You might also like

- Review of Some Online Banks and Visa/Master Cards IssuersFrom EverandReview of Some Online Banks and Visa/Master Cards IssuersNo ratings yet

- Payments 101Document37 pagesPayments 101David Leeman100% (1)

- Rapid7 - Demystifying PCI DSS Ebook PDF - FinalDocument35 pagesRapid7 - Demystifying PCI DSS Ebook PDF - FinalellococarelocoNo ratings yet

- Evaluation of Some Online Payment Providers Services: Best Online Banks and Visa/Master Cards IssuersFrom EverandEvaluation of Some Online Payment Providers Services: Best Online Banks and Visa/Master Cards IssuersNo ratings yet

- Evaluation of Some Online Banks, E-Wallets and Visa/Master Card IssuersFrom EverandEvaluation of Some Online Banks, E-Wallets and Visa/Master Card IssuersNo ratings yet

- The Steps of Credit and Debit Card Payments ProcessingDocument4 pagesThe Steps of Credit and Debit Card Payments ProcessingAtharvaNo ratings yet

- WP PCI Compliance DFDocument8 pagesWP PCI Compliance DFjarihdNo ratings yet

- Payment Info Center: Your Source For Information About Electronic PaymentsDocument4 pagesPayment Info Center: Your Source For Information About Electronic Paymentssanchitarora11No ratings yet

- Summary of Ahmed Siddiqui & Nicholas Straight's The Anatomy of the SwipeFrom EverandSummary of Ahmed Siddiqui & Nicholas Straight's The Anatomy of the SwipeNo ratings yet

- Modern Treasury - Setting Up Your Payment Operations ArchitectureDocument15 pagesModern Treasury - Setting Up Your Payment Operations Architecturefelipeap92No ratings yet

- The Insider's Guide To Ecommerce PaymentDocument20 pagesThe Insider's Guide To Ecommerce PaymentJean Marc LouisNo ratings yet

- Aml KycDocument6 pagesAml KycChristopher Berlandier100% (2)

- A Short Guide To An Important Process : BeginDocument22 pagesA Short Guide To An Important Process : BeginSohail AhmedNo ratings yet

- Simplifying PCI Compliance For IT ProfessionalDocument9 pagesSimplifying PCI Compliance For IT ProfessionalAdeshina Segun AbefeNo ratings yet

- Draft 4 - Types of Merchant Fraud For PAsDocument3 pagesDraft 4 - Types of Merchant Fraud For PAsKunwarbir Singh lohatNo ratings yet

- Who Are The Players in The Credit Card Lifecycle?Document3 pagesWho Are The Players in The Credit Card Lifecycle?swathi bommineniNo ratings yet

- KYC For CryptoGuideDocument25 pagesKYC For CryptoGuidePatricio FagaldeNo ratings yet

- Payment Gateway ThesisDocument5 pagesPayment Gateway Thesiskaraliuerie100% (2)

- Chicken ND Egg-EpaymentsDocument28 pagesChicken ND Egg-Epaymentsstriker26No ratings yet

- Utilization of Rules in Anti-Money Laundering Compliance Monitoring ProgramsDocument5 pagesUtilization of Rules in Anti-Money Laundering Compliance Monitoring ProgramsdavejaiNo ratings yet

- E CommerceDocument7 pagesE CommerceNimya RoyNo ratings yet

- White Paper - All About Ecommerce and Payment GatewaysDocument8 pagesWhite Paper - All About Ecommerce and Payment GatewaysschoginiNo ratings yet

- Why Sotware Vendors Should Be Payment Facilitators: Key Verical MarketsDocument8 pagesWhy Sotware Vendors Should Be Payment Facilitators: Key Verical MarketsКарен ХачатрянNo ratings yet

- L2 Merchant AcquiringV1.0Document59 pagesL2 Merchant AcquiringV1.0Shweta AgrawalNo ratings yet

