0% found this document useful (0 votes)

117 views3 pagesConsolidated Financial Statements Analysis

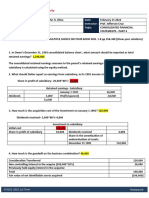

The document is a student's homework on consolidated financial statements that involves solving a multi-step problem. The student analyzed the effects of an acquisition by Day Co. of Night Co., where Day acquired 75% of Night. The summary calculates goodwill, non-controlling interest, consolidated retained earnings and profit. It also provides a consolidated balance sheet and income statement combining Day and Night.

Uploaded by

Imthe OneCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

117 views3 pagesConsolidated Financial Statements Analysis

The document is a student's homework on consolidated financial statements that involves solving a multi-step problem. The student analyzed the effects of an acquisition by Day Co. of Night Co., where Day acquired 75% of Night. The summary calculates goodwill, non-controlling interest, consolidated retained earnings and profit. It also provides a consolidated balance sheet and income statement combining Day and Night.

Uploaded by

Imthe OneCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd