You might also like

- ProjectDocument8 pagesProjectSharan SharanNo ratings yet

- Myanmar Telecommunications Sector: (Summary)Document9 pagesMyanmar Telecommunications Sector: (Summary)Jahedul Abedin SohelNo ratings yet

- POTRAZ Q4 2020 Report Highlights Growth in Internet & Mobile SubscriptionsDocument23 pagesPOTRAZ Q4 2020 Report Highlights Growth in Internet & Mobile SubscriptionsJacob PossibilityNo ratings yet

- Operation Management: PGBM03Document11 pagesOperation Management: PGBM03Amal HameedNo ratings yet

- FMI Briefing Final1Document36 pagesFMI Briefing Final1PetrNo ratings yet

- Estimating Interconnection Cost in Mobile Phone Market in TunisiaDocument12 pagesEstimating Interconnection Cost in Mobile Phone Market in TunisiaSamir GhoualiNo ratings yet

- Sector Performance 1stQ2020Document21 pagesSector Performance 1stQ2020Joseph MutitiNo ratings yet

- Indian Telecom-Price WarDocument12 pagesIndian Telecom-Price WarmaheshwariheenaNo ratings yet

- CAK Sector-Statistics-Report-Q2-2019-2020 (Oct - Dec 2019) PDFDocument24 pagesCAK Sector-Statistics-Report-Q2-2019-2020 (Oct - Dec 2019) PDFgeraldmrkNo ratings yet

- Publications 1822020000 EN Quarterly Bulletin September 2019 2020Document12 pagesPublications 1822020000 EN Quarterly Bulletin September 2019 2020محمد فتحى علىNo ratings yet

- Maroc Telecom KPI-Q12022Document9 pagesMaroc Telecom KPI-Q12022Youssef JaafarNo ratings yet

- Telecom Sector ReportDocument21 pagesTelecom Sector ReportMohammed SaadiNo ratings yet

- Quarter 2 Communications Statistics - Revised Final (1) - 1677145396Document40 pagesQuarter 2 Communications Statistics - Revised Final (1) - 1677145396DaveNo ratings yet

- Sescom Info Solutions FzeDocument14 pagesSescom Info Solutions FzeSESCOM INFO SOLUTIONS FZENo ratings yet

- Mobile Churn Trends and Customer Retention StrategiesDocument17 pagesMobile Churn Trends and Customer Retention StrategiesAydin KaraerNo ratings yet

- ITU Regional Workshop on Mobile Roaming: NTC Role and ChallengesDocument18 pagesITU Regional Workshop on Mobile Roaming: NTC Role and ChallengesALAANo ratings yet

- SCFS23 Day 1 - Full Day SlidesDocument39 pagesSCFS23 Day 1 - Full Day SlidesJoaquin DuranyNo ratings yet

- (Potraz) : Postal and Telecommunications Regulatory Authority of ZimbabweDocument25 pages(Potraz) : Postal and Telecommunications Regulatory Authority of ZimbabweJoseph MutitiNo ratings yet

- Corporate Presentation: January 2022Document67 pagesCorporate Presentation: January 2022vishwas pandithNo ratings yet

- Pocket MF Andoid Applicaion For Microfinance: Chathuranga RathnayakeDocument14 pagesPocket MF Andoid Applicaion For Microfinance: Chathuranga RathnayakeChathuranga RathnayakeNo ratings yet

- Top 10 stockbroking companies analysisDocument20 pagesTop 10 stockbroking companies analysisShilpi KumariNo ratings yet

- POTRAZ 1st - Quarter 2017 PDFDocument19 pagesPOTRAZ 1st - Quarter 2017 PDFJotham NyamandeNo ratings yet

- Addressing The Challenges of Industrialization: Responsible Mining: Moving Beyond ComplianceDocument20 pagesAddressing The Challenges of Industrialization: Responsible Mining: Moving Beyond Compliancemonkeybike88No ratings yet