- Políticas e ProcedimentosDocument31 pagesPolíticas e ProcedimentosEliezer GuimarãesNo ratings yet

- How Credit Credit Card WorksDocument3 pagesHow Credit Credit Card WorksAnil KumarNo ratings yet

- Exois, Inc. - White Paper "Keys To PCI Success For Merchants"Document27 pagesExois, Inc. - White Paper "Keys To PCI Success For Merchants"Huy Trung NguyenNo ratings yet

- Ebook Ebusiness A Canadian Perspective For A Networked World Canadian 4Th Edition Trites Solutions Manual Full Chapter PDFDocument42 pagesEbook Ebusiness A Canadian Perspective For A Networked World Canadian 4Th Edition Trites Solutions Manual Full Chapter PDFquynhagneskrv100% (12)

- How Visa Makes Money and Understaning Visa Business ModelDocument5 pagesHow Visa Makes Money and Understaning Visa Business ModelAchintya MittalNo ratings yet

- National Payment SwitchDocument14 pagesNational Payment SwitchmikhlasNo ratings yet

- Final ReportDocument18 pagesFinal ReportNikki TaklikarNo ratings yet

- Credit Card ProcessingDocument28 pagesCredit Card ProcessingvluhadNo ratings yet

- Visa Security Alert: Protect Against Atm Cash-Out FraudDocument2 pagesVisa Security Alert: Protect Against Atm Cash-Out FraudAbdullah MithaniNo ratings yet

- What Are The Online Payment Methods in El Salvador For Virtual Stores and E-CommerceDocument7 pagesWhat Are The Online Payment Methods in El Salvador For Virtual Stores and E-CommerceOscar SundayNo ratings yet

- Linkedin Huali PostsDocument29 pagesLinkedin Huali Postsgoodlife laundryNo ratings yet

- Know Your Customer (Kyc) Regulations: Tip SheetDocument4 pagesKnow Your Customer (Kyc) Regulations: Tip Sheetdesign salamNo ratings yet

- Visa NetDocument22 pagesVisa NetPahul WaliaNo ratings yet

- PCI DSS Version 4.0: A guide to the payment card industry data security standardFrom EverandPCI DSS Version 4.0: A guide to the payment card industry data security standardNo ratings yet

- The Pci SSC Is An Open Global Forum: AgendaDocument10 pagesThe Pci SSC Is An Open Global Forum: AgendashreeNo ratings yet

- High Risk BusinessDocument17 pagesHigh Risk Business10922368No ratings yet

- Confessions of A BankerDocument59 pagesConfessions of A Bankeremanuelselfmade01No ratings yet

- Payment SystemDocument24 pagesPayment SystemTooba HashmiNo ratings yet

- Corporate Social ResponsibilityDocument11 pagesCorporate Social ResponsibilitySudha GuptaNo ratings yet

- What Is Know Your CustomerDocument9 pagesWhat Is Know Your CustomerAnaghaPuranikNo ratings yet

- Ecommerce Payment Services VGSoMDocument25 pagesEcommerce Payment Services VGSoMboldbuffNo ratings yet

- Hosted Payment Pages Security AlertsDocument2 pagesHosted Payment Pages Security AlertsbenNo ratings yet

- Launching A Digital Asset Exchange: Introductory GuideDocument7 pagesLaunching A Digital Asset Exchange: Introductory Guidenormand67No ratings yet

- Document Set (For JESUS HENRIQUE HERNANDEZ ALBORNOZ) - EncryptedDocument9 pagesDocument Set (For JESUS HENRIQUE HERNANDEZ ALBORNOZ) - Encryptedjesushernandez.alNo ratings yet

- How Credit Card Processing WorksDocument5 pagesHow Credit Card Processing WorksSmita ShetNo ratings yet

- Virgo ProposalDocument8 pagesVirgo ProposalWalterNo ratings yet

- Basic Business StartDocument10 pagesBasic Business Startfox406393No ratings yet

