You might also like

- LIFEAsia Base System Guide V10.1 LatestDocument291 pagesLIFEAsia Base System Guide V10.1 LatestCM100% (5)

- Transaction Monitoring Analyst Assessment TestDocument11 pagesTransaction Monitoring Analyst Assessment TestSreenivasulu Bodolla50% (2)

- FABM2 Q2 Module WS 1Document14 pagesFABM2 Q2 Module WS 1Mitch Dumlao73% (11)

- Bank Reconciliation StatementDocument19 pagesBank Reconciliation StatementJaneth Bootan ProtacioNo ratings yet

- Nature of Bank Reconciliation StatementDocument15 pagesNature of Bank Reconciliation StatementMidsy De la Cruz75% (4)

- Bizmanualz Accounting Policies and Procedures SampleDocument10 pagesBizmanualz Accounting Policies and Procedures Sampleallukazoldyck100% (1)

- Accounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCFrom EverandAccounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCRating: 5 out of 5 stars5/5 (1)

- New Patient Information SheetDocument1 pageNew Patient Information Sheetharrisk31No ratings yet

- Introduction and Importance of Bank Reconciliation Statement (BRS)Document12 pagesIntroduction and Importance of Bank Reconciliation Statement (BRS)Rizwan BashirNo ratings yet

- What Is A Bank Reconciliation StatementDocument3 pagesWhat Is A Bank Reconciliation StatementYassi CurtisNo ratings yet

- Accounting - Reconcilliation 22 JanDocument37 pagesAccounting - Reconcilliation 22 JanGamaya EmmanuelNo ratings yet

- Businesses Errors: Preparation of Bank Reconciliation StatementDocument5 pagesBusinesses Errors: Preparation of Bank Reconciliation StatementPREX WEXNo ratings yet

- Bank Reconciliation: Home Financial Accounting Cash and EquivalentsDocument2 pagesBank Reconciliation: Home Financial Accounting Cash and EquivalentsMayur KundarNo ratings yet

- Bank Reconciliation StatementDocument5 pagesBank Reconciliation StatementakankaroraNo ratings yet

- Bank ReconciliationDocument9 pagesBank ReconciliationhoxhiiNo ratings yet

- June 2012 Business Entity Concept: Accounting ImplicationsDocument5 pagesJune 2012 Business Entity Concept: Accounting ImplicationsAnonymous NSNpGa3T93No ratings yet

- Bookkeeping To Trial Balance 9Document17 pagesBookkeeping To Trial Balance 9elelwaniNo ratings yet

- Bank Reconciliation (Theories and Concept) : Bank Reconciliation, According To Williams, Haka, Et - Al. (2008)Document3 pagesBank Reconciliation (Theories and Concept) : Bank Reconciliation, According To Williams, Haka, Et - Al. (2008)Princess MagpatocNo ratings yet

- VJ Mini ProjectDocument20 pagesVJ Mini ProjectRAKESH VARMANo ratings yet

- Bank Reconciliation Statement Class 11 NotesDocument10 pagesBank Reconciliation Statement Class 11 NotesAshna vargheseNo ratings yet

- Chapter Eight Bank Reconciliation-2Document67 pagesChapter Eight Bank Reconciliation-2Kingsley MweembaNo ratings yet

- Bank ReconciliationDocument3 pagesBank ReconciliationPatrick RazafindravonjyNo ratings yet

- Bank ReconciliationDocument9 pagesBank Reconciliationlit afNo ratings yet

- Fabm2 - June 17, 2021 Asynchronous Activity: Thanks, Happy Working. 3Document7 pagesFabm2 - June 17, 2021 Asynchronous Activity: Thanks, Happy Working. 3Khaira PeraltaNo ratings yet

- Bank - Reconciliatio Statement PowerpointDocument61 pagesBank - Reconciliatio Statement PowerpointLoida Yare LauritoNo ratings yet

- Bank Reconciliation Statement: Names of Sub-UnitsDocument6 pagesBank Reconciliation Statement: Names of Sub-UnitsHermann Schmidt EbengaNo ratings yet

- What Is ReconciliationDocument7 pagesWhat Is ReconciliationRamesh GarikapatiNo ratings yet

- Introduction To Bank ReconciliationDocument8 pagesIntroduction To Bank ReconciliationNath Bongalon100% (1)

- Bank Reconciliation Statement PDFDocument4 pagesBank Reconciliation Statement PDFNasar IqbalNo ratings yet

- Introduction To Bank ReconciliationDocument11 pagesIntroduction To Bank ReconciliationD K DocumentsNo ratings yet

- Bank Reconciliation Statement NOTESDocument3 pagesBank Reconciliation Statement NOTESvarun rajNo ratings yet

