You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5814)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Dhandho Investor ReviewDocument4 pagesThe Dhandho Investor ReviewKiamalchikNo ratings yet

- Treasury Bills: Getting The Price From The Interest RateDocument2 pagesTreasury Bills: Getting The Price From The Interest RateAnav AggarwalNo ratings yet

- A Framework For Analyzing Yield Curve Trades - Salomon BrothersDocument28 pagesA Framework For Analyzing Yield Curve Trades - Salomon BrothersRR886No ratings yet

- Intacc 3 Cash Flow QuizDocument13 pagesIntacc 3 Cash Flow QuizRica RegorisNo ratings yet

- ACCT403-Accounting For InventoryDocument63 pagesACCT403-Accounting For InventoryMary AmoNo ratings yet

- TSTW24Document37 pagesTSTW24Nije AsriNo ratings yet

- Consolidation Techniques and ProceduresDocument48 pagesConsolidation Techniques and ProceduresSausan SaniaNo ratings yet

- Equity SharesDocument25 pagesEquity Sharessharanjeet88% (8)

- GS09 Quick Guide enDocument12 pagesGS09 Quick Guide enRR886No ratings yet

- Diebold MarianoDocument11 pagesDiebold MarianoRR886No ratings yet

- Course Notes Stochastic Processes - AucklandDocument195 pagesCourse Notes Stochastic Processes - AucklandRR886No ratings yet

- Kupiec Paul Techniques For Verifying The Accuracy of Risk Measurement ModelsDocument12 pagesKupiec Paul Techniques For Verifying The Accuracy of Risk Measurement ModelsRR886No ratings yet

- Course Notes On Computational FinanceDocument94 pagesCourse Notes On Computational FinanceRR886No ratings yet

- NH Weekly August 02 2021-EnglishDocument10 pagesNH Weekly August 02 2021-EnglishPutu Chantika Putri DhammayantiNo ratings yet

- Chap4-The Valuation of Long-Term Securities (Van Horne)Document3 pagesChap4-The Valuation of Long-Term Securities (Van Horne)Claudine Duhapa100% (1)

- Tokenization of Real Estate AssetsDocument2 pagesTokenization of Real Estate AssetsSheine Girao-SaponNo ratings yet

- What Is Dynamic Pricing StrategyDocument5 pagesWhat Is Dynamic Pricing Strategypriyanshu.ryp01No ratings yet

- BD5 SM31Document2 pagesBD5 SM31ksgNo ratings yet

- Reconstruct Journal Entries at The End of Its First YearDocument1 pageReconstruct Journal Entries at The End of Its First YearLet's Talk With HassanNo ratings yet

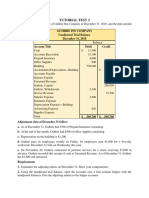

- Tutorial Test 3Document2 pagesTutorial Test 3b1112014041No ratings yet

- Accounting Ae2023Document2 pagesAccounting Ae2023elsana philipNo ratings yet

- Maturity Apple KasusDocument11 pagesMaturity Apple KasusSepta SkundarianNo ratings yet

- Limits of VaRDocument5 pagesLimits of VaRangieendNo ratings yet

- Treasury Management: Indian and International PerspectiveDocument24 pagesTreasury Management: Indian and International PerspectiveSahil WadhwaNo ratings yet

- FUNDAFINDocument2 pagesFUNDAFINSrinivas GopalNo ratings yet

- Asian Paints Annual Report 2016-17Document2 pagesAsian Paints Annual Report 2016-17Amit Pandey0% (1)

- FM - Chapter 3 - QuizDocument8 pagesFM - Chapter 3 - QuizHausland Const. Corp.No ratings yet

- International Corporate Finance 11 Edition: by Jeff MaduraDocument32 pagesInternational Corporate Finance 11 Edition: by Jeff MaduraDun DunNo ratings yet

- Chapter 1 CLCDocument17 pagesChapter 1 CLCLinh BùiNo ratings yet

- Ebd 418Document366 pagesEbd 418Devy RahmawatiNo ratings yet

- East Hill Home Healthcare Services Was Organized On January 1Document1 pageEast Hill Home Healthcare Services Was Organized On January 1trilocksp SinghNo ratings yet

- Chapter 3 SummaryDocument3 pagesChapter 3 SummaryDarlianne Klyne BayerNo ratings yet

- Smallcases Mi25 Mi30 Mi40 Mi50: Product Comparison (Other Than) Feature/ProductDocument1 pageSmallcases Mi25 Mi30 Mi40 Mi50: Product Comparison (Other Than) Feature/ProductMehran AvNo ratings yet

- 6.1a Black-Scholes-Merton FormulasDocument25 pages6.1a Black-Scholes-Merton FormulasAnDy YiMNo ratings yet

- Arora Et - Al. (2012) - Counterparty Credit Risk and The Credit Default Swap MarketDocument14 pagesArora Et - Al. (2012) - Counterparty Credit Risk and The Credit Default Swap MarketyeyenNo ratings yet

- Online Test 3 - Cost of CapitalDocument16 pagesOnline Test 3 - Cost of CapitalShereena FarhoudNo ratings yet