You might also like

- Icici Direct ResearchDocument9 pagesIcici Direct Researchfinanceharsh6No ratings yet

- IDirect IEX Q4FY21Document5 pagesIDirect IEX Q4FY21SushilNo ratings yet

- Divis Idirect 241121Document9 pagesDivis Idirect 241121Peaceful InvestNo ratings yet

- IDirect UnitedSpirits Q4FY21Document6 pagesIDirect UnitedSpirits Q4FY21Ranjith ChackoNo ratings yet

- Buy - Vardhman TextilesIDirect - 1.11.2021.Document5 pagesBuy - Vardhman TextilesIDirect - 1.11.2021.Mritunjay BhartiNo ratings yet

- IDirect Powergrid Q3FY22Document6 pagesIDirect Powergrid Q3FY22Yakshit NangiaNo ratings yet

- ICICI Direct - Astec Lifesciences - Q3FY22Document7 pagesICICI Direct - Astec Lifesciences - Q3FY22Puneet367No ratings yet

- IDirect Bata Q4FY22Document8 pagesIDirect Bata Q4FY22Sarvesh AlavekarNo ratings yet

- 5paisa Capital: Curb in Opex Aids BottomlineDocument6 pages5paisa Capital: Curb in Opex Aids BottomlinePorus Saranjit SinghNo ratings yet

- Action Construction Equipment: Sturdy Performance..Document6 pagesAction Construction Equipment: Sturdy Performance..Aryan SharmaNo ratings yet

- Sterlite Technologies: Ambitious Target To Double Revenues in Three Years!Document8 pagesSterlite Technologies: Ambitious Target To Double Revenues in Three Years!Guarachandar ChandNo ratings yet

- Mahindra & Mahindra: (Mahmah)Document10 pagesMahindra & Mahindra: (Mahmah)Ashwet JadhavNo ratings yet

- HG Infra - 1QFY23RU - Idirect - Aug 4, 2022Document8 pagesHG Infra - 1QFY23RU - Idirect - Aug 4, 2022PavanNo ratings yet

- IDirect AartiInds Q4FY21Document9 pagesIDirect AartiInds Q4FY21AkchikaNo ratings yet

- IDirect ABFRL Q3FY22Document7 pagesIDirect ABFRL Q3FY22Parag SaxenaNo ratings yet

- HOLD Relaxo Footwears IDirect 16.5.2022Document9 pagesHOLD Relaxo Footwears IDirect 16.5.2022Vaishali AgrawalNo ratings yet

- HDFC Life Insurance: Healthy Growth Outlook On Growth OptimisticDocument7 pagesHDFC Life Insurance: Healthy Growth Outlook On Growth OptimisticJay BhushanNo ratings yet

- Vinati Organics: Newer Businesses To Drive Growth AheadDocument6 pagesVinati Organics: Newer Businesses To Drive Growth AheadtamilNo ratings yet

- IDirect GreavesCotton Q1FY23Document8 pagesIDirect GreavesCotton Q1FY23Ayush GoelNo ratings yet

- Abbott India: FY20 Performance Reflects Strength of Power BrandsDocument5 pagesAbbott India: FY20 Performance Reflects Strength of Power BrandspremNo ratings yet

- IDirect AstralPoly Q1FY23Document9 pagesIDirect AstralPoly Q1FY23Denish GalaNo ratings yet

- Sudarshan Chemical: Upcoming Capex Offers Strong Visibility AheadDocument7 pagesSudarshan Chemical: Upcoming Capex Offers Strong Visibility AheadEquityLabs IndiaNo ratings yet

- IDirect RelianceInd CoUpdate Dec22Document6 pagesIDirect RelianceInd CoUpdate Dec22adityazade03No ratings yet

- Pricol - CU-IDirect-Mar 3, 2022Document6 pagesPricol - CU-IDirect-Mar 3, 2022rajesh katareNo ratings yet

- SBI Cards and Payments: Long-Term Outlook Remains IntactDocument6 pagesSBI Cards and Payments: Long-Term Outlook Remains IntactRomelu MartialNo ratings yet

- IDirect TataChemical Q1FY23Document9 pagesIDirect TataChemical Q1FY23Ayush GoelNo ratings yet

- IDirect IDFCBank Q4FY23Document6 pagesIDirect IDFCBank Q4FY23Silambarasan AshokkumarNo ratings yet