- Sms ProjectDocument10 pagesSms Projectrisongkishore8841No ratings yet

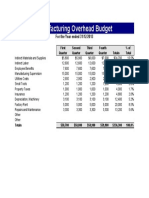

- Manufacturing OVHDocument1 pageManufacturing OVHMichael HakimNo ratings yet

- 2023 ADB Asia SME Monitor - PhilippinesDocument15 pages2023 ADB Asia SME Monitor - PhilippinesCyrishNo ratings yet

- Office For National Statistics (ONS)Document8 pagesOffice For National Statistics (ONS)Carmen PireddaNo ratings yet

- Maroc Telecom KPI FY2021Document9 pagesMaroc Telecom KPI FY2021Youssef JaafarNo ratings yet

- TABLE 2 - Employed Persons by Sector, Subsector, and Hours Worked, with Measures of Precision, PhilippinesDocument1 pageTABLE 2 - Employed Persons by Sector, Subsector, and Hours Worked, with Measures of Precision, PhilippinescotiadanielNo ratings yet

- Group4 Project2-2Document19 pagesGroup4 Project2-2John Brian Asi AlmazanNo ratings yet

- Telecom Industry in IndiaDocument35 pagesTelecom Industry in IndiaGovind ChandvaniNo ratings yet

- Easypaisa-All Pricing and CommissioningDocument17 pagesEasypaisa-All Pricing and Commissioningqaisar_murtaza50% (4)

- 7696 27254 1 PBDocument25 pages7696 27254 1 PBAsnake MekonnenNo ratings yet

- Market Structure Analysis EcoDocument9 pagesMarket Structure Analysis EcoPalak MendirattaNo ratings yet

- AT&T vs Verizon Case StudyDocument9 pagesAT&T vs Verizon Case Studyroyal lathNo ratings yet

- Mobilink Pakistan Market Leader Telecom SubsidiaryDocument36 pagesMobilink Pakistan Market Leader Telecom SubsidiaryArslan JamaliNo ratings yet

- MOBILINK Management Term ReportDocument36 pagesMOBILINK Management Term ReportArslan JamaliNo ratings yet

- Telecom Regulatory Authority of India Performance Report Q3 2011Document445 pagesTelecom Regulatory Authority of India Performance Report Q3 2011ruhiaroraNo ratings yet

- Vodafone Egypt Strategic StudyDocument36 pagesVodafone Egypt Strategic StudyAhmed EssamNo ratings yet

- Telecomarticle Dec13Document10 pagesTelecomarticle Dec13Pranav NaikNo ratings yet

- The Future of Mobility Is at Our DoorstepDocument121 pagesThe Future of Mobility Is at Our DoorstepJosh HuangNo ratings yet

- Portfolio Analysis - June 2019-MuleDocument6 pagesPortfolio Analysis - June 2019-MulemartagobanaNo ratings yet

- Amit Gebreigzihaber TransportationDocument10 pagesAmit Gebreigzihaber TransportationgemechuNo ratings yet

- Full Report 1Document10 pagesFull Report 1Kajune ChithilaphaNo ratings yet

- IndigoDocument63 pagesIndigoHarshit JainNo ratings yet

- EN EN: European CommissionDocument19 pagesEN EN: European CommissionaNo ratings yet

- Mobile Advertising 4 - Ghassan Hasbani - STCDocument16 pagesMobile Advertising 4 - Ghassan Hasbani - STCsebax123No ratings yet

- Accenture-Unlocking-Digital-Value-South Africa-Telecoms-Sector PDFDocument26 pagesAccenture-Unlocking-Digital-Value-South Africa-Telecoms-Sector PDFadityaNo ratings yet

- Telecom Industry Final ProjectDocument3 pagesTelecom Industry Final ProjectShashi SuryaNo ratings yet

- Investor Fact Sheet q3 Fy23Document16 pagesInvestor Fact Sheet q3 Fy23Anshul SainiNo ratings yet

- VoLTE End To End Architecture (MPI0124-000-010)Document32 pagesVoLTE End To End Architecture (MPI0124-000-010)Zach balmar100% (1)

