You might also like

- Revenue From Contracts With CustomersDocument21 pagesRevenue From Contracts With Customersnot meNo ratings yet

- Wiley Not-for-Profit GAAP 2017: Interpretation and Application of Generally Accepted Accounting PrinciplesFrom EverandWiley Not-for-Profit GAAP 2017: Interpretation and Application of Generally Accepted Accounting PrinciplesNo ratings yet

- Damodaran, A. - Capital Structure and Financing DecisionsDocument107 pagesDamodaran, A. - Capital Structure and Financing DecisionsJohnathan Fitz KennedyNo ratings yet

- PAS 1 Presentation of Financial StatementsDocument53 pagesPAS 1 Presentation of Financial Statementsjan petosilNo ratings yet

- Week 1 Conceptual Framework For Financial ReportingDocument17 pagesWeek 1 Conceptual Framework For Financial ReportingSHANE NAVARRONo ratings yet

- Ifrs at A Glance IFRS 15 Revenue From Contracts: With CustomersDocument7 pagesIfrs at A Glance IFRS 15 Revenue From Contracts: With CustomersManoj GNo ratings yet

- Applying IFRS 15 - P&DDocument73 pagesApplying IFRS 15 - P&DMuhammad Zaid Sahak100% (1)

- IFRS 16 (Slides) (2022)Document69 pagesIFRS 16 (Slides) (2022)Eben Katewa100% (2)

- IFRS 15 Revenue From: Contracts With CustomersDocument98 pagesIFRS 15 Revenue From: Contracts With CustomersAswathy JejuNo ratings yet

- Take-Out Pizza, Inc Business PlanDocument19 pagesTake-Out Pizza, Inc Business PlanHannae pascua100% (2)

- 93 AvvashyaDocument1 page93 AvvashyaAnonymous rNqW9p3No ratings yet

- Tfrs 15: Ready For The ChallengesDocument19 pagesTfrs 15: Ready For The ChallengesSudharaka PereraNo ratings yet

- AAFR Notes - IFRS 15Document27 pagesAAFR Notes - IFRS 15Waqas100% (1)

- Notes IAS 19Document18 pagesNotes IAS 19Nasir IqbalNo ratings yet

- Updates in FRS IFRS 15Document19 pagesUpdates in FRS IFRS 15Mary Rose MercadoNo ratings yet

- IFRS15 HandoutsDocument16 pagesIFRS15 HandoutsOdon BatjargalNo ratings yet

- Revenue From Contracts With CustomersDocument88 pagesRevenue From Contracts With CustomersAngga PramadaNo ratings yet

- Ias 12 Income TaxesDocument70 pagesIas 12 Income Taxeszulfi100% (1)

- 15 IfrsDocument13 pages15 Ifrssuruth242100% (1)

- Understanding Financial StatementsDocument36 pagesUnderstanding Financial StatementsDurga PrasadNo ratings yet

- Ias 7Document13 pagesIas 7Ajinkya MohadkarNo ratings yet

- Hardware VS SoftwareDocument4 pagesHardware VS SoftwareAira Nhaira MecateNo ratings yet

- Chapter 3-Analyzing and Recording TransactionsDocument49 pagesChapter 3-Analyzing and Recording TransactionsAira Nhaira MecateNo ratings yet

- IFRS Practice Issues Revenue NIIF 15 Sept14Document204 pagesIFRS Practice Issues Revenue NIIF 15 Sept14prof_fids100% (1)

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Document34 pagesReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB Cloyd100% (1)

- 04 RevenueDocument95 pages04 RevenueShehrozSTNo ratings yet

- PWC Loyalty Programs RevrecDocument12 pagesPWC Loyalty Programs RevrecGeebeeNo ratings yet

- IFRS Chapter 14 Financial Assets and LiabilitiesDocument32 pagesIFRS Chapter 14 Financial Assets and LiabilitiesDeLa Vianty AZ-ZahraNo ratings yet

- Solutions Manual: Company Accounting 10eDocument36 pagesSolutions Manual: Company Accounting 10eLSAT PREPAU1100% (1)

