You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Oocl Bill of LadingDocument2 pagesOocl Bill of Ladingyong.longxi100% (2)

- 03 CCI v. QuiñonesDocument2 pages03 CCI v. QuiñonesArielle LaguillesNo ratings yet

- GROUP 4 Evolution of Philippine TaxationDocument17 pagesGROUP 4 Evolution of Philippine TaxationAkiko Grace Tan100% (2)

- Onett Computation SheetDocument1 pageOnett Computation SheetBreahziel ParillaNo ratings yet

- Title 8: Crimes Against Persons Art. 246. ParricideDocument32 pagesTitle 8: Crimes Against Persons Art. 246. ParricideArielle LaguillesNo ratings yet

- Admin Lec - MTDocument2 pagesAdmin Lec - MTArielle LaguillesNo ratings yet

- Who May File Basis of Grant Requirements of RegistrationDocument2 pagesWho May File Basis of Grant Requirements of RegistrationArielle LaguillesNo ratings yet

- Bar Bulletin 7Document20 pagesBar Bulletin 7Alimozaman DiamlaNo ratings yet

- Code of Commerce PHDocument157 pagesCode of Commerce PHM GNo ratings yet

- Republic of The PhilippinesDocument10 pagesRepublic of The PhilippinesArielle LaguillesNo ratings yet

- Revenue Regulations 02-03Document22 pagesRevenue Regulations 02-03Anonymous HIBt2h6z7No ratings yet

- Yap v. CADocument15 pagesYap v. CAArielle LaguillesNo ratings yet

- Monthly Statement: This Month's SummaryDocument8 pagesMonthly Statement: This Month's SummaryshibaNo ratings yet

- Itinerary: Kota KinabaluDocument2 pagesItinerary: Kota KinabaluMuhammad FirdausNo ratings yet

- 05 Activity 1 ActDocument1 page05 Activity 1 ActPalileo KidsNo ratings yet

- Final IEDocument24 pagesFinal IEywmfry29mkNo ratings yet

- HHDocument13 pagesHHLaxminarayanNo ratings yet

- Course Title: Advanced Taxation Course Code: Acfn 522 Credit Hour: 2 Prerequisite: NoneDocument3 pagesCourse Title: Advanced Taxation Course Code: Acfn 522 Credit Hour: 2 Prerequisite: NoneSeifu BekeleNo ratings yet

- OFFER - TO - PURCHASE sAMPLEDocument2 pagesOFFER - TO - PURCHASE sAMPLELeiNo ratings yet

- The Rice Tarification LawDocument3 pagesThe Rice Tarification LawME ValleserNo ratings yet

- Bill of Supply of ElectricityDocument3 pagesBill of Supply of ElectricityBrahmananda TaraiNo ratings yet

- International Business V1.0Document20 pagesInternational Business V1.0Supian Jannatul FirdausNo ratings yet

- Ia ExampleDocument20 pagesIa ExampleChibuzo OkoliNo ratings yet

- Assignment International Economic LawDocument16 pagesAssignment International Economic LawreazNo ratings yet

- 1914 Application For Tax RefundDocument1 page1914 Application For Tax RefundFrancisco TaquioNo ratings yet

- A26Document5 pagesA26Access MaterialsNo ratings yet

- Clearance & Transportation From Port To Jurong Island Unit Charges Sub Total (USD)Document1 pageClearance & Transportation From Port To Jurong Island Unit Charges Sub Total (USD)Jake RixtonNo ratings yet

- Ankit GSTDocument10 pagesAnkit GSTManuj PareekNo ratings yet

- GST Session 38Document20 pagesGST Session 38manjulaNo ratings yet

- February 2024Document1 pageFebruary 2024hiteswarkumarNo ratings yet

- Tax Policy Handbook - Tax Policy HandbookDocument336 pagesTax Policy Handbook - Tax Policy HandbookKiki Azizatur RofiqohNo ratings yet

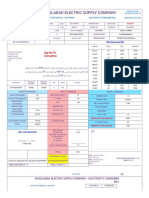

- FESCO ONLINE BILL Faisal Awan PDFDocument2 pagesFESCO ONLINE BILL Faisal Awan PDFWaqas AliNo ratings yet

- Beyonics ERP Configuration Workbook Tax PRODDocument185 pagesBeyonics ERP Configuration Workbook Tax PRODsureshNo ratings yet

- Islamabad Electric Supply Company: Say No To CorruptionDocument2 pagesIslamabad Electric Supply Company: Say No To CorruptionaasfieNo ratings yet

- DownloadDocument1 pageDownloadakshath g sanadiNo ratings yet

- FAQ CustomsDocument5 pagesFAQ Customssandeep_shinuNo ratings yet

- NFCPAR-Auditing Problems: Description Machinery Others NotesDocument1 pageNFCPAR-Auditing Problems: Description Machinery Others NotesSano ManjiroNo ratings yet

- Invoice: Charge DetailsDocument2 pagesInvoice: Charge Detailswa_melianNo ratings yet

- Solar PV Jobs & Value Added in Europe: November 2017Document40 pagesSolar PV Jobs & Value Added in Europe: November 2017roybharggavNo ratings yet