You might also like

- AP Macro WorkbookDocument346 pagesAP Macro WorkbookLynn Hollenbeck Breindel100% (5)

- Financial CrisisDocument53 pagesFinancial CrisisMehedi Hassan RanaNo ratings yet

- 1929-1946 Anjali The GREAT DREPERSSION.... !!!Document24 pages1929-1946 Anjali The GREAT DREPERSSION.... !!!ALOK YADAV100% (1)

- The Great Depression PDFDocument2 pagesThe Great Depression PDFSanthana Bharathi100% (1)

- S 26 Great Depression History - ArticleDocument5 pagesS 26 Great Depression History - ArticleTudor BizuNo ratings yet

- Great Depression 1920sDocument14 pagesGreat Depression 1920sPradeep GuptaNo ratings yet

- The Memoirs of Herbert Hoover - The Great Depression, 1929-1941From EverandThe Memoirs of Herbert Hoover - The Great Depression, 1929-1941No ratings yet

- The Great Depression: Saieesha RastogiDocument12 pagesThe Great Depression: Saieesha RastogiSaieesha RastogiNo ratings yet

- Great Depression Research PaperDocument7 pagesGreat Depression Research Paperdanielu1360% (5)

- Ldce - Fasp - 06 PDFDocument8 pagesLdce - Fasp - 06 PDFDinesh Talele100% (4)

- Depression Macroeconomic United States Unemployment Civil WarDocument7 pagesDepression Macroeconomic United States Unemployment Civil WarRiddhiNo ratings yet

- Chapter 10, Question 1. ADocument25 pagesChapter 10, Question 1. AAnh ThưNo ratings yet

- Chapter 4 International Trade TheoryDocument40 pagesChapter 4 International Trade TheoryAtiqul IslamNo ratings yet

- Understanding the Great Depression and Failures of Modern Economic Policy: The Story of the Heedless GiantFrom EverandUnderstanding the Great Depression and Failures of Modern Economic Policy: The Story of the Heedless GiantNo ratings yet

- Customer Service Case StudiesDocument4 pagesCustomer Service Case Studiessameer maddubaigari80% (5)

- The Great Depression: A Look at The Events and Circumstances That Led to One of The Most Devastating Downturns in The Economic HistoryFrom EverandThe Great Depression: A Look at The Events and Circumstances That Led to One of The Most Devastating Downturns in The Economic HistoryNo ratings yet

- Great DepressionDocument16 pagesGreat DepressionKamalesh KumarNo ratings yet

- The Great DepressionDocument59 pagesThe Great DepressionShambhavi TewariNo ratings yet

- Great DepressionDocument5 pagesGreat DepressionZarmina NaseerNo ratings yet

- Great DepressionDocument13 pagesGreat DepressionJefferson Alzate CabobosNo ratings yet

- Great Depression Era: What Is Great Depression Era? Date: August 1929-1939Document3 pagesGreat Depression Era: What Is Great Depression Era? Date: August 1929-1939Raffay NaveedNo ratings yet

- Intrade References1Document15 pagesIntrade References1claraNo ratings yet

- Fiscal and Monetary Policy Before Great Depression, During Depression, After Depression and There EffectivenessDocument10 pagesFiscal and Monetary Policy Before Great Depression, During Depression, After Depression and There EffectivenessRajan shahNo ratings yet

- Eco 2 Infographic XXDocument6 pagesEco 2 Infographic XXBrian JavierNo ratings yet

- The Event Analysis of Great DepressionDocument12 pagesThe Event Analysis of Great DepressionZia UlhaqNo ratings yet

- The Great DepresionDocument4 pagesThe Great Depresionangela.za.esNo ratings yet

- The Great Depression: Study: Assignment No: Date: TeacherDocument4 pagesThe Great Depression: Study: Assignment No: Date: TeacherAhmed Ullah ShahNo ratings yet

- Case Study Financial CrisisDocument6 pagesCase Study Financial CrisisNicoleParedesNo ratings yet

- FinanceDocument2 pagesFinanceSid TuazonNo ratings yet

- 1930s Great DepressionDocument1 page1930s Great DepressionMinahil NoorNo ratings yet

- Cycles of Depressions: MacroeconomicsDocument18 pagesCycles of Depressions: MacroeconomicsCozma Alina DanielaNo ratings yet

- The Great Depression - Part1Document39 pagesThe Great Depression - Part1philipsNo ratings yet

