You might also like

- Kiln Girth Gear Before Stitch Wleding 150309 11amDocument3 pagesKiln Girth Gear Before Stitch Wleding 150309 11amSunil T V SuniNo ratings yet

- MQDocument4 pagesMQJOMARY AGALEDNo ratings yet

- Bombers and SeagullsDocument8 pagesBombers and SeagullshpgeraldNo ratings yet

- Measurement Sheet of Log No. 101Document5 pagesMeasurement Sheet of Log No. 101ejazNo ratings yet

- Efe, Ife, CPM, QSPM MatrixDocument6 pagesEfe, Ife, CPM, QSPM MatrixYousab Kaldas100% (1)

- His To GramaDocument308 pagesHis To GramaJavier Bustos CastroNo ratings yet

- Bill 075556656923Document1 pageBill 075556656923Sa AlmNo ratings yet

- Grafico P Muestras Yulisa HernmandezDocument3 pagesGrafico P Muestras Yulisa HernmandezCarvajal YulissaNo ratings yet

- Mehran University of Engineering and Technology, JamshoroDocument6 pagesMehran University of Engineering and Technology, JamshoroMuhammad Fahad AliNo ratings yet

- Detail Meja LipatDocument6 pagesDetail Meja Lipatwidibae jokotholeNo ratings yet

- Chart Title Chart TitleDocument11 pagesChart Title Chart TitleAneesh KumarNo ratings yet

- IncertidumbreDocument3 pagesIncertidumbreJuan SantiagoNo ratings yet

- Ejemplo de Aplicación: Evaluación Numérica de La Respuesta Dinámica - NewmarkDocument1 pageEjemplo de Aplicación: Evaluación Numérica de La Respuesta Dinámica - NewmarkLuis Fenco GonzalesNo ratings yet

- PROCUREMENT2010Document1 pagePROCUREMENT2010Biplab SwainNo ratings yet

- Dsipo 1Document4 pagesDsipo 1Douglas Pariona MoyaNo ratings yet

- Waterflooding 3 y 4Document8 pagesWaterflooding 3 y 4Jorge Blanco ChoqueNo ratings yet

- Vpip PFR Robo Check-Raise Re-Subir Fold To 3-BetDocument2 pagesVpip PFR Robo Check-Raise Re-Subir Fold To 3-BetJohn Steven VelasquezNo ratings yet

- Conversion of Working HoursDocument1 pageConversion of Working HoursJean Valerie BrandonNo ratings yet

- Crca CRM Diversion '22-23Document5 pagesCrca CRM Diversion '22-23ram kum,arNo ratings yet

- Revenue Leakage 07172019Document30 pagesRevenue Leakage 07172019AnkushNo ratings yet

- Calculo Custos Por EmpregadoDocument3 pagesCalculo Custos Por EmpregadoFabio.soares RhNo ratings yet

- Commercial Sieve Mesh DimensionsDocument9 pagesCommercial Sieve Mesh DimensionsMuhammad MuneebNo ratings yet

- Heave Acceleration ChartDocument1 pageHeave Acceleration Chartakash808099No ratings yet

- Practica 7 Quimica AnaliticaDocument3 pagesPractica 7 Quimica AnaliticaKenny CarreraNo ratings yet

- Simula Encargos 1.2Document2 pagesSimula Encargos 1.2Fabio.soares RhNo ratings yet

- B) " Data - Frame".: Outliers and Missing Values (8 Marks) AnswerDocument23 pagesB) " Data - Frame".: Outliers and Missing Values (8 Marks) AnswerRaveendra Babu Gaddam100% (1)

- M Furqon Habibie - F44180092Document5 pagesM Furqon Habibie - F44180092Furqon HabibieNo ratings yet

- Putaran Sudut Rol SAP Putaran Sudut Rol PengujianDocument12 pagesPutaran Sudut Rol SAP Putaran Sudut Rol Pengujianauliya nafisaNo ratings yet

- Ejemplo CinematicaDocument1 pageEjemplo CinematicaCaleb BavingNo ratings yet

- BarbacoaDocument3 pagesBarbacoaEdwin Ocaña RamosNo ratings yet

- Harsha AssignmentDocument4 pagesHarsha Assignmentsaibhargav2209No ratings yet

- Calibracion Materiales InterpolacionDocument8 pagesCalibracion Materiales InterpolacionKatherine BautistaNo ratings yet

- Kurva Kalibrasi Kelas A Kurva Kalibrasi Kelas C Kurva Kalibrasi Kelas D Kurva Kalibrasi Kelas BDocument2 pagesKurva Kalibrasi Kelas A Kurva Kalibrasi Kelas C Kurva Kalibrasi Kelas D Kurva Kalibrasi Kelas BDella MeiliaNo ratings yet