- TCI Express IDirect 050822 EBRDocument8 pagesTCI Express IDirect 050822 EBRसुनिवेशक समूहNo ratings yet

- Titan Company (TITIND) : Multiple Levers in Place To Drive Sales GrowthDocument5 pagesTitan Company (TITIND) : Multiple Levers in Place To Drive Sales Growthaachen_24No ratings yet

- Lemon Tree Hotels.Document9 pagesLemon Tree Hotels.Anonymous brpVlaVBNo ratings yet

- HealthcareGlobal Idirect 180324 EBRDocument5 pagesHealthcareGlobal Idirect 180324 EBRamarjeetNo ratings yet

- IDirect SunPharma Q4FY23Document10 pagesIDirect SunPharma Q4FY23raj patilNo ratings yet

- IDirect Voltas Q1FY23Document11 pagesIDirect Voltas Q1FY23Rehan SkNo ratings yet

- IDirect TCS Q1FY23Document11 pagesIDirect TCS Q1FY23uefqyaufdQNo ratings yet

- IDirect HGInfra Q3FY23Document8 pagesIDirect HGInfra Q3FY23ROHIT PAREEKNo ratings yet

- TATACOMM ICICIDirect 06082021Document8 pagesTATACOMM ICICIDirect 06082021gbNo ratings yet

- Sterlite Technologies (STETEC) : Export Demand Drives GrowthDocument10 pagesSterlite Technologies (STETEC) : Export Demand Drives Growthsaran21No ratings yet

- IDirect Titan Q1FY23Document10 pagesIDirect Titan Q1FY23AKHILESH HEBBARNo ratings yet

- Glenmark Pharmaceuticals: Stable Numbers Margin Expansion To The ForeDocument11 pagesGlenmark Pharmaceuticals: Stable Numbers Margin Expansion To The ForeChirag NakumNo ratings yet

- IDirect Glenmark Q3FY22Document9 pagesIDirect Glenmark Q3FY22sukeshNo ratings yet

- Divis RRDocument10 pagesDivis RRRicha P SinghalNo ratings yet

- Jubilant Pharmova 07 06 2021 IciciDocument6 pagesJubilant Pharmova 07 06 2021 IciciBhagwat RautelaNo ratings yet

- Pawan Agraw Al: Conference Call With The Analyst/Investors-PresentationDocument74 pagesPawan Agraw Al: Conference Call With The Analyst/Investors-PresentationLight YagamiNo ratings yet

- Ad AnalysisDocument6 pagesAd Analysisnani reddyNo ratings yet

- IDirect Mindtree Q1FY23Document11 pagesIDirect Mindtree Q1FY23Porus Saranjit SinghNo ratings yet

- Ultratech Cement: Margin Stays Firm Outlook Remains HealthyDocument9 pagesUltratech Cement: Margin Stays Firm Outlook Remains HealthyHarsh ShahNo ratings yet

- ICICI Direct Sagar CementDocument10 pagesICICI Direct Sagar CementRithuik YerrabroluNo ratings yet

- Leaders of Tomorrow2Document19 pagesLeaders of Tomorrow2Dara ShyamsundarNo ratings yet

- IDirect JustDial CoUpdate Jul21Document5 pagesIDirect JustDial CoUpdate Jul21ShivangimahadevNo ratings yet

- ABBOTT INDIA LTD - ICICI Direct - Co Update - 260819 - Strong Revenue Growth With Margin ImprovementDocument4 pagesABBOTT INDIA LTD - ICICI Direct - Co Update - 260819 - Strong Revenue Growth With Margin ImprovementShanti RanganNo ratings yet

- Sumitomo Chemicals: CRAMS Offers Strong Visibility AheadDocument7 pagesSumitomo Chemicals: CRAMS Offers Strong Visibility AheadhamsNo ratings yet

- IDirect SunTV Q2FY22Document7 pagesIDirect SunTV Q2FY22Sarah AliceNo ratings yet

- IDirect Pidilite Q1FY22Document8 pagesIDirect Pidilite Q1FY22Ranjith ChackoNo ratings yet

- Icici DmartDocument6 pagesIcici DmartGOUTAMNo ratings yet

- IDirect GranulesIndia Q1FY22Document9 pagesIDirect GranulesIndia Q1FY22YASH CHAUDHARYNo ratings yet