- Taxation of Income of Individuals IDocument61 pagesTaxation of Income of Individuals ICaroline Muthoni Mwangi100% (1)

- Kenya Coast National Polytechnic Department of Electrical and Electronics Engineering Diploma in Electrical andDocument78 pagesKenya Coast National Polytechnic Department of Electrical and Electronics Engineering Diploma in Electrical andPascal MuchonjiNo ratings yet

- Presentation of FSDocument2 pagesPresentation of FSTimmy KellyNo ratings yet

- Ifrs 12: Disclosures of Interest in Other EntitiesDocument3 pagesIfrs 12: Disclosures of Interest in Other EntitiesAira Nhaira MecateNo ratings yet

- Ifrs 12: Disclosures of Interest in Other EntitiesDocument3 pagesIfrs 12: Disclosures of Interest in Other EntitiesAira Nhaira MecateNo ratings yet

- Ifrs 16 LeasesDocument33 pagesIfrs 16 Leasesesulawyer2001100% (1)

- Ifrs 5 Assets Held For Sale and Discontinued OperationsDocument45 pagesIfrs 5 Assets Held For Sale and Discontinued OperationstinashekuzangaNo ratings yet

- Consolidation or Business CombinationsDocument17 pagesConsolidation or Business CombinationsTimothy Kawuma100% (1)

- IFRS 16 LeaseDocument64 pagesIFRS 16 LeaseTanvir HossainNo ratings yet

- Ifrs 15: Revenue From Contracts With CustomersDocument46 pagesIfrs 15: Revenue From Contracts With CustomersHace AdisNo ratings yet

- Advanced FA I - Chapter 01, Accounting For Investment in JADocument58 pagesAdvanced FA I - Chapter 01, Accounting For Investment in JAKalkidan G/wahidNo ratings yet

- Diff Bet USGAAP IGAAP IFRSDocument7 pagesDiff Bet USGAAP IGAAP IFRSMichael HillNo ratings yet

- Business Combinations - ASPEDocument3 pagesBusiness Combinations - ASPEShariful HoqueNo ratings yet

- Financial Management - AssignmentDocument9 pagesFinancial Management - Assignmentpeter mulilaNo ratings yet

- ch03 SM Leo 10eDocument72 pagesch03 SM Leo 10ePyae PhyoNo ratings yet

- Shares and Debentures: A Comparison ChartDocument2 pagesShares and Debentures: A Comparison ChartJobin JohnNo ratings yet

- ch05 SM Leo 10eDocument31 pagesch05 SM Leo 10ePyae Phyo100% (2)

- Ind As 109Document26 pagesInd As 109Sandya Gupta100% (1)

- Ias 1Document41 pagesIas 1Ibrahim Arafat ZicoNo ratings yet

- National Exchange Actors Association (NEAA) : Difference Between IFRS & US GAAPDocument10 pagesNational Exchange Actors Association (NEAA) : Difference Between IFRS & US GAAPEshetieNo ratings yet

- Topic 3 - Part 1 - Regulatory Approach of An Accounting TheoryDocument31 pagesTopic 3 - Part 1 - Regulatory Approach of An Accounting TheoryMOHAMMAD ASYRAF NAZRI SAKRINo ratings yet

- LesseeDocument6 pagesLesseeZance JordaanNo ratings yet

- NFRS IiiDocument105 pagesNFRS Iiikaran shahiNo ratings yet

- Ias 7 Statement of Cash Flows: PurposeDocument14 pagesIas 7 Statement of Cash Flows: Purposemusic niNo ratings yet

- Accounting For Government Grants and Disclosure of Government AssistanceDocument18 pagesAccounting For Government Grants and Disclosure of Government AssistanceMaria DevinaNo ratings yet

- ch2 PDFDocument50 pagesch2 PDFAliaa Hosam100% (1)

- Presentation of Financial StatementsDocument40 pagesPresentation of Financial StatementsQuinta NovitaNo ratings yet

- Accounting Adjustments and Constructing The Financial StatementsDocument12 pagesAccounting Adjustments and Constructing The Financial StatementsKwaku DanielNo ratings yet

