You might also like

- 61a8953c7b94b - Account English NotesDocument23 pages61a8953c7b94b - Account English NotesAnuska ThapaNo ratings yet

- Digital Assignment-2: Yogesh. A 19BCC0028Document8 pagesDigital Assignment-2: Yogesh. A 19BCC0028Ash KetchumNo ratings yet

- Financial Reporting & Analysis Study MaterialDocument127 pagesFinancial Reporting & Analysis Study Materialxaseyay235No ratings yet

- Accounting Notes Module - 1Document16 pagesAccounting Notes Module - 1Bheemeswar ReddyNo ratings yet

- Accountingppt 140927013707 Phpapp02 PDFDocument25 pagesAccountingppt 140927013707 Phpapp02 PDFANKITNo ratings yet

- AccountingDocument22 pagesAccountingawdadadNo ratings yet

- Accounting ConceptsDocument8 pagesAccounting ConceptsBajra VinayaNo ratings yet

- Business AccountingDocument25 pagesBusiness AccountingYash PatawariNo ratings yet

- Concepts ConventionsDocument5 pagesConcepts Conventionssinghriya2513No ratings yet

- Accounts Notes 1Document7 pagesAccounts Notes 1Dynmc ThugzNo ratings yet

- Basics of Business AccountingDocument34 pagesBasics of Business AccountingMadhusmita MishraNo ratings yet

- Accounting Concepts and ConventionsDocument2 pagesAccounting Concepts and ConventionsWelcome 1995No ratings yet

- Unit-1:-Introduction of Financial Management Accounting, Book Keeping & RecordingDocument5 pagesUnit-1:-Introduction of Financial Management Accounting, Book Keeping & RecordingShradha KapseNo ratings yet

- Book Keeping Form OneDocument97 pagesBook Keeping Form OneChizani MnyifunaNo ratings yet

- Accounting ConceptsDocument2 pagesAccounting Conceptssoumyasundar720No ratings yet

- Accounting and Financial ManagementDocument3 pagesAccounting and Financial ManagementDhara PatelNo ratings yet

- Accounting Concepts and ConventionsDocument40 pagesAccounting Concepts and ConventionsAmrita TatiaNo ratings yet

- CPT Accounts ThoeryDocument6 pagesCPT Accounts ThoeryanandvkakuNo ratings yet

- Concepts: Introduction To Financial AccountingDocument30 pagesConcepts: Introduction To Financial Accountingbmurali37No ratings yet

- Topic OneDocument21 pagesTopic Onesammie celeNo ratings yet

- Accounts TheoryDocument73 pagesAccounts Theoryaneupane465No ratings yet

- Concepts & Conventions in AccountingDocument5 pagesConcepts & Conventions in Accountingpratz dhakateNo ratings yet

- BasicConceptofManagerialAccounting Unit 1Document9 pagesBasicConceptofManagerialAccounting Unit 1sourabhdangarhNo ratings yet

- AFM Question Bank For 16MBA13 SchemeDocument10 pagesAFM Question Bank For 16MBA13 SchemeChandan Dn Gowda100% (1)

- Accounting Concepts: 1. The Business Entity ConceptDocument2 pagesAccounting Concepts: 1. The Business Entity Conceptnikita bajpaiNo ratings yet

- Accounting PrinciplesDocument4 pagesAccounting PrinciplesManjulaNo ratings yet

- Module-1: Accounting Concepts and ConventionsDocument14 pagesModule-1: Accounting Concepts and ConventionsSai kiran VeeravalliNo ratings yet

- Accounting Concepts and ConventionsDocument7 pagesAccounting Concepts and ConventionsPraveenKumarPraviNo ratings yet

- Unit 1 TAPDocument19 pagesUnit 1 TAPchethanraaz_66574068No ratings yet

- GAAPDocument14 pagesGAAPMr SuTtUNo ratings yet

- Accounting Concepts and ConventionsDocument4 pagesAccounting Concepts and ConventionsPrincess RubyNo ratings yet

- 2.basic Accounting Concepts and ConventionsDocument10 pages2.basic Accounting Concepts and ConventionsLakshmanrao NayiniNo ratings yet

- Company Outsiders: Resources TodayDocument20 pagesCompany Outsiders: Resources TodaySarbani Mishra0% (1)

- Unit - Ii Introduction To Financial AccountingDocument37 pagesUnit - Ii Introduction To Financial AccountingdownloaderNo ratings yet

