You might also like

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Advanced Financial Accounting: AssetsDocument9 pagesAdvanced Financial Accounting: AssetsPrabavathi KarunanithiNo ratings yet

- Hong Fok Corporation Limited: Revenue (Note 1)Document8 pagesHong Fok Corporation Limited: Revenue (Note 1)Theng RogerNo ratings yet

- ANSWERDocument9 pagesANSWERLeesaa88No ratings yet

- Advanced Financial Accounting: AssetsDocument2 pagesAdvanced Financial Accounting: AssetsPrabavathi KarunanithiNo ratings yet

- Workings Rs.000Document1 pageWorkings Rs.000.No ratings yet

- Workings Rs.000Document1 pageWorkings Rs.000.No ratings yet

- 2021 Seminar Paper Marking SchemeDocument12 pages2021 Seminar Paper Marking Schemesayuru423geenethNo ratings yet

- Mangerial Remuneration Final!Document4 pagesMangerial Remuneration Final!Yash RajNo ratings yet

- Chapter 5 Complex Group StructuresDocument12 pagesChapter 5 Complex Group StructuresKE XIN NGNo ratings yet

- Tutorial 12 Performance MeasurementDocument4 pagesTutorial 12 Performance MeasurementEsther LuehNo ratings yet

- C 20: C C F: Hapter Onsolidation ASH LowsDocument1 pageC 20: C C F: Hapter Onsolidation ASH Lows.No ratings yet

- CFAP 1 Summer 2023Document7 pagesCFAP 1 Summer 2023Ali MohammadNo ratings yet

- CSOCF Acquisition Both Methods Malim Nawar BHDDocument7 pagesCSOCF Acquisition Both Methods Malim Nawar BHDSyafahani SafieNo ratings yet

- 20solution Far460 - Jun 2020 - StudentDocument10 pages20solution Far460 - Jun 2020 - StudentRuzaikha razaliNo ratings yet

- Facn311 Test 1 Solution 2019Document10 pagesFacn311 Test 1 Solution 20196lackzamokuhleNo ratings yet

- Balgownie LTD Solution 2021 - V2Document12 pagesBalgownie LTD Solution 2021 - V2Ludmila DorojanNo ratings yet

- Annual Report of Reliance General Insurance On 10-11Document49 pagesAnnual Report of Reliance General Insurance On 10-11bhagathnagarNo ratings yet

- Reliance General Insurance Company Limited: Disclosures - Non-Life Insurance CompaniesDocument48 pagesReliance General Insurance Company Limited: Disclosures - Non-Life Insurance CompaniesNeha A BirajdarNo ratings yet

- Paragon SPL & SFP With AnswerDocument3 pagesParagon SPL & SFP With Answerramyaa baluNo ratings yet

- Ans Mini Case 2 - A171 - LecturerDocument14 pagesAns Mini Case 2 - A171 - LecturerXue Yin Lew100% (1)

- Examination Paper: Ba Accounting & Finance Level Five Financial Accounting 5AG006 (RESIT)Document8 pagesExamination Paper: Ba Accounting & Finance Level Five Financial Accounting 5AG006 (RESIT)Boago PhatshwaneNo ratings yet

- SSGC Final UpdateDocument212 pagesSSGC Final Updateemzeday100% (1)

- Comparative FSDocument4 pagesComparative FSSuper GenerationNo ratings yet

- Mid Term Solution 2021Document5 pagesMid Term Solution 2021Ayush SrivastavaNo ratings yet

- Close LTDDocument5 pagesClose LTDXianFa WongNo ratings yet

- Stanley Gibbons Group PLCDocument2 pagesStanley Gibbons Group PLCImran WarsiNo ratings yet

- ABC Cement FM (Final)Document24 pagesABC Cement FM (Final)Muhammad Ismail (Father Name:Abdul Rahman)No ratings yet

- Enterprise Group PLC: Unaudited Financial Statements For The Year Ended 31 December 2021Document8 pagesEnterprise Group PLC: Unaudited Financial Statements For The Year Ended 31 December 2021Fuaad DodooNo ratings yet

- Tutorial Questions - Trimester - 2210.Document26 pagesTutorial Questions - Trimester - 2210.premsuwaatiiNo ratings yet

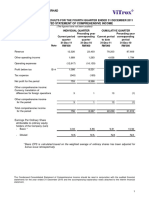

- Vitrox q42011Document10 pagesVitrox q42011Dennis AngNo ratings yet

- 10a Limited Company RevisionDocument3 pages10a Limited Company RevisionJoseph IbrahimNo ratings yet

- Valuation: © The Institute of Chartered Accountants of IndiaDocument72 pagesValuation: © The Institute of Chartered Accountants of IndiaNmNo ratings yet