- Table 13-1 Perrys Chemical Engineering Handbook 7th EdDocument1 pageTable 13-1 Perrys Chemical Engineering Handbook 7th EdBun YaminNo ratings yet

- Subject Code Subject Name Year X Semester X Mid Sem Exam Results 20Xx Laqs (15 Marks Each)Document10 pagesSubject Code Subject Name Year X Semester X Mid Sem Exam Results 20Xx Laqs (15 Marks Each)Aida WaniNo ratings yet

- Part A (B) - Chemical Engineers Handbook, Perry Vol 1Document1 pagePart A (B) - Chemical Engineers Handbook, Perry Vol 1Jia Yuan ChngNo ratings yet

- Illustration On Pillar Score CalculationDocument3 pagesIllustration On Pillar Score Calculationayu aryistaNo ratings yet

- Tensile Load Vs LengthDocument25 pagesTensile Load Vs LengthGirish DNo ratings yet

- Conversion of Working HoursDocument1 pageConversion of Working HoursLizjasmine DimayaNo ratings yet

- Graph of Theoretical Values Vs SimulatedDocument4 pagesGraph of Theoretical Values Vs Simulatedaakorley01No ratings yet

- Laporan Kendali Fuzzy Logic Kelompok RianDocument11 pagesLaporan Kendali Fuzzy Logic Kelompok RianNina FloydNo ratings yet

- Data Tugas StatstDocument3 pagesData Tugas StatstNur KomariahNo ratings yet

- Clase 04-10-2019Document12 pagesClase 04-10-2019KIKA CONTENTONo ratings yet

- Aggregate ClaimsDocument3 pagesAggregate ClaimsEdgar Alexander Hernández RebolledoNo ratings yet

- No Size Konsentrasi Titran HCL Massa Sampel (M) Konsentrasi Analit (Ch3Cooh) (M) Awal Akhir 1 1Document2 pagesNo Size Konsentrasi Titran HCL Massa Sampel (M) Konsentrasi Analit (Ch3Cooh) (M) Awal Akhir 1 1indah dwi lestariNo ratings yet

- Tabla Conversion Combustible CM - GalDocument35 pagesTabla Conversion Combustible CM - GalJulieta TaveraNo ratings yet

- Tabla Conversion Combustible CM - GalDocument35 pagesTabla Conversion Combustible CM - GalJulieta TaveraNo ratings yet

- Exemplo de Granulometria Correta - Aula10Document9 pagesExemplo de Granulometria Correta - Aula10Sandro Dias PenaNo ratings yet

- Dokaznice Količina OktobarDocument1 pageDokaznice Količina OktobarBurazBurazNo ratings yet

- Coefficients v1 1cDocument6 pagesCoefficients v1 1cRekha PandeyNo ratings yet

- Horas Hombres CapacitacionDocument1 pageHoras Hombres Capacitacionperucho20032003No ratings yet

- DLC GradingDocument9 pagesDLC GradingAshok kumarNo ratings yet

- Expt 6Document11 pagesExpt 6nooneNo ratings yet

- Example 3.32 Area Under ROCDocument2 pagesExample 3.32 Area Under ROCNiger RomeNo ratings yet

- Iapm 19.09Document19 pagesIapm 19.09NISCHAL UPRETINo ratings yet

- Fill Grid 1 2 3 4 5 Points Area Total Average Fill: Estimate Work SheetDocument3 pagesFill Grid 1 2 3 4 5 Points Area Total Average Fill: Estimate Work SheetraviNo ratings yet

- Caso 4 InventariosDocument8 pagesCaso 4 InventariosClari ClaritaNo ratings yet

- Procemin 2015 Flotation Plant Design With Aminfloat SimulatorDocument24 pagesProcemin 2015 Flotation Plant Design With Aminfloat SimulatorNereo SpenglerNo ratings yet

- Math Practice Simplified: Decimals & Percents (Book H): Practicing the Concepts of Decimals and PercentagesFrom EverandMath Practice Simplified: Decimals & Percents (Book H): Practicing the Concepts of Decimals and PercentagesRating: 5 out of 5 stars5/5 (3)

- Activity 14: International Financial Markets and Innovations 1. Explain What Is International Financial MarketDocument2 pagesActivity 14: International Financial Markets and Innovations 1. Explain What Is International Financial MarketNJ Sibbaluca DeriloNo ratings yet

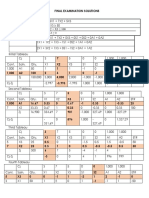

- Final Examination SolutionsDocument5 pagesFinal Examination SolutionsNJ Sibbaluca DeriloNo ratings yet

- IMpact of IT To Business OperationDocument1 pageIMpact of IT To Business OperationNJ Sibbaluca DeriloNo ratings yet

- Chapter 4 Product and Service DesignDocument40 pagesChapter 4 Product and Service DesignLuarn WeiNo ratings yet