- Afm 2Document3 pagesAfm 2helpevery7No ratings yet

- Accounting Concepts F5Document7 pagesAccounting Concepts F5Tinevimbo NdlovuNo ratings yet

- Accountancy: Accounting Is The Language of The BusinessDocument41 pagesAccountancy: Accounting Is The Language of The BusinessAnand Mishra100% (1)

- Balance Sheet BasicsDocument24 pagesBalance Sheet Basicsnavya sreeNo ratings yet

- Financial and Management AccountingDocument9 pagesFinancial and Management AccountingyogipendliNo ratings yet

- Syllabus: Subject - Financial AccountingDocument74 pagesSyllabus: Subject - Financial AccountingAnitha RNo ratings yet

- Financial Accounting Notes B.com 1st SemDocument64 pagesFinancial Accounting Notes B.com 1st SemJeevesh Roy0% (1)

- The Original Attachment: BasicsDocument32 pagesThe Original Attachment: BasicsVijayGogulaNo ratings yet

- Accounting NotesDocument71 pagesAccounting Noteswaseem ahsanNo ratings yet

- Accounting ConceptsDocument4 pagesAccounting ConceptsAjmal KhanNo ratings yet

- BCOM 1 Financial Accounting 1Document63 pagesBCOM 1 Financial Accounting 1karthikeyan01No ratings yet

- MBA Financial AccountingDocument57 pagesMBA Financial AccountingNaresh Guduru100% (1)

- Accounting Concepts and Priciples: Fundamentals of Accountancy, Business and Management 1Document10 pagesAccounting Concepts and Priciples: Fundamentals of Accountancy, Business and Management 1Marilyn Nelmida TamayoNo ratings yet

- Accounting Concept Refers To The Basic Assumptions and Rules andDocument4 pagesAccounting Concept Refers To The Basic Assumptions and Rules andManisha SharmaNo ratings yet

- Chapter 3 Analyzing Transactions To Start A BusinessDocument3 pagesChapter 3 Analyzing Transactions To Start A BusinessPaw VerdilloNo ratings yet

- Basics of Accounting Theory: AppendixDocument6 pagesBasics of Accounting Theory: AppendixRushelle Vergara MosepNo ratings yet

- Principle of Accounting Notes CompleteDocument34 pagesPrinciple of Accounting Notes Completemuzammilamiri2No ratings yet

- Agri Rahulic: Accounting Concepts and Conventions of AccountingDocument3 pagesAgri Rahulic: Accounting Concepts and Conventions of AccountingAgricultural RahulicNo ratings yet

- Financial Accounting-Short Answers Revision NotesDocument26 pagesFinancial Accounting-Short Answers Revision Notesfathimathabasum100% (7)

- Accounting Concepts and ConventionsDocument17 pagesAccounting Concepts and ConventionsKathuria AmanNo ratings yet

- Accounting Concepts and ConventionsDocument13 pagesAccounting Concepts and Conventionssunsign100% (1)

- Assignment (Fundamentals of Book - Keeping & Accounting)Document25 pagesAssignment (Fundamentals of Book - Keeping & Accounting)api-370836989% (9)

- AccountingDocument5 pagesAccountingCma Pushparaj KulkarniNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- Mid Term Question Paper - Corporate Governanace and Ethics-Sem IV Batch 2020-2022 PDFDocument3 pagesMid Term Question Paper - Corporate Governanace and Ethics-Sem IV Batch 2020-2022 PDFshruthiNo ratings yet

- Conflict and Negotiation - Question Paper Set 1-Semester 4 - Batch 2020-22Document2 pagesConflict and Negotiation - Question Paper Set 1-Semester 4 - Batch 2020-22shruthiNo ratings yet

- Correlation and Data DistributionDocument21 pagesCorrelation and Data DistributionshruthiNo ratings yet

- Unit 1 BSDocument30 pagesUnit 1 BSshruthiNo ratings yet

- Entrep Module 1 Q1Document14 pagesEntrep Module 1 Q1MacyNo ratings yet

- StashFin IntroDocument12 pagesStashFin IntroMohit Garg100% (1)

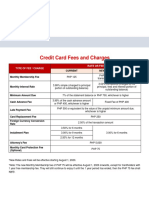

- Credit Card Fees and Charges: Type of Fee / Charge Rate or FeeDocument1 pageCredit Card Fees and Charges: Type of Fee / Charge Rate or FeeKram Yer EtentepmocNo ratings yet