- The Great DepressionDocument4 pagesThe Great Depressionapi-283823164No ratings yet

- The Great DepressionDocument25 pagesThe Great Depressionshunno kabirNo ratings yet

- Great Depression: Economic IndicatorsDocument4 pagesGreat Depression: Economic IndicatorsNikki ElejordeNo ratings yet

- THE Great Depression: Submitted By: Utkarsh Garg 2K16/ME/183 OPQ BatchDocument6 pagesTHE Great Depression: Submitted By: Utkarsh Garg 2K16/ME/183 OPQ BatchUtkarsh GargNo ratings yet

- TheGreatDepression 1Document3 pagesTheGreatDepression 1OmenApxNo ratings yet

- Great DepressionDocument34 pagesGreat DepressionUyen NgoNo ratings yet

- The Great DepressionDocument5 pagesThe Great Depressionkipkoech.cheruiyotNo ratings yet

- Final Paper MacroDocument9 pagesFinal Paper Macroapi-537730890No ratings yet

- Cycles of Depressions: MacroeconomicsDocument17 pagesCycles of Depressions: MacroeconomicsCozma Alina DanielaNo ratings yet

- Objectives For Chapter 12: The Great Depression (1929 To 1941) and The Beginning of Keynesian EconomicsDocument11 pagesObjectives For Chapter 12: The Great Depression (1929 To 1941) and The Beginning of Keynesian EconomicsSaieesha RastogiNo ratings yet

- The Great DepressionDocument7 pagesThe Great DepressionBhavya ShahNo ratings yet

- The Great DepressionDocument8 pagesThe Great Depressioniftikhar ahmedNo ratings yet

- The Great DepressionDocument1 pageThe Great DepressionEric RentschlerNo ratings yet

- Great DepressionDocument26 pagesGreat Depressionjosejosef630No ratings yet

- Great DepressionDocument2 pagesGreat Depressionmister almondNo ratings yet

- AODfallsDocument4 pagesAODfallsDeep MandaliaNo ratings yet

- International BankingDocument36 pagesInternational Bankingngochailuong7274No ratings yet

- Great DepressionDocument4 pagesGreat Depressionngla.alexNo ratings yet

- Great Depression: The Scope and Trajectory of The Great DepressionDocument7 pagesGreat Depression: The Scope and Trajectory of The Great DepressionAlly MangineNo ratings yet

- Great Depression - WikipediaDocument317 pagesGreat Depression - WikipediabrajpaljawlaNo ratings yet

- Study Guide For Great DepressionDocument4 pagesStudy Guide For Great DepressionKyle Panek-KravitzNo ratings yet

- Great Depression Research Paper by Marcus DiorDocument7 pagesGreat Depression Research Paper by Marcus DiorRegular Ol'MärcusNo ratings yet

- Guggenheim PartnersDocument10 pagesGuggenheim PartnersSFinancialNo ratings yet

- Great Depression Teacher-Expert AssignmentDocument22 pagesGreat Depression Teacher-Expert Assignmentisha56621No ratings yet

- Final ProjectDocument6 pagesFinal Projectlauren roNo ratings yet

- Baliddawa 1Document10 pagesBaliddawa 1rinaNo ratings yet

- Joseph Lazzaro - Did New Deal End DepressionDocument2 pagesJoseph Lazzaro - Did New Deal End DepressionAgustín PineauNo ratings yet

- Lecture Morys Great DepressionDocument17 pagesLecture Morys Great DepressionAntonio AguiarNo ratings yet

- Macroeconomics Assignment: "Great Depression"Document6 pagesMacroeconomics Assignment: "Great Depression"Kriti SahoreNo ratings yet

- H1.1-The Great DepressionDocument5 pagesH1.1-The Great Depressioniwhitetower11No ratings yet

- DOW 30,000: The Coming Stock CRASH AND HOUSING PRICE COLLAPSEFrom EverandDOW 30,000: The Coming Stock CRASH AND HOUSING PRICE COLLAPSERating: 5 out of 5 stars5/5 (1)

- Pricing A Collateralized Derivative Trade With A FDocument26 pagesPricing A Collateralized Derivative Trade With A FAtul NaharNo ratings yet