- Consumer Behaviour in Selecting Mobile PhonesDocument24 pagesConsumer Behaviour in Selecting Mobile PhonesPriyank_Vishar_470No ratings yet

- SK Telecom Announces 2010 ResultsDocument11 pagesSK Telecom Announces 2010 ResultsmaximebayenNo ratings yet

- M - S R K EnterprisesDocument23 pagesM - S R K EnterprisesArun PrasadNo ratings yet

- POTRAZ 3rd - Quarter - 2017 PDFDocument24 pagesPOTRAZ 3rd - Quarter - 2017 PDFJotham NyamandeNo ratings yet

- Mobile Cellular Policy: IT and Telecommunication DivisionDocument23 pagesMobile Cellular Policy: IT and Telecommunication DivisionZahid KhanNo ratings yet

- Anc300 Jangad Contaoe Valdez Lopez SibagDocument18 pagesAnc300 Jangad Contaoe Valdez Lopez SibagElla Mae ContaoeNo ratings yet

- Strategic Management Group AssignmentDocument15 pagesStrategic Management Group Assignmentabhishek guptaNo ratings yet

- Nagarro's Work From Anywhere FutureDocument159 pagesNagarro's Work From Anywhere Futureomar cortezNo ratings yet

- Factors Influencing Internet Banking Adoption in ZimbabweDocument10 pagesFactors Influencing Internet Banking Adoption in ZimbabweTANATSWA RON CHINENERENo ratings yet

- Sector Perfomance 4th Quarter 2013Document18 pagesSector Perfomance 4th Quarter 2013TANATSWA RON CHINENERENo ratings yet

- Privacy Concerns for Internet Cafe Users in ZimbabweDocument17 pagesPrivacy Concerns for Internet Cafe Users in ZimbabweTANATSWA RON CHINENERENo ratings yet

- Privacy Concerns for Internet Cafe Users in ZimbabweDocument17 pagesPrivacy Concerns for Internet Cafe Users in ZimbabweTANATSWA RON CHINENERENo ratings yet

- Finscope Consumer Survey Zimbabwe 2011: Maya Makanjee, Finmark Trust Grown M. Chirongwe, Zimstat HarareDocument52 pagesFinscope Consumer Survey Zimbabwe 2011: Maya Makanjee, Finmark Trust Grown M. Chirongwe, Zimstat HarareTANATSWA RON CHINENERENo ratings yet

- Sony STR d615Document41 pagesSony STR d615zlrigNo ratings yet

- SNUGSingaporeDocument27 pagesSNUGSingaporeYashwanthKumarNo ratings yet

- SEUIC CRUISE 1 (P) Product Introduction 2019 V2.3Document36 pagesSEUIC CRUISE 1 (P) Product Introduction 2019 V2.3Malm n FeelNo ratings yet

- Irfr120, Irfu120: 8.4A, 100V, 0.270 Ohm, N-Channel Power Mosfets FeaturesDocument7 pagesIrfr120, Irfu120: 8.4A, 100V, 0.270 Ohm, N-Channel Power Mosfets FeaturesWahyu DiyonoNo ratings yet

- One step solution for LCD / PDP / OLED panel application: Datasheet, inventory and accessoryDocument29 pagesOne step solution for LCD / PDP / OLED panel application: Datasheet, inventory and accessoryjaluadiNo ratings yet

- Internet of Things in Industries: A Survey: Li Da Xu, Senior Member, IEEE, Wu He, and Shancang LiDocument11 pagesInternet of Things in Industries: A Survey: Li Da Xu, Senior Member, IEEE, Wu He, and Shancang LiAshutosh PandeyNo ratings yet

- Internet of Things Professional Elective Course - IvDocument2 pagesInternet of Things Professional Elective Course - IvShivakumar pNo ratings yet

- Nrscgfreqconfig - Scgdlarfcn and Nrscgfreqconfig - Scgdlarfcnpriority Parameters Specify The Arfcn and PriorityDocument5 pagesNrscgfreqconfig - Scgdlarfcn and Nrscgfreqconfig - Scgdlarfcnpriority Parameters Specify The Arfcn and PriorityCesarNunesNo ratings yet