- Company Financial Statements - FORMAT LTDDocument5 pagesCompany Financial Statements - FORMAT LTDrumelrashid_seuNo ratings yet

- Group Project 1 - 2023Document10 pagesGroup Project 1 - 2023Aina SaffiyahNo ratings yet

- 4q19 Cimb Group Financial StatementsDocument70 pages4q19 Cimb Group Financial StatementsShaheer AliNo ratings yet

- Dec09 Inv Presentation GAAPDocument23 pagesDec09 Inv Presentation GAAPOladipupo Mayowa PaulNo ratings yet

- Tutorial 13 14 RevisedDocument4 pagesTutorial 13 14 RevisedEsther LuehNo ratings yet

- BFA301 Solution For Lecture Example 3-2Document6 pagesBFA301 Solution For Lecture Example 3-2erinNo ratings yet

- F6mys 2010 AnsDocument8 pagesF6mys 2010 AnsHar San LeeNo ratings yet

- Co Operative Bank of Kenya LTD Audited Financial Results For The Period Ended 31 Dec 2021Document3 pagesCo Operative Bank of Kenya LTD Audited Financial Results For The Period Ended 31 Dec 2021gilton amadadiNo ratings yet

- Test 3 SolutionsDocument4 pagesTest 3 SolutionsSAMNo ratings yet

- Adv CH 2Document52 pagesAdv CH 2Yonas AlemuNo ratings yet

- Eem Mid 1-2013Document2 pagesEem Mid 1-2013bhlprajuNo ratings yet

- December 2018: Nur Amira Nadia Binti Azizi 2018404898 BA1185FDocument4 pagesDecember 2018: Nur Amira Nadia Binti Azizi 2018404898 BA1185FNur Amira NadiaNo ratings yet

- Realestate Annual Handbook 2018Document65 pagesRealestate Annual Handbook 2018Sayed DanishNo ratings yet

- Group Project 2 - Published Account DEC2019 FAR270 - SSDocument6 pagesGroup Project 2 - Published Account DEC2019 FAR270 - SSHaru BiruNo ratings yet

- ICAEW Mar 2020 - Q4Document4 pagesICAEW Mar 2020 - Q4leejw2810No ratings yet

- IFRIC 14 - Class Practice (Solutions)Document4 pagesIFRIC 14 - Class Practice (Solutions)Muhammed NaqiNo ratings yet

- 00000Document30 pages00000ImanNo ratings yet

- Vitrox q22020Document16 pagesVitrox q22020Dennis AngNo ratings yet

- Assets: Balance Sheet As of September 31, 2020Document91 pagesAssets: Balance Sheet As of September 31, 2020Glennizze GalvezNo ratings yet

- Financial Information of PT SrikandiDocument1 pageFinancial Information of PT SrikandiNadira AristyaNo ratings yet

- ADB Interim FinancialDocument17 pagesADB Interim FinancialNurul HidayahNo ratings yet

- ACCT 4200 Project Solution - Final Posting 2022Document14 pagesACCT 4200 Project Solution - Final Posting 2022Jaspal SinghNo ratings yet

- FSA - Tutorial 6-Fall 2023 With SolutionsDocument5 pagesFSA - Tutorial 6-Fall 2023 With SolutionsnourbenmiledtbsNo ratings yet

- Income Statements For The November: @Chapter7AnalyslngandlnterpretlngflnanclalstatementsDocument1 pageIncome Statements For The November: @Chapter7AnalyslngandlnterpretlngflnanclalstatementsAik Luen LimNo ratings yet

- Test 3 2019 MemoDocument5 pagesTest 3 2019 MemoKoti KatishiNo ratings yet

- Assets Rupees in Million: Other Comprehensive IncomeDocument9 pagesAssets Rupees in Million: Other Comprehensive IncomeAziz TalbaniNo ratings yet

- Acc117 Ass 3Document12 pagesAcc117 Ass 3izma hadirNo ratings yet

- Tutorial 5 Jan 2022 Question OnlyDocument8 pagesTutorial 5 Jan 2022 Question OnlyMurali RasamahNo ratings yet

- TUTORIAL 6 - Increasing Shareholding (Answer) : UKAF4034 Advanced Corporate Reporting (Tutorial 6)Document11 pagesTUTORIAL 6 - Increasing Shareholding (Answer) : UKAF4034 Advanced Corporate Reporting (Tutorial 6)Murali RasamahNo ratings yet

- Tutorial 6 Q1 2 and 4 Excel AnswersDocument23 pagesTutorial 6 Q1 2 and 4 Excel AnswersMurali RasamahNo ratings yet

