You might also like

- Deed of ReconveyanceDocument1 pageDeed of ReconveyanceKaren DyNo ratings yet

- Massey Ferguson Case StudyDocument10 pagesMassey Ferguson Case StudyStephen Kim100% (3)

- Module 1-3 ACCTG 201Document32 pagesModule 1-3 ACCTG 201Sky SoronoiNo ratings yet

- 2015-2014 June 30 The Florida Bar Financial StatementsDocument35 pages2015-2014 June 30 The Florida Bar Financial StatementsNeil GillespieNo ratings yet

- Assignment 2Document12 pagesAssignment 2Geetu SharmaNo ratings yet

- Cost Classifications: Learning ObjectivesDocument32 pagesCost Classifications: Learning ObjectivesKhánh Đoan NgôNo ratings yet

- Cost Defined: Introduction To Cost Accounting, Cost Concepts, Cost Behavior Analysis and Cost Accounting CycleDocument4 pagesCost Defined: Introduction To Cost Accounting, Cost Concepts, Cost Behavior Analysis and Cost Accounting Cyclecriselyn agtingNo ratings yet

- Ca NotesDocument36 pagesCa Notesretchiel love calinogNo ratings yet

- Chapter 2 Cost Terms Concepts and ClassificationsDocument51 pagesChapter 2 Cost Terms Concepts and ClassificationsMulugeta Girma100% (1)

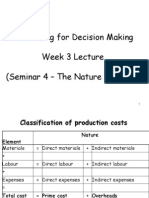

- Accounting For Decision Making Week 3 Lecture (Seminar 4 - The Nature of Costs)Document51 pagesAccounting For Decision Making Week 3 Lecture (Seminar 4 - The Nature of Costs)nwcbenny337No ratings yet

- Cost Terminologies and ClassficationsDocument51 pagesCost Terminologies and ClassficationsLim Jie XiNo ratings yet

- Basic Cost Management ConceptsDocument7 pagesBasic Cost Management ConceptsHeizeruNo ratings yet

- Cost Terms, Concepts, and ClassificationDocument27 pagesCost Terms, Concepts, and ClassificationParadise VillageNo ratings yet

- 3 Classification of Cost CMA Inter Costing Fast Track ClassDocument18 pages3 Classification of Cost CMA Inter Costing Fast Track ClassLeviNo ratings yet

- 10632m Lecture 6 - Full Costing I (Full Version)Document53 pages10632m Lecture 6 - Full Costing I (Full Version)kammiefan215No ratings yet

- Chapter 4: Type of Cost: Direct Costs (Prime Costs) Indirect Costs (Overheads)Document8 pagesChapter 4: Type of Cost: Direct Costs (Prime Costs) Indirect Costs (Overheads)Claudia WongNo ratings yet

- Chapter 2 Cost Accounting ConceptsDocument22 pagesChapter 2 Cost Accounting ConceptsRosliana RazabNo ratings yet

- Presentation 04 (1slide-Pg)Document33 pagesPresentation 04 (1slide-Pg)araika.maksutNo ratings yet

- Chapter 2 - Managerial Acc. & Cost ConceptsDocument23 pagesChapter 2 - Managerial Acc. & Cost ConceptsMuhammad Ali KazmiNo ratings yet

- Chapter 2Document5 pagesChapter 2Hania M. CalandadaNo ratings yet

- Topic 2 IDocument16 pagesTopic 2 Iami zawaniNo ratings yet

- CN #2 - CVP AnalysisDocument5 pagesCN #2 - CVP AnalysisRen EyNo ratings yet

- Cost Concepts Classification BehaviorDocument46 pagesCost Concepts Classification BehaviorrhearomefranciscoNo ratings yet

- Managerial Accounting and Cost ConceptsDocument6 pagesManagerial Accounting and Cost ConceptsJUST KINGNo ratings yet

- Chapter 02 - Cost Term and Concepts FinalDocument60 pagesChapter 02 - Cost Term and Concepts FinalAminaMatinNo ratings yet

- Accounting 2Document5 pagesAccounting 2jessicaong2403No ratings yet

- Chapter 1Document4 pagesChapter 1Tricia Rozl PimentelNo ratings yet

- Cost ClassificationDocument6 pagesCost ClassificationAnonymous yy8In96j0r100% (1)

- 1b - Cost Concepts and Terminology - 14sept06Document31 pages1b - Cost Concepts and Terminology - 14sept06Zaid AnsariNo ratings yet

- Cost Accounting Concepts: Prof. Dr. Farid MoharamDocument90 pagesCost Accounting Concepts: Prof. Dr. Farid Moharammohamed el kadyNo ratings yet