- Sip Config Guide Cisco Unified CmeDocument18 pagesSip Config Guide Cisco Unified Cmeharri06665No ratings yet

- AYON-prijslijst-4Document14 pagesAYON-prijslijst-4aleks canjugaNo ratings yet

- MCQ On Network TopologyDocument2 pagesMCQ On Network TopologyLittle princeNo ratings yet

- Home Modem - Internet - Installation - Guide - CGN-RESDocument8 pagesHome Modem - Internet - Installation - Guide - CGN-RESAnthony HansonNo ratings yet

- Behrouz A Forouzan.: Downloaded From Downloaded FromDocument15 pagesBehrouz A Forouzan.: Downloaded From Downloaded FromShyam DharanNo ratings yet

- Cambridge IGCSE™: Information and Communication Technology 0417/11 October/November 2020Document9 pagesCambridge IGCSE™: Information and Communication Technology 0417/11 October/November 2020osmanfut1No ratings yet

- Training Report: Indian RailwayDocument38 pagesTraining Report: Indian RailwayAyush Maheshwari83% (12)

- Medusa 4 TS 09 033Document2 pagesMedusa 4 TS 09 033doantran2508No ratings yet

- Ivan Pavlović English CVDocument3 pagesIvan Pavlović English CVMarina Masnić-PetrovićNo ratings yet

- Poptronics 1974 12 PDFDocument108 pagesPoptronics 1974 12 PDFAhmet KarabeyNo ratings yet

- Ipc Hdbw4231e As s4Document3 pagesIpc Hdbw4231e As s4EBIE ATANGANANo ratings yet

- Pag QSL Net Chap6-3Document23 pagesPag QSL Net Chap6-3Arturo FuentesNo ratings yet

- Ericsson Mini-Link EquipmentDocument3 pagesEricsson Mini-Link EquipmentJaime Garcia De ParedesNo ratings yet

- (Question Bank) : Dr. Harjinder SinghDocument12 pages(Question Bank) : Dr. Harjinder SinghSanjay DuttNo ratings yet

- DS-D5186RB - A - Android 11Document5 pagesDS-D5186RB - A - Android 11Gopal Chandra SamantaNo ratings yet

- Memory CompilersDocument58 pagesMemory CompilersSnehaNo ratings yet

- Uitf Offsite Exam Reminders.Document29 pagesUitf Offsite Exam Reminders.reagan blaireNo ratings yet

- Edexcel 2022 - JuneDocument24 pagesEdexcel 2022 - JuneDix BrosNo ratings yet

- EE8591 DSP Unit 1 Notes FinalDocument81 pagesEE8591 DSP Unit 1 Notes Final5047- MUTHINENI AGNIVESHNo ratings yet

- Bryston's Powerful and Flexible PowerPac AmplifiersDocument11 pagesBryston's Powerful and Flexible PowerPac AmplifiersElkin BabiloniaNo ratings yet

- AxiDocument12 pagesAxiganapathiNo ratings yet

- Branding: What You Need to Know About Building a Personal Brand and Growing Your Small Business Using Social Media Marketing and Offline Guerrilla TacticsFrom EverandBranding: What You Need to Know About Building a Personal Brand and Growing Your Small Business Using Social Media Marketing and Offline Guerrilla TacticsRating: 5 out of 5 stars5/5 (32)

- Defensive Cyber Mastery: Expert Strategies for Unbeatable Personal and Business SecurityFrom EverandDefensive Cyber Mastery: Expert Strategies for Unbeatable Personal and Business SecurityRating: 5 out of 5 stars5/5 (1)

- The Internet Con: How to Seize the Means of ComputationFrom EverandThe Internet Con: How to Seize the Means of ComputationRating: 5 out of 5 stars5/5 (6)

- The Wires of War: Technology and the Global Struggle for PowerFrom EverandThe Wires of War: Technology and the Global Struggle for PowerRating: 4 out of 5 stars4/5 (34)