- Bank ReconciliationDocument11 pagesBank ReconciliationKamrul Hasan100% (1)

- About The AuthorDocument11 pagesAbout The AuthorYassi CurtisNo ratings yet

- Bank Reconciliation Statement - Why & How To Prepare The - Statement PDFDocument2 pagesBank Reconciliation Statement - Why & How To Prepare The - Statement PDFAman KodwaniNo ratings yet

- Bank Reconciliation Statement - Why & How To Prepare The - StatementDocument2 pagesBank Reconciliation Statement - Why & How To Prepare The - StatementAman KodwaniNo ratings yet

- Bank Reconciliation StatementDocument6 pagesBank Reconciliation StatementamnatariqshahNo ratings yet

- Acc201 Su2Document5 pagesAcc201 Su2Gwyneth LimNo ratings yet

- LAS Q2 Week3 FABM2Document9 pagesLAS Q2 Week3 FABM2Dash DomingoNo ratings yet

- Bank Reconciliation Statement 2023Document30 pagesBank Reconciliation Statement 2023jsy claudeNo ratings yet

- Basic Reconciliation Statement 3 HoursDocument11 pagesBasic Reconciliation Statement 3 Hoursmarissa casareno almueteNo ratings yet

- VJ Mini ProjectDocument10 pagesVJ Mini ProjectRAKESH VARMA100% (1)

- Las1 Q2 BankreconDocument12 pagesLas1 Q2 BankreconCharlyn CastroNo ratings yet

- Bank Reconciliation Theory & ProblemsDocument9 pagesBank Reconciliation Theory & ProblemsSalvador DapatNo ratings yet

- Lesson 10 Bank Reconciliation StatementDocument22 pagesLesson 10 Bank Reconciliation StatementGelai Batad100% (1)

- Bank ReconciliationDocument6 pagesBank ReconciliationDenishNo ratings yet

- Bank ReconciliationDocument5 pagesBank ReconciliationAngel PadillaNo ratings yet

- Accounting Project: Bank Reconciliation StatementDocument2 pagesAccounting Project: Bank Reconciliation StatementshabanNo ratings yet

- Bank ReconciliationDocument5 pagesBank ReconciliationaizaNo ratings yet

- Physical Protection of Cash BalancesDocument2 pagesPhysical Protection of Cash BalancesJemal SeidNo ratings yet

- CH 3Document25 pagesCH 3yared gebrewoldNo ratings yet

- Lecture File On Bank Reconciliation StatementDocument2 pagesLecture File On Bank Reconciliation StatementRizwan umerNo ratings yet

- Bizmanualz CEO Policies and Procedures Series 2Document20 pagesBizmanualz CEO Policies and Procedures Series 2Ye PhoneNo ratings yet

- Bank Reconciliation StatementDocument10 pagesBank Reconciliation StatementShreeharsh BhaleraoNo ratings yet

- m1 Bank ReconDocument2 pagesm1 Bank ReconRedmond Abalos TejadaNo ratings yet

- FABM2 Module 08 (Q2-W1-2)Document7 pagesFABM2 Module 08 (Q2-W1-2)Christian Zebua0% (2)

- Bank Reconciliation StatementDocument5 pagesBank Reconciliation StatementMuhammad JunaidNo ratings yet

- Bank Reconciliation StatementsDocument13 pagesBank Reconciliation StatementsShreeharsh BhaleraoNo ratings yet

- Bank ReconciliationDocument3 pagesBank ReconciliationBianca Jane GaayonNo ratings yet

- Basic Reconciliation StatementsDocument41 pagesBasic Reconciliation StatementsBeverly EroyNo ratings yet

- Bank Reconciliation StatementDocument3 pagesBank Reconciliation StatementRealGenius (Carl)No ratings yet

- 1.0 Bank Statement Preparation: ProcedureDocument3 pages1.0 Bank Statement Preparation: ProcedureJoseNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- What Is Earnings Per ShareDocument2 pagesWhat Is Earnings Per ShareHsin Wua ChiNo ratings yet

- What Is A Good EPSDocument2 pagesWhat Is A Good EPSHsin Wua ChiNo ratings yet

- What Is The Indirect MethodDocument3 pagesWhat Is The Indirect MethodHsin Wua ChiNo ratings yet

- What Is A Profit and LossDocument4 pagesWhat Is A Profit and LossHsin Wua ChiNo ratings yet

- What Are Cash and Cash EquivalentsDocument3 pagesWhat Are Cash and Cash EquivalentsHsin Wua ChiNo ratings yet

- What Is Management AccountingDocument7 pagesWhat Is Management AccountingHsin Wua ChiNo ratings yet

- Loans Payable DefinedDocument2 pagesLoans Payable DefinedHsin Wua ChiNo ratings yet