- Comp-XM Basix Guide PDFDocument6 pagesComp-XM Basix Guide PDFJai PhookanNo ratings yet

- Are Taxes EvilDocument5 pagesAre Taxes Evilpokeball0010% (1)

- CCL Products - Initiating Coverage - 09092019 - 11!09!2019 - 08Document29 pagesCCL Products - Initiating Coverage - 09092019 - 11!09!2019 - 08Amit PatelNo ratings yet

- Financial Management For Engineers Fall 2021 Calculating Yield (Bond) Using BA II Plus CalculatorDocument5 pagesFinancial Management For Engineers Fall 2021 Calculating Yield (Bond) Using BA II Plus CalculatorRussul Al-RawiNo ratings yet

- Tambunting v. CADocument9 pagesTambunting v. CAAlex FelicesNo ratings yet

- The Companies Ordinance 2017 Company Limited by Shares Articles of Association of Al-Abbas Seed PROCESSING Private Limited CompaniesDocument7 pagesThe Companies Ordinance 2017 Company Limited by Shares Articles of Association of Al-Abbas Seed PROCESSING Private Limited Companiesabbs khanNo ratings yet

- Building Pro-Forma Financial Statements Comparables Net Present Value Method The Venture Capital MethodDocument6 pagesBuilding Pro-Forma Financial Statements Comparables Net Present Value Method The Venture Capital MethodKarya BangunanNo ratings yet

- Saturn Retrograde Will Trigger Global RecessionDocument26 pagesSaturn Retrograde Will Trigger Global RecessionmichaNo ratings yet

- Jayshree Periwal High School: AccountsDocument8 pagesJayshree Periwal High School: AccountsShreekumar MaheshwariNo ratings yet

- United States Bankruptcy Court For The District of DelawareDocument9 pagesUnited States Bankruptcy Court For The District of DelawareChapter 11 DocketsNo ratings yet

- Sol. Man. - Chapter 13 - Partnership DissolutionDocument16 pagesSol. Man. - Chapter 13 - Partnership DissolutionJaymark RueloNo ratings yet

- AMCO-11006822-V1-Prosus N V ProspectusDocument426 pagesAMCO-11006822-V1-Prosus N V ProspectussuedelopeNo ratings yet

- Proposed Rule: Medical Benefits: Medical Care or Services Reasonable ChargesDocument4 pagesProposed Rule: Medical Benefits: Medical Care or Services Reasonable ChargesJustia.comNo ratings yet

- Ug Scholarships at Iit KGPDocument5 pagesUg Scholarships at Iit KGPPriyank AgrawalNo ratings yet

- TOC of Pre Feasibility Report On Five Star HotelDocument6 pagesTOC of Pre Feasibility Report On Five Star Hotelbrainkrusherz0% (1)

- Southwind AflDocument42 pagesSouthwind Aflpraviny100% (1)

- C3 Crafting & Executing Strategy 21eDocument62 pagesC3 Crafting & Executing Strategy 21eMuthia Khairani100% (1)

- Myanmar APGevaluationDocument207 pagesMyanmar APGevaluationKashishBansalNo ratings yet

- Teuer Furniture Case A DCFDocument28 pagesTeuer Furniture Case A DCFShilpi Jain100% (2)

- Computation Part2Document4 pagesComputation Part2Jeane Mae BooNo ratings yet

- Muh. SyukurDocument6 pagesMuh. SyukurDrawing For LifeNo ratings yet

- Introduction To Cost AccountingDocument2 pagesIntroduction To Cost AccountingHunson AbadeerNo ratings yet

- Kanika Khurana: 2018. Clients Experience IncludesDocument3 pagesKanika Khurana: 2018. Clients Experience IncludesjfrNo ratings yet

- An Assignment On TFO UCBLDocument15 pagesAn Assignment On TFO UCBLFahim Dad KhanNo ratings yet

- Solution Manual For Intermediate Accounting IFRS 4th Edition by Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield Chapter 1 - 24Document70 pagesSolution Manual For Intermediate Accounting IFRS 4th Edition by Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield Chapter 1 - 24marcuskenyatta27550% (2)

- 2020 Appraiser's Exam Mock Exam Set GDocument5 pages2020 Appraiser's Exam Mock Exam Set GMarkein Dael VirtudazoNo ratings yet

- Functions of National Small Industries Corporation (NSIC)Document14 pagesFunctions of National Small Industries Corporation (NSIC)Naveen Jacob JohnNo ratings yet

- QF5205 1011sem2Document3 pagesQF5205 1011sem2sunnysantraNo ratings yet

- Chapter-7 Investment ManagementDocument7 pagesChapter-7 Investment Managementhasan alNo ratings yet

- Chuidian V Sandiganbayan Rule 57Document2 pagesChuidian V Sandiganbayan Rule 57KISSINGER REYESNo ratings yet