You might also like

- AP03 Audit of Inventories QDocument6 pagesAP03 Audit of Inventories Qbobo kaNo ratings yet

- MASTERY CLASS IN AUDITING PROBLEMS Part 1 Prob 1 9Document35 pagesMASTERY CLASS IN AUDITING PROBLEMS Part 1 Prob 1 9Mark Gelo WinchesterNo ratings yet

- Excel Professional Services, Inc.: Discussion QuestionsDocument4 pagesExcel Professional Services, Inc.: Discussion QuestionsSadAccountantNo ratings yet

- Standard Audit Programme Guide: SAPG Ref.: Function: Stock & Materials Handling Activity/System: Stock ControlDocument13 pagesStandard Audit Programme Guide: SAPG Ref.: Function: Stock & Materials Handling Activity/System: Stock Control06l01a0224No ratings yet

- Audit of Accounts Receivable and Related Accounts1Document5 pagesAudit of Accounts Receivable and Related Accounts1CJ alandyNo ratings yet

- Applied Auditing Audit of Cash and ReceivablesDocument2 pagesApplied Auditing Audit of Cash and ReceivablesCar Mae LaNo ratings yet

- Correct Inventory Balances and Audit of Sales/Purchase Cut-OffDocument10 pagesCorrect Inventory Balances and Audit of Sales/Purchase Cut-OffMarkie GrabilloNo ratings yet

- Audit of Receivables at Far Eastern UniversityDocument6 pagesAudit of Receivables at Far Eastern UniversityKenneth A. S. AlabadoNo ratings yet

- Audit of Investments - Set ADocument4 pagesAudit of Investments - Set AZyrah Mae SaezNo ratings yet

- Problem No.1: D. P147,000 C. P349,000 C. P639,000Document6 pagesProblem No.1: D. P147,000 C. P349,000 C. P639,000debate ddNo ratings yet

- ReSA B43 FAR First PB Exam Questions Answers SolutionsDocument14 pagesReSA B43 FAR First PB Exam Questions Answers Solutionsrtenaja100% (1)

- Responsibility Accounting Concepts and CalculationsDocument5 pagesResponsibility Accounting Concepts and CalculationsRenNo ratings yet

- 240 (Revised) - PSA 240 (Revised)Document41 pages240 (Revised) - PSA 240 (Revised)Andreiu Mark Salvador EsmeleNo ratings yet

- CPAR B94 FAR Final PB Exam - Answers - SolutionsDocument8 pagesCPAR B94 FAR Final PB Exam - Answers - SolutionsJazehl ValdezNo ratings yet

- Answers Managerial Accounting Prelim ExaminationDocument4 pagesAnswers Managerial Accounting Prelim ExaminationRegine ReyesNo ratings yet

- Auditing ProblemsDocument6 pagesAuditing ProblemsMaurice AgbayaniNo ratings yet

- Theories ReceivableDocument26 pagesTheories ReceivableMark Gelo WinchesterNo ratings yet

- Escorido Malfarta Accounts ReceivableDocument41 pagesEscorido Malfarta Accounts ReceivableAna Marie EscoridoNo ratings yet

- Chapter 4 Caselette Audit of ReceivablesDocument37 pagesChapter 4 Caselette Audit of ReceivablesXXXXXXXXXXXXXXXXXXNo ratings yet

- UdD 2nd Semester PRE02 Auditing and Assurance Concepts and Applications Midterm 1Document16 pagesUdD 2nd Semester PRE02 Auditing and Assurance Concepts and Applications Midterm 1Roland CatubigNo ratings yet

- Auditing Problems Intangibles Impairment and Revaluation PDFDocument44 pagesAuditing Problems Intangibles Impairment and Revaluation PDFMark Domingo MendozaNo ratings yet

- Audit of Inventory PDFDocument7 pagesAudit of Inventory PDFMae-shane SagayoNo ratings yet

- AFAR-02 Corporate LiquidationDocument2 pagesAFAR-02 Corporate LiquidationRamainne RonquilloNo ratings yet

- Chapter12 - AnswerDocument26 pagesChapter12 - AnswerAubreyNo ratings yet

- Intermediate Acctg A 1 10Document10 pagesIntermediate Acctg A 1 10Leonila RiveraNo ratings yet

- Applied Auditing Quiz #1 (Diagnostic Exam)Document15 pagesApplied Auditing Quiz #1 (Diagnostic Exam)xjammerNo ratings yet

- Ap-1403 ReceivablesDocument18 pagesAp-1403 Receivableschowchow123No ratings yet

- Audit of Inventory 2021 - ExamDocument9 pagesAudit of Inventory 2021 - ExammoreNo ratings yet

- Libyae Lustare - Audit Cash & Equivalents Under 40 CharactersDocument1 pageLibyae Lustare - Audit Cash & Equivalents Under 40 CharactersAna Mae HernandezNo ratings yet