- Mojaloop AssessmentDocument15 pagesMojaloop AssessmentJeoffrey LimNo ratings yet

- Unit-4.4-Payment GatewaysDocument8 pagesUnit-4.4-Payment GatewaysShivam SinghNo ratings yet

- Payment Collection for Small Business: QuickStudy Laminated Reference Guide to Customer Payment OptionsFrom EverandPayment Collection for Small Business: QuickStudy Laminated Reference Guide to Customer Payment OptionsNo ratings yet

- PLDT AcoDocument1 pagePLDT AcoWesNo ratings yet

- Electronic Payment Systems-FinalDocument105 pagesElectronic Payment Systems-FinalDileep VkNo ratings yet

- National Payment Switch: Bank of MauritiusDocument14 pagesNational Payment Switch: Bank of MauritiusdeepakNo ratings yet

- Nline Eight Management Ounseling Program For Ealthcare ProvidersDocument59 pagesNline Eight Management Ounseling Program For Ealthcare ProvidershermestriNo ratings yet

- Nline Eight Management Ounseling Program For Ealthcare ProvidersDocument49 pagesNline Eight Management Ounseling Program For Ealthcare ProvidershermestriNo ratings yet

- Gotelecare 2014 Franchise Disclosure DocumentDocument95 pagesGotelecare 2014 Franchise Disclosure DocumenthermestriNo ratings yet

- How To Protect Your Phone and Data Privacy at U.S. Customs - The Washington PostDocument4 pagesHow To Protect Your Phone and Data Privacy at U.S. Customs - The Washington PosthermestriNo ratings yet

- LifeextensionDocument84 pagesLifeextensionhermestriNo ratings yet

- Complementary List Injection: 30 MG (Hydrochloride) / ML in 1-mL AmpouleDocument35 pagesComplementary List Injection: 30 MG (Hydrochloride) / ML in 1-mL AmpoulehermestriNo ratings yet

- Token Match ICO ProfilesDocument23 pagesToken Match ICO ProfileshermestriNo ratings yet

- Molten Salt Presentation PDFDocument110 pagesMolten Salt Presentation PDFhermestriNo ratings yet

- The Future of Banking Is Open PDFDocument52 pagesThe Future of Banking Is Open PDFhermestriNo ratings yet

- Knee Webinar WorkbookDocument8 pagesKnee Webinar WorkbookhermestriNo ratings yet

- XIUS Payment BankDocument21 pagesXIUS Payment BankhermestriNo ratings yet

- Conns2Document4 pagesConns2serviceconsultancy005No ratings yet

- Office of The General Manager (Com-Rev) : Assam Power Distribution Company LTDDocument5 pagesOffice of The General Manager (Com-Rev) : Assam Power Distribution Company LTDishansri7776873No ratings yet

- Current Acct Statement - XX0388 - 12092023Document10 pagesCurrent Acct Statement - XX0388 - 12092023Ashwani KumarNo ratings yet

- Https WWW - Cimb.bizchannel - Com.my Corp Front Transactioninquiry - Do Action Doprint PDFDocument1 pageHttps WWW - Cimb.bizchannel - Com.my Corp Front Transactioninquiry - Do Action Doprint PDFSyed HanafieNo ratings yet

- Juntos Global Deploying Human Centered Design To Motivate The Newly BankedDocument17 pagesJuntos Global Deploying Human Centered Design To Motivate The Newly BankedAman Kumar JhaNo ratings yet

- Account Statement (Online)Document12 pagesAccount Statement (Online)Malikali AwanNo ratings yet

- Single Euro Payments AreaDocument13 pagesSingle Euro Payments AreaamaravatiNo ratings yet

- Seminar MWC Visa Token ServiceDocument11 pagesSeminar MWC Visa Token Servicesrx devNo ratings yet