- CSG Ar 2009 enDocument496 pagesCSG Ar 2009 enAtul NaharNo ratings yet

- CSG Ar 2008 enDocument444 pagesCSG Ar 2008 enAtul NaharNo ratings yet

- CSG Ar 2007 enDocument396 pagesCSG Ar 2007 enAtul NaharNo ratings yet

- IMA Pre-Readiness ChecklistDocument9 pagesIMA Pre-Readiness ChecklistAtul NaharNo ratings yet

- Approved Supplier of IFR For IOCL Vijayawada Tender.Document2 pagesApproved Supplier of IFR For IOCL Vijayawada Tender.rohitNo ratings yet

- Exchange Rate, Inflation and Interest Rates Relationships: Anautoregressive Distributed Lag AnalysisDocument17 pagesExchange Rate, Inflation and Interest Rates Relationships: Anautoregressive Distributed Lag AnalysisFeranmi OladigboNo ratings yet

- The Role of Monetary PolicyDocument2 pagesThe Role of Monetary PolicyHân NgọcNo ratings yet

- Case Processing SummaryDocument2 pagesCase Processing SummaryEka MuallimahNo ratings yet

- Economics 2142 Time Series Analysis SyllabusDocument14 pagesEconomics 2142 Time Series Analysis SyllabusGabriel RoblesNo ratings yet

- Bahrain ChemicalDocument4 pagesBahrain Chemicallokesh LokiNo ratings yet

- GHMC Property Tax PDFDocument1 pageGHMC Property Tax PDFSrinubabu MaddukuriNo ratings yet

- Managerial Economics: Applications, Strategy, and Tactics, 12 EditionDocument24 pagesManagerial Economics: Applications, Strategy, and Tactics, 12 EditionWilliam DC RiveraNo ratings yet

- GroupActivity1 EntrepDocument5 pagesGroupActivity1 Entrepyannie isananNo ratings yet

- SPF 2000 Bill FormsDocument17 pagesSPF 2000 Bill Formskarunamoorthi_p220957% (7)

- Excel Problem Set 2 FIN 5203 SP21 PDFDocument3 pagesExcel Problem Set 2 FIN 5203 SP21 PDFAhmed MahmoudNo ratings yet

- NS ES 0048 Steam Generator - ALLDocument2 pagesNS ES 0048 Steam Generator - ALLbartney chenNo ratings yet

- Adobe Scan 02-Jul-2022Document4 pagesAdobe Scan 02-Jul-2022Akshita SethiNo ratings yet

- Dongyang 1926 Parts Catalog Watermark 150625104921 Lva1 App 6891Document10 pagesDongyang 1926 Parts Catalog Watermark 150625104921 Lva1 App 6891shirley100% (46)

- HTM 220 Assignment #4Document2 pagesHTM 220 Assignment #4Annie ChoiNo ratings yet

- Chemistry 1 Tutor - Vol 2 - Worksheet 10 - Limiting Reactants - Part 1Document12 pagesChemistry 1 Tutor - Vol 2 - Worksheet 10 - Limiting Reactants - Part 1lightningpj1234No ratings yet

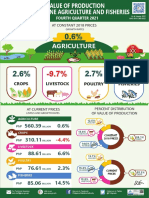

- Infographics, Value of Production in Philippine Agriculture and Fisheries, Fourth Quarter 2021Document1 pageInfographics, Value of Production in Philippine Agriculture and Fisheries, Fourth Quarter 2021Cart LaneNo ratings yet

- Summary For The Preparation of Bank Reconciliation StatementDocument5 pagesSummary For The Preparation of Bank Reconciliation StatementGhalib HussainNo ratings yet

- Detailed Advertisement English Nov22Document6 pagesDetailed Advertisement English Nov22VijayNo ratings yet

- A Case Study of TanzaniaDocument15 pagesA Case Study of TanzaniaVladGrigoreNo ratings yet

- Cost AccountingDocument7 pagesCost AccountingShubhamNo ratings yet

- VISUALS IN ECONOMICS (Deped)Document4 pagesVISUALS IN ECONOMICS (Deped)Ceres B. LuzarragaNo ratings yet

- Upstate Gold Sheet - Dynamic Pricing PDFDocument1 pageUpstate Gold Sheet - Dynamic Pricing PDFtwrdaveNo ratings yet

- Module 4 - DepreciationDocument70 pagesModule 4 - DepreciationGaurav ShekharNo ratings yet

- Utex Plunger PackingDocument7 pagesUtex Plunger Packinganandkumar.mauryaNo ratings yet