- Time TechnoplastDocument8 pagesTime Technoplastagrawal.minNo ratings yet

- IDirect Berger Q2FY23Document9 pagesIDirect Berger Q2FY23Rutuparna mohantyNo ratings yet

- V-Mart: Annual Report FY18: Improvement Across Key ParametersDocument14 pagesV-Mart: Annual Report FY18: Improvement Across Key ParametersRanjan KumarNo ratings yet

- Bata India: Steady Revenue Recovery To Aid Premiumisation PlayDocument4 pagesBata India: Steady Revenue Recovery To Aid Premiumisation PlayAnkita NegiNo ratings yet

- Rural Marketing, 2eDocument14 pagesRural Marketing, 2eRahul AggarwalNo ratings yet

- Doosan - CaseDocument6 pagesDoosan - CaseRahul AggarwalNo ratings yet

- Enabling A Step Change in User Experience and Perception With Holistic ExperienceDocument1 pageEnabling A Step Change in User Experience and Perception With Holistic ExperienceRahul AggarwalNo ratings yet

- 61e3c581208ea Vichaar Case StudyDocument22 pages61e3c581208ea Vichaar Case StudyRahul AggarwalNo ratings yet

- Group No. 09 - WM Batch 3 - Shirish GoelDocument6 pagesGroup No. 09 - WM Batch 3 - Shirish GoelRahul AggarwalNo ratings yet

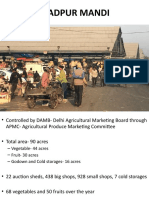

- Azadpur MandiDocument11 pagesAzadpur MandiRahul AggarwalNo ratings yet

- Concetto 5.0: Analysing Tea Market in IndiaDocument6 pagesConcetto 5.0: Analysing Tea Market in IndiaRahul AggarwalNo ratings yet

- The Rural Boom in India: Pradeep KashyapDocument10 pagesThe Rural Boom in India: Pradeep KashyapRahul AggarwalNo ratings yet

- Rural Marketing: Seelampur VisitDocument15 pagesRural Marketing: Seelampur VisitRahul AggarwalNo ratings yet

- Corporation Hand Out - RevisedDocument11 pagesCorporation Hand Out - RevisedEichelle Joy ZuluetaNo ratings yet

- ImpairmentDocument22 pagesImpairmentRaine PiliinNo ratings yet

- One Person Company by Sabarnee ChatterjeeDocument11 pagesOne Person Company by Sabarnee ChatterjeeSabarnee Chatterjee50% (2)

- 6.MAF 603 CH 10 - Mergers, Acquisitions and DivestituresDocument45 pages6.MAF 603 CH 10 - Mergers, Acquisitions and DivestituresSullivan LyaNo ratings yet

- Chapter 10Document40 pagesChapter 10joyabyss100% (1)

- Acct 2011 Anderson Pty LTD Is An Australian Diversified IndustrialDocument2 pagesAcct 2011 Anderson Pty LTD Is An Australian Diversified IndustrialCharlotteNo ratings yet

- Finance Module 01 - Week 1Document14 pagesFinance Module 01 - Week 1Christian ZebuaNo ratings yet

- Dr. Domingo Clinic Chart of Accounts: Account Numbers Account Titles Current AssetsDocument2 pagesDr. Domingo Clinic Chart of Accounts: Account Numbers Account Titles Current AssetsmariaNo ratings yet

- School of Business and Management Sciences Departmentof Electronic CommerceDocument6 pagesSchool of Business and Management Sciences Departmentof Electronic Commercesamantha dobaNo ratings yet

- R03.7 Guidance For Standard VDocument18 pagesR03.7 Guidance For Standard VBảo TrâmNo ratings yet

- Main Exam 2014-Sol-1Document7 pagesMain Exam 2014-Sol-1Diego AguirreNo ratings yet

- Introduction - Joint Stock CompanyDocument5 pagesIntroduction - Joint Stock Companyiisjaffer100% (3)

- Use The Following Information To Answer Items 3 and 4Document15 pagesUse The Following Information To Answer Items 3 and 4charlies parrenoNo ratings yet

- Cogent Analytics M&A ManualDocument19 pagesCogent Analytics M&A Manualvan070100% (1)

- SMC Financial Statements 2012Document104 pagesSMC Financial Statements 2012Christian D. OrbeNo ratings yet