- Payment Slip: Summary of Charges / Payments Current Bill AnalysisDocument4 pagesPayment Slip: Summary of Charges / Payments Current Bill AnalysisChong LexinNo ratings yet

- E - Business Unit-III, 2020Document15 pagesE - Business Unit-III, 2020Sourabh SoniNo ratings yet

- NMB Tariff Guide 2021Document2 pagesNMB Tariff Guide 2021Adul MahmoudNo ratings yet

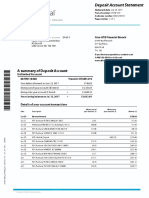

- A Summary of Deposit Account: Your ATB Financial BranchDocument2 pagesA Summary of Deposit Account: Your ATB Financial BranchMike SandruNo ratings yet

- 6 Dec - 5 JanDocument8 pages6 Dec - 5 JanEXE03 BilmedNo ratings yet

- Febr-Mar 2019Document7 pagesFebr-Mar 2019Ionut DumitrescuNo ratings yet

- Listaadmin 10 08 2021Document35 pagesListaadmin 10 08 2021carloshlc99No ratings yet

- 2020 BSRF Withdrawal FormDocument1 page2020 BSRF Withdrawal FormRifki SafrezaNo ratings yet

- Penyata Akaun: Tarikh Date Keterangan Description Terminal ID ID Terminal Amaun (RM) Amount (RM) Baki (RM) Balance (RM)Document6 pagesPenyata Akaun: Tarikh Date Keterangan Description Terminal ID ID Terminal Amaun (RM) Amount (RM) Baki (RM) Balance (RM)ABDUL HALIM BIN A WAHAB MoeNo ratings yet

- Account Statement: Transaction Date Value Date Description Debit Amount Credit Amount BalanceDocument2 pagesAccount Statement: Transaction Date Value Date Description Debit Amount Credit Amount BalanceAthul AjayanNo ratings yet

- 1-4 StatementDocument8 pages1-4 StatementNFAK LINENo ratings yet

- Application Form For Cheque Book and Debit Card IssuanceDocument2 pagesApplication Form For Cheque Book and Debit Card IssuanceAltoheed channelNo ratings yet

- Pe Perioada: 20-12-2023 - 05-01-2024 EXTRAS DE CONT Nr. 1 Din Data: 05-01-2024Document5 pagesPe Perioada: 20-12-2023 - 05-01-2024 EXTRAS DE CONT Nr. 1 Din Data: 05-01-2024Miki CristinaNo ratings yet

- Wirecard Funds Accessible Blog Post Updated - 30 June 2020 PDFDocument2 pagesWirecard Funds Accessible Blog Post Updated - 30 June 2020 PDFAsia Binta Amanat SumiNo ratings yet

- 70th PSME National Convention Invitation To Co Mechanical Engineers 0919Document2 pages70th PSME National Convention Invitation To Co Mechanical Engineers 0919Engr. harold JosephNo ratings yet

- IDFCFIRSTBankstatement 10070894160 005449576Document4 pagesIDFCFIRSTBankstatement 10070894160 005449576manishasurywanshi91No ratings yet

- Casa StrategyDocument2 pagesCasa StrategyS.s.SubramanianNo ratings yet

- Artificial Intelligence in FinanceDocument50 pagesArtificial Intelligence in FinancepatternprojectNo ratings yet

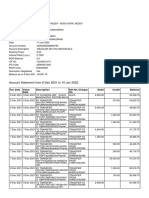

- Account StatementDocument12 pagesAccount StatementTonyNo ratings yet

- Robolox DescriptionDocument3 pagesRobolox DescriptionS E ENo ratings yet

- 3D Secure Guide PDFDocument7 pages3D Secure Guide PDFOliver JamesNo ratings yet

- Mahindra War Room: by Team: MarvinDocument14 pagesMahindra War Room: by Team: MarvinVanshGuptaNo ratings yet