- Ilovepdf MergedDocument34 pagesIlovepdf Mergeddivyanshi singhNo ratings yet

- Introduction To Cost and Management AccountingDocument31 pagesIntroduction To Cost and Management AccountingTestNo ratings yet

- Chapter 3 - Virtual - Classroom-M.Document61 pagesChapter 3 - Virtual - Classroom-M.rebeccahf7No ratings yet

- Chapter 2 Cost ClassificationsDocument18 pagesChapter 2 Cost Classificationsmarizemeyer2No ratings yet

- Part III-Managerial AccountingDocument91 pagesPart III-Managerial AccountingGebreNo ratings yet

- Supplementary 1 - Cost ClassificationDocument26 pagesSupplementary 1 - Cost ClassificationNguyen Tuan Anh (BTEC HN)No ratings yet

- CA Notes2Document3 pagesCA Notes2jeyoon13No ratings yet

- Managerial Accounting and Cost Concepts: Chapter TwoDocument63 pagesManagerial Accounting and Cost Concepts: Chapter TwoMd Hasibul Karim 1811766630No ratings yet

- 07 Module 03 AVC PDFDocument12 pages07 Module 03 AVC PDFMarriah Izzabelle Suarez RamadaNo ratings yet

- Cost Concepts HandoutsDocument13 pagesCost Concepts HandoutsTushar DuaNo ratings yet

- Basic Cost ConceptDocument43 pagesBasic Cost ConceptAaron WidofanNo ratings yet

- Unit - 3 Cost Accounting PDFDocument19 pagesUnit - 3 Cost Accounting PDFShreyash PardeshiNo ratings yet

- Sesi 2 Akuntansi Manajemen - Rev1Document32 pagesSesi 2 Akuntansi Manajemen - Rev1Dian Permata SariNo ratings yet

- Cost Concepts and ClassificationDocument8 pagesCost Concepts and ClassificationJericho PagsuguironNo ratings yet

- CH 02Document40 pagesCH 02hoangmyduyennguyen2004No ratings yet

- Cost Accounting Part 1Document21 pagesCost Accounting Part 1Mostafa ElgendyNo ratings yet

- CH 02Document40 pagesCH 02lyonanh289No ratings yet

- Summary Chapter 4Document3 pagesSummary Chapter 4ninarizkitaNo ratings yet

- Chapter 2 - Managerial Cost Concepts and Cost Behaviour AnalysisDocument53 pagesChapter 2 - Managerial Cost Concepts and Cost Behaviour AnalysisPRAkriT POUdeLNo ratings yet

- Elements of Costs AND Classification of Expenditure: Asst. Prof. Joseph George Konnully, MJCETDocument14 pagesElements of Costs AND Classification of Expenditure: Asst. Prof. Joseph George Konnully, MJCETJoseph George KonnullyNo ratings yet

- Chapter 2 (Reviewer)Document3 pagesChapter 2 (Reviewer)Erika May EndencioNo ratings yet

- Cost TerminologyDocument2 pagesCost TerminologyChristine TutorNo ratings yet

- 5 - Cost Concepts and ClassificationsDocument31 pages5 - Cost Concepts and ClassificationsAlyssa TolcidasNo ratings yet

- Lecture 2 - Acc204Document4 pagesLecture 2 - Acc204ALYZA NICOLE CALLEJANo ratings yet

- Managerial Accounting Creating Value in A Dynamic Business Environment Hilton 10th Edition Solutions ManualDocument11 pagesManagerial Accounting Creating Value in A Dynamic Business Environment Hilton 10th Edition Solutions Manualbarrenlywale1ibn8No ratings yet

- 1a Cost Classification Form Manufacturing PT of View and Predicting Cost Behaviour - 19 - 12 - 2023Document12 pages1a Cost Classification Form Manufacturing PT of View and Predicting Cost Behaviour - 19 - 12 - 2023Md Rashadul IslamNo ratings yet

- Cost Accounting 1 8 PDFDocument110 pagesCost Accounting 1 8 PDFHashim Mahmood KhanNo ratings yet

- Chapter 1 IntroductionDocument46 pagesChapter 1 IntroductionIrzam ZairyNo ratings yet

- Cost Accounting SystemsDocument4 pagesCost Accounting SystemsEDELYN PoblacionNo ratings yet

- Cost ClassificationDocument19 pagesCost ClassificationAli AshhabNo ratings yet

- Week 2-Basic Cost ManagementDocument21 pagesWeek 2-Basic Cost ManagementRichard Oliver CortezNo ratings yet

- Review Chapter 1-2-4-18Document55 pagesReview Chapter 1-2-4-18hoangmyduyennguyen2004No ratings yet