- Philippine Bonded Warehouse Services, Inc. Application For Accreditation To CCBW 1415Document3 pagesPhilippine Bonded Warehouse Services, Inc. Application For Accreditation To CCBW 1415Itsfreynk05No ratings yet

- Roadmap To IND ASDocument2 pagesRoadmap To IND ASKhushi SoniNo ratings yet

- NRI Investment in Indian StartupsDocument10 pagesNRI Investment in Indian StartupsAdityaNo ratings yet

- Chap 21 - Leasing (PSAK 73) - E12-12Document27 pagesChap 21 - Leasing (PSAK 73) - E12-12Happy MichaelNo ratings yet

- Corporate Finance: Topic: Company Analysis "Infosys"Document6 pagesCorporate Finance: Topic: Company Analysis "Infosys"Anuradha SinghNo ratings yet

- Bridge Loan - InvestopediaDocument3 pagesBridge Loan - InvestopediaBob KaneNo ratings yet

- Cost and Management Accounting IIDocument66 pagesCost and Management Accounting IIsamuel debebeNo ratings yet

- Chapter 10 - Cash To Accrual Basis of AccountingDocument3 pagesChapter 10 - Cash To Accrual Basis of AccountingJEFFERSON CUTENo ratings yet

- Calendar FY18 For Any CompanyDocument1 pageCalendar FY18 For Any CompanyburnoutcandleNo ratings yet

- Kimberly C. GleasonDocument44 pagesKimberly C. Gleasonfisayobabs11No ratings yet

- FM Class Capital BudgetingDocument39 pagesFM Class Capital BudgetingEviya Jerrin KoodalyNo ratings yet

- Furniture Business PlanDocument23 pagesFurniture Business Planjsean.ahadNo ratings yet

- Bab 5 Analisis Laporan KeuanganDocument54 pagesBab 5 Analisis Laporan KeuanganBenedict MihoyoNo ratings yet

- E 14-6 Acquisition-Excess Allocation and Amortization EffectDocument13 pagesE 14-6 Acquisition-Excess Allocation and Amortization EffectRizkina MoelNo ratings yet

- TYBAF Project TopicsDocument2 pagesTYBAF Project Topicsseema mundaleNo ratings yet

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 3.5 out of 5 stars3.5/5 (8)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successFrom EverandReady, Set, Growth hack:: A beginners guide to growth hacking successRating: 4.5 out of 5 stars4.5/5 (93)

- An easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyFrom EverandAn easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyRating: 3 out of 5 stars3/5 (1)

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamFrom EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamNo ratings yet

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthFrom EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthRating: 4 out of 5 stars4/5 (20)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- Built, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursFrom EverandBuilt, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursRating: 5 out of 5 stars5/5 (13)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)

- Creating Shareholder Value: A Guide For Managers And InvestorsFrom EverandCreating Shareholder Value: A Guide For Managers And InvestorsRating: 4.5 out of 5 stars4.5/5 (8)

- The Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsFrom EverandThe Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsNo ratings yet

- Product-Led Growth: How to Build a Product That Sells ItselfFrom EverandProduct-Led Growth: How to Build a Product That Sells ItselfRating: 5 out of 5 stars5/5 (1)

- Mastering the VC Game: A Venture Capital Insider Reveals How to Get from Start-up to IPO on Your TermsFrom EverandMastering the VC Game: A Venture Capital Insider Reveals How to Get from Start-up to IPO on Your TermsRating: 4.5 out of 5 stars4.5/5 (21)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- Valley Girls: Lessons From Female Founders in the Silicon Valley and BeyondFrom EverandValley Girls: Lessons From Female Founders in the Silicon Valley and BeyondNo ratings yet

- Mind over Money: The Psychology of Money and How to Use It BetterFrom EverandMind over Money: The Psychology of Money and How to Use It BetterRating: 4 out of 5 stars4/5 (24)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (8)

- Finance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)From EverandFinance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)Rating: 4 out of 5 stars4/5 (5)

- Buffett's 2-Step Stock Market Strategy: Know When To Buy A Stock, Become A Millionaire, Get The Highest ReturnsFrom EverandBuffett's 2-Step Stock Market Strategy: Know When To Buy A Stock, Become A Millionaire, Get The Highest ReturnsRating: 5 out of 5 stars5/5 (1)

- The Value of a Whale: On the Illusions of Green CapitalismFrom EverandThe Value of a Whale: On the Illusions of Green CapitalismRating: 5 out of 5 stars5/5 (2)