- Bill Gates - Business at The Speed of ThoughtDocument64 pagesBill Gates - Business at The Speed of Thoughtадміністратор Wake Up SchoolNo ratings yet

- Amc Case StudyDocument2 pagesAmc Case StudyAishwarya SundararajNo ratings yet

- 2023 Budget Ordinance First ReadingDocument3 pages2023 Budget Ordinance First ReadinginforumdocsNo ratings yet

- Quarter 3 Summative Test 1Document4 pagesQuarter 3 Summative Test 1Maria CongNo ratings yet

- Balance of Payment: DR - Pinki ShahDocument12 pagesBalance of Payment: DR - Pinki ShahRain StarNo ratings yet

- Strategic Management Concepts Competitiveness and Globalization Hitt 11th Edition Solutions Manual Full DownloadDocument11 pagesStrategic Management Concepts Competitiveness and Globalization Hitt 11th Edition Solutions Manual Full Downloaddonnaparkermepfikcndx100% (36)

- Careem's Owner HandbookDocument103 pagesCareem's Owner HandbookgateebNo ratings yet

- JD 60 13Document13 pagesJD 60 13nlrbdocsNo ratings yet

- 6QQMN331 Sample Essay 2Document28 pages6QQMN331 Sample Essay 2dance.yards0vNo ratings yet

- SJB ProfileDocument4 pagesSJB ProfileSourajit PattanaikNo ratings yet

- PART 1 An Overview of Strategic Retail Management 21: Chapter 1 An Introduction To Retailing 22Document1 pagePART 1 An Overview of Strategic Retail Management 21: Chapter 1 An Introduction To Retailing 22AlesmanNo ratings yet

- Faq Transitional Issues Companies Act 2016 - Technical 2 2 2017 PDFDocument14 pagesFaq Transitional Issues Companies Act 2016 - Technical 2 2 2017 PDFazilaNo ratings yet

- Break-Even Level of Output BUSINESS STUDIES IGCSEDocument3 pagesBreak-Even Level of Output BUSINESS STUDIES IGCSEHriday KotechaNo ratings yet

- ACS 1000 Preventive MaintenanceDocument2 pagesACS 1000 Preventive Maintenanceazultenue780% (1)

- Define PERT and CPM in Project Management and Its Importance and PROS and Cons of Pert and CPM in Project ManagementDocument4 pagesDefine PERT and CPM in Project Management and Its Importance and PROS and Cons of Pert and CPM in Project Managementbaskar rajuNo ratings yet

- Intermediate Accounting 2 (Notes Payable) - Problem 2Document3 pagesIntermediate Accounting 2 (Notes Payable) - Problem 2DM MontefalcoNo ratings yet

- Deed of Sale of Motor VehicleDocument1 pageDeed of Sale of Motor VehicleJoemar CalunaNo ratings yet

- Marketing Strategies of Cornetto, WallsDocument13 pagesMarketing Strategies of Cornetto, Wallsmaham aziz100% (1)

- 2nd RMA For 30 RADIOsDocument4 pages2nd RMA For 30 RADIOsmohamedNo ratings yet

- Brand DecisionsDocument38 pagesBrand Decisionssonalidhanokar9784100% (2)

- Customer Information Sheet (CRL-FM-ADMN-049) - r1Document1 pageCustomer Information Sheet (CRL-FM-ADMN-049) - r1alvin salmingoNo ratings yet

- A Project Report On Group InsuranceDocument64 pagesA Project Report On Group Insurancesharinair1393% (15)

- Cadweld Multi: An Evolution in Exothermic WeldingDocument2 pagesCadweld Multi: An Evolution in Exothermic Weldingakshaf10No ratings yet

- Tata Technologies IPO PDF 201123Document1 pageTata Technologies IPO PDF 201123Hitesh PhulwaniNo ratings yet

- Example RA Working at Height Risk AssessmentDocument6 pagesExample RA Working at Height Risk AssessmentYossef K FawzyNo ratings yet

- Supplying The Fashion Product-Assessment 1-Range Plan ReportDocument31 pagesSupplying The Fashion Product-Assessment 1-Range Plan Reportapi-292074531No ratings yet

- 426 Exam 2 Questions AnswersDocument25 pages426 Exam 2 Questions AnswersIlya StadnikNo ratings yet