- Internal Control Measures: Page 1 of 7Document7 pagesInternal Control Measures: Page 1 of 7Lucy HeartfiliaNo ratings yet

- Code of Ethics CPAR Manila ReviewerDocument14 pagesCode of Ethics CPAR Manila ReviewerJudith GabuteroNo ratings yet

- Unit 7 Audit of Property Plant and Equipment Handout Final t21516Document10 pagesUnit 7 Audit of Property Plant and Equipment Handout Final t21516Mikaella BengcoNo ratings yet

- Assignment 3.2 Inventory CutoffDocument3 pagesAssignment 3.2 Inventory CutoffHannah NolongNo ratings yet

- Karkits Corporation PDFDocument4 pagesKarkits Corporation PDFRachel LeachonNo ratings yet

- INTACC Reviewer Cash and EquivalentsDocument9 pagesINTACC Reviewer Cash and EquivalentsCzarhiena SantiagoNo ratings yet

- AP Lesson 2Document13 pagesAP Lesson 2Joanne RomaNo ratings yet

- Correction of ErrorsDocument4 pagesCorrection of ErrorsKris Van HalenNo ratings yet

- Substantive Tests of Receivables and SalesDocument5 pagesSubstantive Tests of Receivables and SalesEricaNo ratings yet

- Intercompany Plant Asset TransactionsDocument11 pagesIntercompany Plant Asset TransactionsRo-Anne LozadaNo ratings yet

- Cost Concepts, Classification and Segregation: M.S.M.CDocument7 pagesCost Concepts, Classification and Segregation: M.S.M.CAllen CarlNo ratings yet

- 94-Final PB-AUD - UnlockedDocument13 pages94-Final PB-AUD - UnlockedJessaNo ratings yet

- This Study Resource Was: Crc-Ace Review SchoolDocument7 pagesThis Study Resource Was: Crc-Ace Review SchoolLei Anne GatdulaNo ratings yet

- MQ 1 Receivables and InventoryDocument4 pagesMQ 1 Receivables and Inventorymarygraceomac100% (2)

- Home Office, Agency and Branch AccountingDocument17 pagesHome Office, Agency and Branch AccountingPaupauNo ratings yet

- Special TransactionsDocument5 pagesSpecial TransactionsJehannahBarat100% (1)

- Applied Auditing LeasesDocument2 pagesApplied Auditing Leasesshinebakayero hojillaNo ratings yet

- Department of Accountancy: Page - 1Document17 pagesDepartment of Accountancy: Page - 1NoroNo ratings yet

- SA1 Submissions: Standalone AssessmentDocument11 pagesSA1 Submissions: Standalone AssessmentYenNo ratings yet

- ProblemsDocument9 pagesProblemsMark Angelo AlvarezNo ratings yet

- Auditing Cup - 19 Rmyc Answer Key Final Round House StarkDocument13 pagesAuditing Cup - 19 Rmyc Answer Key Final Round House StarkCarl John PlacidoNo ratings yet

- Audit of PPE ExercisesDocument3 pagesAudit of PPE ExercisesMARCUAP Flora Mel Joy H.No ratings yet

- P1-01 Cash and Cash EquivalentsDocument5 pagesP1-01 Cash and Cash EquivalentsRachel LeachonNo ratings yet

- Assignment 3Document4 pagesAssignment 3Anna Mae NebresNo ratings yet

- Ap 59 PW - 5 06 PDFDocument18 pagesAp 59 PW - 5 06 PDFJasmin NgNo ratings yet

- Cebu Cpar Practical Accounting 1 InvestmentDocument11 pagesCebu Cpar Practical Accounting 1 InvestmentSky SoronoiNo ratings yet

- Ap-5905 Inventories PDFDocument9 pagesAp-5905 Inventories PDFKathleen Jane SolmayorNo ratings yet

- AP 5905 InventoriesDocument9 pagesAP 5905 Inventoriesxxxxxxxxx67% (3)

- Cpa Review School of The Philippines Manila Auditing Problems Audit of Inventories Problem No. 1Document11 pagesCpa Review School of The Philippines Manila Auditing Problems Audit of Inventories Problem No. 1Angelou100% (1)

- Substantive Testing For Inventories: Problem 1: The Makati Company Is On A Calendar Year Basis. The Following DataDocument17 pagesSubstantive Testing For Inventories: Problem 1: The Makati Company Is On A Calendar Year Basis. The Following DataPaul Anthony AspuriaNo ratings yet

- AUDIT PROBLEM INVENTORIES PART 1Document4 pagesAUDIT PROBLEM INVENTORIES PART 1Rio Cyrel CelleroNo ratings yet