- Ias - 28 PDFDocument16 pagesIas - 28 PDFANo ratings yet

- IAS 19 Employee Benefits (2021)Document6 pagesIAS 19 Employee Benefits (2021)Tawanda Tatenda Herbert100% (1)

- Format of Cash Flow StatementDocument3 pagesFormat of Cash Flow StatementMoses Fernandes100% (1)

- Ias 24 Related Party DisclosuresDocument13 pagesIas 24 Related Party DisclosuresPallavi PriyaNo ratings yet

- Isre 2400Document21 pagesIsre 2400naveedawan321No ratings yet

- Financial Accounting - TheoriesDocument5 pagesFinancial Accounting - TheoriesKim Cristian MaañoNo ratings yet

- FinQuiz - UsgaapvsifrsDocument12 pagesFinQuiz - UsgaapvsifrsĐạt BùiNo ratings yet

- Workshop On Deferred TaxationDocument21 pagesWorkshop On Deferred TaxationYusuf KhanNo ratings yet

- Acct TutorDocument22 pagesAcct TutorKthln Mntlla100% (1)

- Stratagic Cost-Activity 1Document1 pageStratagic Cost-Activity 1Aira Nhaira MecateNo ratings yet

- Course Name: Course Title: Teachers: Required Text: Course DescriptionDocument5 pagesCourse Name: Course Title: Teachers: Required Text: Course DescriptionAira Nhaira MecateNo ratings yet

- Chapter 5Document47 pagesChapter 5Aira Nhaira MecateNo ratings yet

- CH 5Document44 pagesCH 5Aira Nhaira MecateNo ratings yet

- Decision Making: Relevant Costs and BenefitsDocument39 pagesDecision Making: Relevant Costs and BenefitsAira Nhaira MecateNo ratings yet

- Social Network: Presented By: Supervised byDocument28 pagesSocial Network: Presented By: Supervised byAira Nhaira MecateNo ratings yet

- Consolidated Financial Statements: Ifrs 10Document9 pagesConsolidated Financial Statements: Ifrs 10Aira Nhaira MecateNo ratings yet

- The Role of Financial Information in ContractingDocument25 pagesThe Role of Financial Information in ContractingAira Nhaira MecateNo ratings yet

- Acca Dip Ifrs Book 2019 PDF WWW PDFDocument559 pagesAcca Dip Ifrs Book 2019 PDF WWW PDFAira Nhaira MecateNo ratings yet

- Fundamentalsofabm2statementofcomprehensiveincomeabmspecializedsubject 171210045513Document12 pagesFundamentalsofabm2statementofcomprehensiveincomeabmspecializedsubject 171210045513Aira Nhaira MecateNo ratings yet

- RESPONDUS Training (For Student) Oct 19, 2020 10AMDocument39 pagesRESPONDUS Training (For Student) Oct 19, 2020 10AMAira Nhaira MecateNo ratings yet

- Ifrs 13: Fair Value MeasurementDocument7 pagesIfrs 13: Fair Value MeasurementAira Nhaira MecateNo ratings yet

- Ifrs 14: Regulatory Deferral AccountDocument4 pagesIfrs 14: Regulatory Deferral AccountAira Nhaira MecateNo ratings yet

- Joint Arrangement: Ifrs 11Document3 pagesJoint Arrangement: Ifrs 11Aira Nhaira MecateNo ratings yet

- Ifrs 16Document6 pagesIfrs 16Aira Nhaira MecateNo ratings yet

- CH 10 Special and Combo Journals and Voucher Sys PDFDocument41 pagesCH 10 Special and Combo Journals and Voucher Sys PDFAira Nhaira MecateNo ratings yet

- Ifrs 10: Consolidated Financial InstrumentDocument5 pagesIfrs 10: Consolidated Financial InstrumentAira Nhaira Mecate100% (1)

- Ifrs 9 Financial Instruments: Approach To Macro Hedging. Consequently, The Exception in IAS 39 For A Fair ValueDocument13 pagesIfrs 9 Financial Instruments: Approach To Macro Hedging. Consequently, The Exception in IAS 39 For A Fair ValueAira Nhaira MecateNo ratings yet