- TikTok Algorithms 2024 $15,000/Month Guide To Escape Your Job And Build an Successful Social Media Marketing Business From Home Using Your Personal Account, Branding, SEO, InfluencerFrom EverandTikTok Algorithms 2024 $15,000/Month Guide To Escape Your Job And Build an Successful Social Media Marketing Business From Home Using Your Personal Account, Branding, SEO, InfluencerRating: 4 out of 5 stars4/5 (4)

- Python for Beginners: The 1 Day Crash Course For Python Programming In The Real WorldFrom EverandPython for Beginners: The 1 Day Crash Course For Python Programming In The Real WorldNo ratings yet

- Social Media Marketing 2024, 2025: Build Your Business, Skyrocket in Passive Income, Stop Working a 9-5 Lifestyle, True Online Working from HomeFrom EverandSocial Media Marketing 2024, 2025: Build Your Business, Skyrocket in Passive Income, Stop Working a 9-5 Lifestyle, True Online Working from HomeNo ratings yet

- How to Do Nothing: Resisting the Attention EconomyFrom EverandHow to Do Nothing: Resisting the Attention EconomyRating: 4 out of 5 stars4/5 (421)

- The Digital Marketing Handbook: A Step-By-Step Guide to Creating Websites That SellFrom EverandThe Digital Marketing Handbook: A Step-By-Step Guide to Creating Websites That SellRating: 5 out of 5 stars5/5 (6)

- Facing Cyber Threats Head On: Protecting Yourself and Your BusinessFrom EverandFacing Cyber Threats Head On: Protecting Yourself and Your BusinessRating: 4.5 out of 5 stars4.5/5 (27)

- Content Rules: How to Create Killer Blogs, Podcasts, Videos, Ebooks, Webinars (and More) That Engage Customers and Ignite Your BusinessFrom EverandContent Rules: How to Create Killer Blogs, Podcasts, Videos, Ebooks, Webinars (and More) That Engage Customers and Ignite Your BusinessRating: 4.5 out of 5 stars4.5/5 (42)

- The $1,000,000 Web Designer Guide: A Practical Guide for Wealth and Freedom as an Online FreelancerFrom EverandThe $1,000,000 Web Designer Guide: A Practical Guide for Wealth and Freedom as an Online FreelancerRating: 4.5 out of 5 stars4.5/5 (22)

- HTML, CSS, and JavaScript Mobile Development For DummiesFrom EverandHTML, CSS, and JavaScript Mobile Development For DummiesRating: 4 out of 5 stars4/5 (10)

- More Porn - Faster!: 50 Tips & Tools for Faster and More Efficient Porn BrowsingFrom EverandMore Porn - Faster!: 50 Tips & Tools for Faster and More Efficient Porn BrowsingRating: 3.5 out of 5 stars3.5/5 (23)

- The Designer’s Guide to Figma: Master Prototyping, Collaboration, Handoff, and WorkflowFrom EverandThe Designer’s Guide to Figma: Master Prototyping, Collaboration, Handoff, and WorkflowNo ratings yet

- A Great Online Dating Profile: 30 Tips to Get Noticed and Get More ResponsesFrom EverandA Great Online Dating Profile: 30 Tips to Get Noticed and Get More ResponsesRating: 3.5 out of 5 stars3.5/5 (2)

- Monitored: Business and Surveillance in a Time of Big DataFrom EverandMonitored: Business and Surveillance in a Time of Big DataRating: 4 out of 5 stars4/5 (1)

- An Ultimate Guide to Kali Linux for BeginnersFrom EverandAn Ultimate Guide to Kali Linux for BeginnersRating: 3.5 out of 5 stars3.5/5 (4)

- So You Want to Start a Podcast: Finding Your Voice, Telling Your Story, and Building a Community that Will ListenFrom EverandSo You Want to Start a Podcast: Finding Your Voice, Telling Your Story, and Building a Community that Will ListenRating: 4.5 out of 5 stars4.5/5 (35)