- Activity in E3 - LiabilitiesDocument9 pagesActivity in E3 - LiabilitiesPaupau100% (1)

- Actvity 4 in Auditing 4 - Biological AssetsDocument3 pagesActvity 4 in Auditing 4 - Biological AssetsPaupauNo ratings yet

- Implement Strategy StructureDocument21 pagesImplement Strategy StructurePaupau100% (1)

- Activity - Derivatives and Hedging Accounting (PFRS 9)Document8 pagesActivity - Derivatives and Hedging Accounting (PFRS 9)PaupauNo ratings yet

- Activity - Translation of Foreign Currency Financial Statements (PAS 21 & PAS 29)Document1 pageActivity - Translation of Foreign Currency Financial Statements (PAS 21 & PAS 29)PaupauNo ratings yet

- Accounting for Cash, Receivables and InventoriesDocument12 pagesAccounting for Cash, Receivables and InventoriesPaupau100% (1)

- Assessment No. 6 MAS 06 Standard Costing Multiple Choice Problems: Choose The Letter of The Correct AnswerDocument12 pagesAssessment No. 6 MAS 06 Standard Costing Multiple Choice Problems: Choose The Letter of The Correct AnswerPaupauNo ratings yet

- Audit 4 - Audit in Specialized IndustryDocument7 pagesAudit 4 - Audit in Specialized IndustryPaupauNo ratings yet

- Assignment On PCF and Bank ReconDocument2 pagesAssignment On PCF and Bank ReconPaupauNo ratings yet

- Activity - Consolidated Financial Statement - Part 2 (1) (REVIEWER MIDTERM0Document6 pagesActivity - Consolidated Financial Statement - Part 2 (1) (REVIEWER MIDTERM0PaupauNo ratings yet

- AFAR ReviewDocument11 pagesAFAR ReviewPaupauNo ratings yet

- Activity - Consolidated Financial Statement, Part 1 (REVIEWER MIDTERM)Document12 pagesActivity - Consolidated Financial Statement, Part 1 (REVIEWER MIDTERM)Paupau0% (1)

- Activity On Application ControlDocument5 pagesActivity On Application ControlPaupauNo ratings yet

- Activity 2 Audit On CISDocument4 pagesActivity 2 Audit On CISPaupauNo ratings yet

- Special Purpose Audit Procedures and ReportsDocument6 pagesSpecial Purpose Audit Procedures and ReportsPaupauNo ratings yet

- Answer in Prelim Exam E4.Document12 pagesAnswer in Prelim Exam E4.PaupauNo ratings yet

- Activity - Home Office, Branch Accounting & Business Combination (REVIEWER MIDTERM)Document11 pagesActivity - Home Office, Branch Accounting & Business Combination (REVIEWER MIDTERM)Paupau100% (1)

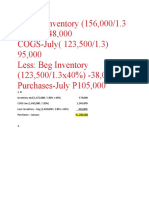

- Ending Inventory (156,000/1.3 x40%) P48,000 COGS-July (123,500/1.3) 95,000 Less: Beg Inventory (123,500/1.3x40%) - 38,000 Purchases-July P105,000Document1 pageEnding Inventory (156,000/1.3 x40%) P48,000 COGS-July (123,500/1.3) 95,000 Less: Beg Inventory (123,500/1.3x40%) - 38,000 Purchases-July P105,000PaupauNo ratings yet

- Activity 3 - CAATsDocument4 pagesActivity 3 - CAATsPaupauNo ratings yet

- Estimated transaction price methods and entries for consignment salesDocument7 pagesEstimated transaction price methods and entries for consignment salesPaupauNo ratings yet

- Answers - Partnership AccountingDocument14 pagesAnswers - Partnership AccountingPaupauNo ratings yet

- Actvity 4 in Auditing 4 - Biological AssetsDocument2 pagesActvity 4 in Auditing 4 - Biological AssetsPaupauNo ratings yet

- Home Office, Agency and Branch AccountingDocument17 pagesHome Office, Agency and Branch AccountingPaupauNo ratings yet

- Answer in Act. 2 For Cash-receivables-InventoriesDocument10 pagesAnswer in Act. 2 For Cash-receivables-InventoriesPaupauNo ratings yet

- MAS-04 Relevant CostingDocument10 pagesMAS-04 Relevant CostingPaupauNo ratings yet

- Management Accounting Techniques CompilationDocument40 pagesManagement Accounting Techniques CompilationGracelle Mae Oraller100% (1)

- 6 Business StrategyDocument27 pages6 Business StrategyPaupauNo ratings yet

- PAULA GOZUN - Activity 2 Accounting For Cash-receivables-InventoriesDocument9 pagesPAULA GOZUN - Activity 2 Accounting For Cash-receivables-InventoriesPaupauNo ratings yet