- What Is The Earnings Per ShareDocument3 pagesWhat Is The Earnings Per ShareHsin Wua ChiNo ratings yet

- What Is Accounts ReceivableDocument3 pagesWhat Is Accounts ReceivableHsin Wua ChiNo ratings yet

- How To Forecast Financial StatementsDocument8 pagesHow To Forecast Financial StatementsHsin Wua ChiNo ratings yet

- Purposes of Taxation: Taxation, Imposition of Compulsory Levies On Individuals or Entities by GovernmentsDocument12 pagesPurposes of Taxation: Taxation, Imposition of Compulsory Levies On Individuals or Entities by GovernmentsHsin Wua ChiNo ratings yet

- Basic EPS VsDocument3 pagesBasic EPS VsHsin Wua ChiNo ratings yet

- Absorption CostingDocument6 pagesAbsorption CostingHsin Wua ChiNo ratings yet

- What Is A Statement of AccountsDocument5 pagesWhat Is A Statement of AccountsHsin Wua ChiNo ratings yet

- General Terms and Conditions of Delivery and Payment: 1. Conclusion of The ContractDocument3 pagesGeneral Terms and Conditions of Delivery and Payment: 1. Conclusion of The ContractMociran ClaudiuNo ratings yet

- BCG - Global Payments 2022Document40 pagesBCG - Global Payments 2022Anupam GuptaNo ratings yet

- Original: Office of The Provincial ProsecutorDocument19 pagesOriginal: Office of The Provincial ProsecutorGUILLERMO R. DE LEONNo ratings yet

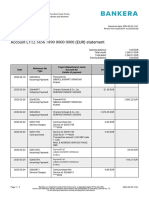

- Bankera StatenebtDocument2 pagesBankera Statenebt9999qyNo ratings yet

- WMS For SAP Business OneDocument9 pagesWMS For SAP Business OneKevin KuttappaNo ratings yet

- Contract IDocument30 pagesContract IHemen zinahbizuNo ratings yet

- General Banking Activities of Sonali BanDocument56 pagesGeneral Banking Activities of Sonali BanKazi Abu SayeedNo ratings yet

- Internship Report On Credit Management of MTBLDocument61 pagesInternship Report On Credit Management of MTBLtanvir100% (1)

- SAP FICO - Summary InfoDocument49 pagesSAP FICO - Summary InfosharwariNo ratings yet

- Say Good Bye To Physical Cash and Welcome To Central Bank Digital CurrencyDocument44 pagesSay Good Bye To Physical Cash and Welcome To Central Bank Digital CurrencyJohn TaskinsoyNo ratings yet

- Disbursement of Pension by Agency BanksDocument25 pagesDisbursement of Pension by Agency BanksnalluriimpNo ratings yet

- Isu Fica TablesDocument5 pagesIsu Fica Tablespasmanica0% (1)

- CISM Certification BrochureDocument15 pagesCISM Certification Brochureyudi6175100% (2)

- Security QuotationDocument7 pagesSecurity QuotationMantesh VhadalureNo ratings yet

- Classification of Electronic PaymentsDocument38 pagesClassification of Electronic PaymentsKenen BhandhaviNo ratings yet

- Terms of Delivery - Sauter Feinmechanik GMBHDocument7 pagesTerms of Delivery - Sauter Feinmechanik GMBHCarloncho LonchoNo ratings yet

- Exit Formalities PDFDocument3 pagesExit Formalities PDFHRNo ratings yet

- Akkreditiv Dokumentarinkassi 4540004 En1Document113 pagesAkkreditiv Dokumentarinkassi 4540004 En1manocher1No ratings yet

- Shubhi RPRDocument82 pagesShubhi RPRSāñyä CháuràsiãNo ratings yet

- Assignment On Presentment Under Negotiable InstrumentsDocument4 pagesAssignment On Presentment Under Negotiable InstrumentsMukul BajajNo ratings yet

- Use Case Fully DressedDocument9 pagesUse Case Fully DressedAli SyedNo ratings yet

- DigestDocument12 pagesDigestAnna Marie DayanghirangNo ratings yet

- Business Proposal Group 7 AssignmentDocument19 pagesBusiness Proposal Group 7 AssignmentTikaNo ratings yet

- Maria Lachica vs. Gregorio AranetaDocument9 pagesMaria Lachica vs. Gregorio AranetaRobert Jayson UyNo ratings yet

- Revision Doc Shashe2023Document40 pagesRevision Doc Shashe2023Oautlwa Seema100% (1)

- Difficulty of Care PaymentsDocument4 pagesDifficulty of Care PaymentsKevin KellyNo ratings yet

- Books For Chefs ReceiptDocument2 pagesBooks For Chefs ReceiptMájer ErikaNo ratings yet