASSIGNING COSTS To PRODUCTlovianicyndiNo ratings yet

- Chapter 2 UpdatedDocument58 pagesChapter 2 Updatedbing bongNo ratings yet

- Engineering CostDocument62 pagesEngineering CostSuleiman BaruniNo ratings yet

- Akb Bab4Document37 pagesAkb Bab4MulyaniNo ratings yet

- Basic Cost ConceptDocument43 pagesBasic Cost ConceptAaron WidofanNo ratings yet

- Chapter No.04 - Process Costing and Hybrid Product-Costing SystemsDocument39 pagesChapter No.04 - Process Costing and Hybrid Product-Costing SystemsWali NoorzadNo ratings yet

- Chap4 (E)Document47 pagesChap4 (E)Kiên Lê TrungNo ratings yet

- Cost Class If CationDocument24 pagesCost Class If CationSanjita TanDonNo ratings yet

- Cost Defined: Introduction To Cost Accounting, Cost Concepts, Cost Behavior Analysis and Cost Accounting CycleDocument4 pagesCost Defined: Introduction To Cost Accounting, Cost Concepts, Cost Behavior Analysis and Cost Accounting Cyclecriselyn agtingNo ratings yet

- Kaplan-M1 Ch2 PDocument22 pagesKaplan-M1 Ch2 PinbyNo ratings yet

- Part III-Managerial AccountingDocument91 pagesPart III-Managerial AccountingGebreNo ratings yet

- CA Notes2Document3 pagesCA Notes2jeyoon13No ratings yet

- Lec 02 Cost ClassificationsDocument97 pagesLec 02 Cost ClassificationsMd Shawfiqul IslamNo ratings yet

- CH 2Document35 pagesCH 2nigoxiy168No ratings yet

- Hilton 11e Chap004 PPT-STUDocument42 pagesHilton 11e Chap004 PPT-STULạnh LùngNo ratings yet

- Chapter 2 Cost Terms Concepts and ClassificationsDocument51 pagesChapter 2 Cost Terms Concepts and ClassificationsMulugeta Girma100% (1)

- Chapter-4: Manufacturing Cost Elements and Cost Estimation For Various ProcessDocument21 pagesChapter-4: Manufacturing Cost Elements and Cost Estimation For Various ProcessTerefa FeyisaNo ratings yet

- Chaitra B Chaitra C MDocument28 pagesChaitra B Chaitra C MChaitra MuralidharaNo ratings yet

- Chapter 1 - Manufacturing AccountDocument32 pagesChapter 1 - Manufacturing AccountNORZAIHA BINTI ALI MoeNo ratings yet

- Chap004, Process CostingDocument17 pagesChap004, Process Costingrief1010No ratings yet

- 10632m Lecture 6 - Full Costing I (Full Version)Document53 pages10632m Lecture 6 - Full Costing I (Full Version)kammiefan215No ratings yet

- Introduction To Managerial Accounting and Cost ConceptsDocument17 pagesIntroduction To Managerial Accounting and Cost ConceptsvanessaNo ratings yet

- Cost Accounting: Introduction To Cost Accounting Lecture-1 Jameel A Khan HakroDocument35 pagesCost Accounting: Introduction To Cost Accounting Lecture-1 Jameel A Khan Hakrokashif aliNo ratings yet

- MS 2Document8 pagesMS 2gabprems11No ratings yet

- Chapter 3Document40 pagesChapter 3Korubel Asegdew YimenuNo ratings yet

- Cost Concepts, Terms and ClassificationsDocument18 pagesCost Concepts, Terms and ClassificationsShennie BeldaNo ratings yet

- Managerial Accounting and Cost Concepts: Chapter TwoDocument63 pagesManagerial Accounting and Cost Concepts: Chapter TwoMd Hasibul Karim 1811766630No ratings yet

- Lecture 2 Cost Terms, Concepts and ClassificationDocument34 pagesLecture 2 Cost Terms, Concepts and ClassificationTgrh TgrhNo ratings yet

- Cost Accounting CycleDocument22 pagesCost Accounting CycleCarla Flor LosiñadaNo ratings yet

- Cost Term, Concept and ClassificationsDocument28 pagesCost Term, Concept and ClassificationskumarNo ratings yet

- Manufacturing Operations: YANTO, 2019 - Ballada, Basic Accounting Made EasyDocument9 pagesManufacturing Operations: YANTO, 2019 - Ballada, Basic Accounting Made EasyDanica MedinaNo ratings yet