- Tutorial 3 Answer SegmentalDocument6 pagesTutorial 3 Answer Segmental--bolabolaNo ratings yet

- (Answer) : Tutorial 2 (MFRS 124 - Related Party Disclosures)Document11 pages(Answer) : Tutorial 2 (MFRS 124 - Related Party Disclosures)Murali RasamahNo ratings yet

- Construction ContractDocument17 pagesConstruction ContractYvonne Gam-oyNo ratings yet

- Jakawali ParachuteDocument1 pageJakawali Parachuteparasailing jakartaNo ratings yet

- MG8591 Principles of Management 2,13 MARKS Converted 1Document90 pagesMG8591 Principles of Management 2,13 MARKS Converted 14723 Nilamani M100% (1)

- Elimination Questions Elimination QuestionsDocument4 pagesElimination Questions Elimination QuestionsasffghjkNo ratings yet

- Tribune 17th June 2023Document30 pagesTribune 17th June 2023adam shingeNo ratings yet

- Midterm International Economics 2023Document4 pagesMidterm International Economics 2023Nhi Nguyễn YếnNo ratings yet

- CSE4003 - Cyber Security: Digital Assignment IDocument15 pagesCSE4003 - Cyber Security: Digital Assignment IjustadityabistNo ratings yet

- Law Chapter 3Document6 pagesLaw Chapter 3Yap AustinNo ratings yet

- Review of Related Literature OutlineDocument4 pagesReview of Related Literature OutlineSiote ChuaNo ratings yet

- Network Marketing Business Plan ExampleDocument50 pagesNetwork Marketing Business Plan ExampleJoseph QuillNo ratings yet

- Agricultural InsuranceDocument21 pagesAgricultural InsuranceSamer SahuNo ratings yet

- RTI ManualDocument79 pagesRTI Manualtnpsc2busarNo ratings yet

- AC415 Fixed Variable Costs BreakEven 1 - 11 - 2017Document35 pagesAC415 Fixed Variable Costs BreakEven 1 - 11 - 2017blablaNo ratings yet

- Chapter 6 PRACTICING AS AN ETHICAL ADMINISTRATIONDocument8 pagesChapter 6 PRACTICING AS AN ETHICAL ADMINISTRATIONJR Rolf NeuqeletNo ratings yet

- Understanding The Leadership Spectrum - Developing The SkillsDocument46 pagesUnderstanding The Leadership Spectrum - Developing The SkillsSam PoliasNo ratings yet

- Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002. byDocument56 pagesSecuritisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002. bykannangksNo ratings yet

- Faktor Resiko TBDocument15 pagesFaktor Resiko TBdrnurmayasarisihombingNo ratings yet

- Study Regarding Innovation and Entrepreneurship in Romanian SmesDocument6 pagesStudy Regarding Innovation and Entrepreneurship in Romanian SmesAlex ObrejanNo ratings yet

- Option Valuation Black ScholesDocument18 pagesOption Valuation Black ScholessanchiNo ratings yet

- Unit-5&6 Inst. Support To Ent. in Nepal-2Document65 pagesUnit-5&6 Inst. Support To Ent. in Nepal-2notes.mcpu0% (2)

- Major Project - AmolDocument47 pagesMajor Project - AmolAmol ShikariNo ratings yet

- Consolidated Financial Statement Excercise 3-4Document2 pagesConsolidated Financial Statement Excercise 3-4Winnie TanNo ratings yet

- CH 05Document37 pagesCH 05Janna KarapetyanNo ratings yet

- State of Afghan Cities 2015 Volume - 1Document156 pagesState of Afghan Cities 2015 Volume - 1United Nations Human Settlements Programme (UN-HABITAT)No ratings yet

- Digital Transformation OF FMCG Supply Chain: Case Presentation (Nitie, Mumbai)Document10 pagesDigital Transformation OF FMCG Supply Chain: Case Presentation (Nitie, Mumbai)snehaarpiNo ratings yet

- The Bond Market: Financial Markets and Institutions, Mishkin & EakinsDocument26 pagesThe Bond Market: Financial Markets and Institutions, Mishkin & EakinsKhondoker ShidurNo ratings yet

- List of PEREgistered On DLTDocument4,812 pagesList of PEREgistered On DLTVishalChaturvediNo ratings yet

- Std. X Ch. 3 Money and Credit WS (21 - 22)Document3 pagesStd. X Ch. 3 Money and Credit WS (21 - 22)YASHVI MODINo ratings yet

- Vendor DetailDocument4 pagesVendor DetailKamal PashaNo ratings yet

- TM 2Document28 pagesTM 2ArsaNo ratings yet