- Chapter 4Document52 pagesChapter 4Aira Nhaira MecateNo ratings yet

- Pfrs 2 Share Based Payments: Aira Nhaire C. Mecate, CpaDocument9 pagesPfrs 2 Share Based Payments: Aira Nhaire C. Mecate, CpaAira Nhaira MecateNo ratings yet

- Chapter 2Document37 pagesChapter 2Aira Nhaira MecateNo ratings yet

- Activity-Chapter 3Document1 pageActivity-Chapter 3Aira Nhaira MecateNo ratings yet

- Drivers of Shareholder ValueDocument19 pagesDrivers of Shareholder Valueadbad100% (1)

- A Handbook On Private Equity FundingDocument109 pagesA Handbook On Private Equity FundingLakshmi811No ratings yet

- Company Profile Tan Kai Chean Construction SDN BHD WMDocument24 pagesCompany Profile Tan Kai Chean Construction SDN BHD WMdaniel osmanNo ratings yet

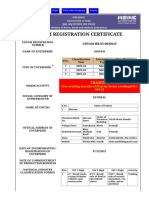

- Print - Udyam Registration CertificateDocument2 pagesPrint - Udyam Registration CertificateshivamNo ratings yet

- Janhavi JaiswalDocument1 pageJanhavi JaiswalSaurabh DubeyNo ratings yet

- Lean Think PDFDocument13 pagesLean Think PDFசரவணகுமார் மாரியப்பன்No ratings yet

- Synopsis Form MS 100Document1 pageSynopsis Form MS 100Neeraj MoghaNo ratings yet

- S & EPM Unit 2Document30 pagesS & EPM Unit 2SaikatPatraNo ratings yet

- 1 s2.0 S0007681316300192 MainDocument7 pages1 s2.0 S0007681316300192 Main罗准恩 Loh Chun EnNo ratings yet

- Past Paper Csec PaperDocument6 pagesPast Paper Csec Paperapi-290917899No ratings yet

- Denmark: Thematic Review of The Transition From Initial Education To Working LifeDocument63 pagesDenmark: Thematic Review of The Transition From Initial Education To Working LifeR PeniNo ratings yet

- Contract Labour Act GistDocument4 pagesContract Labour Act Gistvikas2519No ratings yet

- Invoice 21864732856Document2 pagesInvoice 21864732856ASHISH CHAURASIANo ratings yet

- SMDocument24 pagesSMpriya68kNo ratings yet

- Online Stock Trading Process With The Different Intermediary Institutions As in Practice in Stock Exchange in IndiaDocument6 pagesOnline Stock Trading Process With The Different Intermediary Institutions As in Practice in Stock Exchange in IndiaNirupam NayakNo ratings yet

- New Credit Card Regulations Aid ConsumersDocument1 pageNew Credit Card Regulations Aid ConsumersbmoakNo ratings yet

- The HR Management and Payroll CycleDocument97 pagesThe HR Management and Payroll CycleErwin David SianturiNo ratings yet

- Prof. Dr. Szilágyi József ASPECTS REGARDING THE IMPACT OF TOURISM ON THE ENVIRONMENT IN PRAID BALNEARY RESORTDocument4 pagesProf. Dr. Szilágyi József ASPECTS REGARDING THE IMPACT OF TOURISM ON THE ENVIRONMENT IN PRAID BALNEARY RESORTSzilagyi JozsefNo ratings yet

- Sri Zaheer CVDocument14 pagesSri Zaheer CVKiran ModiNo ratings yet

- IBM Systems Journal PerspectivesDocument24 pagesIBM Systems Journal PerspectivesSmitha MathewNo ratings yet

- IAPMDocument4 pagesIAPMapi-3699305No ratings yet

- Leader Analysis-John MackeyDocument8 pagesLeader Analysis-John Mackeyapi-272623096No ratings yet

- FI RealDocument95 pagesFI RealSohelNo ratings yet

- 18 BibliographyDocument15 pages18 BibliographytouffiqNo ratings yet

- Circular Refund 146 PDFDocument5 pagesCircular Refund 146 PDFradha gNo ratings yet

- OECD - Management Training in SMEsDocument189 pagesOECD - Management Training in SMEsLuis RomeroNo ratings yet