- SPPTChap 002Document16 pagesSPPTChap 002saharinshakib7505No ratings yet

- BE 604 - Macrh 24 2022 Class DeckDocument12 pagesBE 604 - Macrh 24 2022 Class DeckChan DavidNo ratings yet

- BE 604 - January 27 2022 Class DeckDocument40 pagesBE 604 - January 27 2022 Class DeckChan DavidNo ratings yet

- Creative Brief Worksheet March 24, 2022Document4 pagesCreative Brief Worksheet March 24, 2022Chan DavidNo ratings yet

- BE 604 January 06 2022 Class DeckDocument18 pagesBE 604 January 06 2022 Class DeckChan DavidNo ratings yet

- BE 604 - March 17 2022 Class DeckDocument50 pagesBE 604 - March 17 2022 Class DeckChan DavidNo ratings yet

- BE 601 Class 4Document57 pagesBE 601 Class 4Chan DavidNo ratings yet

- Ece668: Distribution System Engineering Winter Term 2022Document2 pagesEce668: Distribution System Engineering Winter Term 2022Chan DavidNo ratings yet

- BE 601 Class 1Document34 pagesBE 601 Class 1Chan DavidNo ratings yet

- BE 601 Class 3Document24 pagesBE 601 Class 3Chan DavidNo ratings yet

- BE 604 - January 20 2022 Class DeckDocument19 pagesBE 604 - January 20 2022 Class DeckChan DavidNo ratings yet

- Distribution System Engineering ECE668Document56 pagesDistribution System Engineering ECE668Chan DavidNo ratings yet

- BE 601 Class 2Document17 pagesBE 601 Class 2Chan DavidNo ratings yet

- Notes, 3 (A) : Z Z 1 N I (1,..., N) IDocument3 pagesNotes, 3 (A) : Z Z 1 N I (1,..., N) IChan DavidNo ratings yet

- Notes, 4 (A)Document7 pagesNotes, 4 (A)Chan DavidNo ratings yet

- Notes, 6 (A)Document4 pagesNotes, 6 (A)Chan DavidNo ratings yet

- Notes, 6 (B)Document4 pagesNotes, 6 (B)Chan DavidNo ratings yet

- Notes, 5 (C)Document4 pagesNotes, 5 (C)Chan DavidNo ratings yet

- Notes, 5 (A)Document5 pagesNotes, 5 (A)Chan DavidNo ratings yet

- Notes, 5 (B) : ECE 606 QuicksortDocument5 pagesNotes, 5 (B) : ECE 606 QuicksortChan DavidNo ratings yet

- Notes, 4 (B)Document5 pagesNotes, 4 (B)Chan DavidNo ratings yet

- Notes, 1 (B)Document4 pagesNotes, 1 (B)Chan DavidNo ratings yet

- What Is An "Algorithm?"Document46 pagesWhat Is An "Algorithm?"Chan DavidNo ratings yet

- AlgorithmDocument11 pagesAlgorithmChan DavidNo ratings yet

- ECE 606, Algorithms: Mahesh Tripunitara Tripunit@uwaterloo - Ca ECE, University of WaterlooDocument64 pagesECE 606, Algorithms: Mahesh Tripunitara Tripunit@uwaterloo - Ca ECE, University of WaterlooChan DavidNo ratings yet

- AlgorithmDocument5 pagesAlgorithmChan DavidNo ratings yet

- AlgorithmDocument3 pagesAlgorithmChan DavidNo ratings yet

- ECE 606, Algorithms: Mahesh Tripunitara Tripunit@uwaterloo - Ca ECE, University of WaterlooDocument4 pagesECE 606, Algorithms: Mahesh Tripunitara Tripunit@uwaterloo - Ca ECE, University of WaterlooChan DavidNo ratings yet

- ECE 636: Advanced Analog Integrated Circuits (Fall 2021)Document3 pagesECE 636: Advanced Analog Integrated Circuits (Fall 2021)Chan DavidNo ratings yet

- AlgorithmDocument4 pagesAlgorithmChan DavidNo ratings yet

- AlgorithmDocument6 pagesAlgorithmChan DavidNo ratings yet

- Dr. A. Aziz Bazoune: King Fahd University of Petroleum & MineralsDocument37 pagesDr. A. Aziz Bazoune: King Fahd University of Petroleum & MineralsJoe Jeba RajanNo ratings yet

- Spisak Gledanih Filmova Za 2012Document21 pagesSpisak Gledanih Filmova Za 2012Mirza AhmetovićNo ratings yet