- Management Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesFrom EverandManagement Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesNo ratings yet

- 1 1-KTQTe1Document1 page1 1-KTQTe1040404.anniNo ratings yet

- Kế toán quốc tế IDocument6 pagesKế toán quốc tế I040404.anniNo ratings yet

- Exercise International Acc 1 GroupDocument11 pagesExercise International Acc 1 Group040404.anniNo ratings yet

- Chapter 5 - Relevant Information and Decision MakingDocument56 pagesChapter 5 - Relevant Information and Decision Making040404.anniNo ratings yet

- Essay KT căn bảnDocument1 pageEssay KT căn bản040404.anniNo ratings yet

- KT quốc tếDocument1 pageKT quốc tế040404.anniNo ratings yet

- Form 4A: General Consumption Tax ReturnDocument2 pagesForm 4A: General Consumption Tax ReturnSi KiNo ratings yet

- Aditya Karulkar Diane Leblanc Sami Matta Mrudu NairDocument14 pagesAditya Karulkar Diane Leblanc Sami Matta Mrudu NairMrudu NairNo ratings yet

- VWAPDocument8 pagesVWAPKarthick Annamalai50% (2)

- Report IFA For Norway On Interest DeductionDocument19 pagesReport IFA For Norway On Interest DeductionAnna ScaoaNo ratings yet

- AJCL - Public-Private PartnershipsDocument31 pagesAJCL - Public-Private PartnershipsJohn JohnsonNo ratings yet

- Tax Invoice: Redmi Note 5 Pro (Gold, 64 GB)Document1 pageTax Invoice: Redmi Note 5 Pro (Gold, 64 GB)Mohammad Rafiq DarNo ratings yet

- Certificate in Accounting (IAS) Level 3/series 3-2009Document14 pagesCertificate in Accounting (IAS) Level 3/series 3-2009Hein Linn Kyaw75% (4)

- CBC Blue Book: Market ReviewDocument36 pagesCBC Blue Book: Market ReviewColdwell Banker CommercialNo ratings yet

- Ys%, XLD M Dka S%L Iudcjd Ckrcfha .Eiü M %H: The Gazette of The Democratic Socialist Republic of Sri LankaDocument10 pagesYs%, XLD M Dka S%L Iudcjd Ckrcfha .Eiü M %H: The Gazette of The Democratic Socialist Republic of Sri LankaAnuruddhaNo ratings yet

- Accountant Advice 2020Document306 pagesAccountant Advice 2020Jerald MirandaNo ratings yet

- Homeowners Savings and Loan Bank vs. FeloniaDocument4 pagesHomeowners Savings and Loan Bank vs. FeloniaLoren MandaNo ratings yet

- Foundations in Accountancy FFA/ACCA FDocument45 pagesFoundations in Accountancy FFA/ACCA FTuyết Anh ĐồngNo ratings yet

- 9 StatementOfAccount-September2023Document3 pages9 StatementOfAccount-September2023cailinghoneygenNo ratings yet

- Business Math Week 9Document10 pagesBusiness Math Week 9황혜진No ratings yet

- Board-2011 Aof QTR 3Document7 pagesBoard-2011 Aof QTR 3EllenBeth WachsNo ratings yet

- Sales and Leases OutlineDocument4 pagesSales and Leases OutlinerusselldanielNo ratings yet

- Gilead CaseDocument22 pagesGilead CaseTaruntej SinghNo ratings yet

- A Sample Flower Shop Business Plan TemplateDocument14 pagesA Sample Flower Shop Business Plan TemplateAljon NojLa YapNo ratings yet

- Financial Performance Evaluation Using RATIO ANALYSISDocument31 pagesFinancial Performance Evaluation Using RATIO ANALYSISGurvinder Arora100% (1)

- Acc GroupDocument19 pagesAcc GroupAhmad Aqeef Kamar ZamanNo ratings yet

- First Long Quiz COSMANDocument5 pagesFirst Long Quiz COSMANby ScribdNo ratings yet

- On TATA AIGDocument11 pagesOn TATA AIGakshayNo ratings yet

- Adjusting Entries, 10-Column WorksheetDocument21 pagesAdjusting Entries, 10-Column WorksheetRachelNo ratings yet

- Project On Maruti Suzuki ModifiedDocument83 pagesProject On Maruti Suzuki ModifiedSumit Kumar100% (1)

- Law Mock TestDocument8 pagesLaw Mock TestHemant AherNo ratings yet

- Cambodian Chinese Medical Association: Pay Slip - January, 2022Document25 pagesCambodian Chinese Medical Association: Pay Slip - January, 2022VichhaiJacksonNo ratings yet