- Activity - Consolidated Financial Statement Part 1Document10 pagesActivity - Consolidated Financial Statement Part 1PaupauNo ratings yet

- Assessment No. 4 MAS-04 Relevant Costing I. Multiple Choice Theory: Choose The Letter of The Best AnswerDocument12 pagesAssessment No. 4 MAS-04 Relevant Costing I. Multiple Choice Theory: Choose The Letter of The Best AnswerPaupauNo ratings yet

- Statement of Cash Flow - Simple ExampleDocument5 pagesStatement of Cash Flow - Simple ExampleVinnie VermaNo ratings yet

- Tugas AKM 2 Proportional MetodeDocument3 pagesTugas AKM 2 Proportional MetodeSheny WulandariNo ratings yet

- Principles of Microeconomics 9Th Edition Sayre Test Bank Full Chapter PDFDocument67 pagesPrinciples of Microeconomics 9Th Edition Sayre Test Bank Full Chapter PDFphenicboxironicu9100% (9)

- True or False Costing QuizDocument5 pagesTrue or False Costing Quizretchiel love calinogNo ratings yet

- Auditing Theory MCQsDocument21 pagesAuditing Theory MCQsDawn Caldeira100% (1)

- Financial Management R. KitDocument241 pagesFinancial Management R. KitDamaris100% (1)

- Understand Cost-Volume-Profit (CVP) AnalysisDocument39 pagesUnderstand Cost-Volume-Profit (CVP) AnalysisVandana SharmaNo ratings yet

- Business Plan (Bigasan)Document10 pagesBusiness Plan (Bigasan)Harold Kent MendozaNo ratings yet

- Cost-Volume-Profit (CVP) Analysis Definition - InvestopediaDocument4 pagesCost-Volume-Profit (CVP) Analysis Definition - InvestopediaBob KaneNo ratings yet

- Calculating Gillette's Cost of CapitalDocument3 pagesCalculating Gillette's Cost of CapitalManvendra SinghNo ratings yet

- Working Capital MGMT Practice Manual PDFDocument75 pagesWorking Capital MGMT Practice Manual PDFPankaj PandeyNo ratings yet

- Mahusay Bsa-315major-Output-1Document3 pagesMahusay Bsa-315major-Output-1Jeth MahusayNo ratings yet

- Essays Sample Questions - Parts 1 & 2Document54 pagesEssays Sample Questions - Parts 1 & 2Krizia Almiranez100% (1)

- Accounting FundamentalsDocument37 pagesAccounting FundamentalsRuhen Rj PanchoNo ratings yet

- AccountingDocument72 pagesAccountingOmar SanadNo ratings yet

- Branch Accounting PDFDocument18 pagesBranch Accounting PDFSivasruthi DhandapaniNo ratings yet

- Statement of Changes in EquityDocument24 pagesStatement of Changes in EquityChristine SalvadorNo ratings yet

- Calcul Ating T He Co ST O F CapitalDocument50 pagesCalcul Ating T He Co ST O F CapitalSyrell NaborNo ratings yet

- Ghana University Business School MPhil MSc MBA Public Sector Accounting PracticeDocument6 pagesGhana University Business School MPhil MSc MBA Public Sector Accounting Practiceabigail acheampongNo ratings yet

- Capital Budgeting 01Document60 pagesCapital Budgeting 01Favian Maraville YadisaputraNo ratings yet

- Exercise 1-10: Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Fifth Canadian EditionDocument5 pagesExercise 1-10: Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Fifth Canadian EditionjorwitzNo ratings yet

- Calculate Break-Even Point Using Equation & Contribution Margin Methods (39Document11 pagesCalculate Break-Even Point Using Equation & Contribution Margin Methods (39Jayson TasarraNo ratings yet

- Print ExamDocument14 pagesPrint ExamkristinamanalangNo ratings yet

- 1-Finance For Non Finance - Training Material - 22 ND & 23rd Feb 2010Document89 pages1-Finance For Non Finance - Training Material - 22 ND & 23rd Feb 2010Raja RamNo ratings yet

- Exam in Accounting-FinalsDocument5 pagesExam in Accounting-FinalsIyarna YasraNo ratings yet

- Holygrail1 AflDocument23 pagesHolygrail1 AflSuresh AppstoreNo ratings yet

- Cost of Project: Smrity Paper Mills Private LimitedDocument17 pagesCost of Project: Smrity Paper Mills Private LimitedTripurari KumarNo ratings yet

- Accounting Basics: Inputs, Outputs and Financial StatementsDocument7 pagesAccounting Basics: Inputs, Outputs and Financial StatementsKiko Doragon Inoue TsubasaNo ratings yet

- Accounting 102 TermsDocument3 pagesAccounting 102 TermsAlfred MartinNo ratings yet

- ch08 SolDocument18 pagesch08 SolJohn Nigz Payee50% (2)