- Mwa 2 - The Legal MemorandumDocument3 pagesMwa 2 - The Legal Memorandumapi-239236545No ratings yet

- Speech by His Excellency The Governor of Vihiga County (Rev) Moses Akaranga During The Closing Ceremony of The Induction Course For The Sub-County and Ward Administrators.Document3 pagesSpeech by His Excellency The Governor of Vihiga County (Rev) Moses Akaranga During The Closing Ceremony of The Induction Course For The Sub-County and Ward Administrators.Moses AkarangaNo ratings yet

- Nespresso Case StudyDocument7 pagesNespresso Case StudyDat NguyenNo ratings yet

- Literature Review On Catfish ProductionDocument5 pagesLiterature Review On Catfish Productionafmzyodduapftb100% (1)

- Hygiene and HealthDocument2 pagesHygiene and HealthMoodaw SoeNo ratings yet

- Promising Anti Convulsant Effect of A Herbal Drug in Wistar Albino RatsDocument6 pagesPromising Anti Convulsant Effect of A Herbal Drug in Wistar Albino RatsIJAR JOURNALNo ratings yet

- 7cc003 Assignment DetailsDocument3 pages7cc003 Assignment Detailsgeek 6489No ratings yet

- (U) Daily Activity Report: Marshall DistrictDocument6 pages(U) Daily Activity Report: Marshall DistrictFauquier NowNo ratings yet

- Bgs Chapter 2Document33 pagesBgs Chapter 2KiranShettyNo ratings yet

- Anti-Epileptic Drugs: - Classification of SeizuresDocument31 pagesAnti-Epileptic Drugs: - Classification of SeizuresgopscharanNo ratings yet

- MOA Agri BaseDocument6 pagesMOA Agri BaseRodj Eli Mikael Viernes-IncognitoNo ratings yet

- Mathematics Trial SPM 2015 P2 Bahagian BDocument2 pagesMathematics Trial SPM 2015 P2 Bahagian BPauling ChiaNo ratings yet

- Cruz-Arevalo v. Layosa DigestDocument2 pagesCruz-Arevalo v. Layosa DigestPatricia Ann RueloNo ratings yet

- Trigonometry Primer Problem Set Solns PDFDocument80 pagesTrigonometry Primer Problem Set Solns PDFderenz30No ratings yet

- PSYC1111 Ogden Psychology of Health and IllnessDocument108 pagesPSYC1111 Ogden Psychology of Health and IllnessAleNo ratings yet

- Far Eastern University-Institute of Nursing In-House NursingDocument25 pagesFar Eastern University-Institute of Nursing In-House Nursingjonasdelacruz1111No ratings yet

- Factor Causing Habitual Viewing of Pornographic MaterialDocument64 pagesFactor Causing Habitual Viewing of Pornographic MaterialPretzjay BensigNo ratings yet

- MGT501 Final Term MCQs + SubjectiveDocument33 pagesMGT501 Final Term MCQs + SubjectiveAyesha Abdullah100% (1)

- SuperconductorDocument33 pagesSuperconductorCrisanta GanadoNo ratings yet

- Complete Admin Law OutlineDocument135 pagesComplete Admin Law Outlinemarlena100% (1)

- Jordana Wagner Leadership Inventory Outcome 2Document22 pagesJordana Wagner Leadership Inventory Outcome 2api-664984112No ratings yet

- Site Master S113C, S114C, S331C, S332C, Antenna, Cable and Spectrum AnalyzerDocument95 pagesSite Master S113C, S114C, S331C, S332C, Antenna, Cable and Spectrum AnalyzerKodhamagulla SudheerNo ratings yet

- Concrete Design Using PROKONDocument114 pagesConcrete Design Using PROKONHesham Mohamed100% (2)

- Chapter 3 - the-WPS OfficeDocument15 pagesChapter 3 - the-WPS Officekyoshiro RyotaNo ratings yet

- Multicutural LiteracyDocument3 pagesMulticutural LiteracyMark Alfred AlemanNo ratings yet

- Leisure TimeDocument242 pagesLeisure TimeArdelean AndradaNo ratings yet

- Effect of Intensive Health Education On Adherence To Treatment in Sputum Positive Pulmonary Tuberculosis PatientsDocument6 pagesEffect of Intensive Health Education On Adherence To Treatment in Sputum Positive Pulmonary Tuberculosis PatientspocutindahNo ratings yet

- Modern DrmaDocument7 pagesModern DrmaSHOAIBNo ratings yet