You might also like

- Corporate Finance Case Study WorkingDocument11 pagesCorporate Finance Case Study WorkingS.H. Rustam16% (19)

- Solution Review QuestionsDocument41 pagesSolution Review Questionsying huiNo ratings yet

- Chapter 18 SolutionsDocument38 pagesChapter 18 SolutionsMichael Cox50% (2)

- Paul M. Getty - Tax Deferral Strategies Utilizing The Delaware Statutory TrustDocument184 pagesPaul M. Getty - Tax Deferral Strategies Utilizing The Delaware Statutory TrustwaynesailNo ratings yet

- Taxation Assignment BcaDocument12 pagesTaxation Assignment BcaJeniffer TracyNo ratings yet

- Accounting Department Basic Accounting Works Level Ii: Global College Ambo CampusDocument21 pagesAccounting Department Basic Accounting Works Level Ii: Global College Ambo Campusembiale ayaluNo ratings yet

- General Knowledge of Course Work in Tax LawsDocument5 pagesGeneral Knowledge of Course Work in Tax Lawsiyldyzadf100% (2)

- Accounting Department Basic Accounting Works Level Ii: Global College Ambo CampusDocument20 pagesAccounting Department Basic Accounting Works Level Ii: Global College Ambo Campusembiale ayalu0% (1)

- FABM2 12 Quarter2 Week4Document9 pagesFABM2 12 Quarter2 Week4Princess DuquezaNo ratings yet

- TaxationDocument12 pagesTaxationHaris MalikNo ratings yet

- 18bco6el U3Document11 pages18bco6el U3Teguade ChekolNo ratings yet

- Taxation-for-Development-Narrative-Report Final ReportDocument40 pagesTaxation-for-Development-Narrative-Report Final ReportJackNo ratings yet

- Income Taxation - ModuleDocument15 pagesIncome Taxation - ModuleJuniper Murro BayawaNo ratings yet

- Assignment On: Public Finance For Bangladesh PerspectiveDocument6 pagesAssignment On: Public Finance For Bangladesh PerspectiveNazib UllahNo ratings yet

- Module 1Document9 pagesModule 1ᜊ᜔ᜎᜀᜈ᜔ᜃ᜔ ᜃᜈ᜔ᜊᜐ᜔No ratings yet

- Learning Guide: Accounts and Budget Support Level IiiDocument75 pagesLearning Guide: Accounts and Budget Support Level IiiNigussie BerhanuNo ratings yet

- WK 1-3 in A NutshellDocument2 pagesWK 1-3 in A NutshellexquisiteNo ratings yet

- BAC-103-SG-1 Module 1 TaxationDocument8 pagesBAC-103-SG-1 Module 1 TaxationEmmanuel DalioanNo ratings yet

- Vanshita TaxationPPTDocument13 pagesVanshita TaxationPPTVanshita GuptaNo ratings yet

- Lecture 2 - Income TaxDocument13 pagesLecture 2 - Income TaxMasitala PhiriNo ratings yet

- Informe en Ingles - Planeamiento TributarioDocument11 pagesInforme en Ingles - Planeamiento TributarioHELEN YAZURI DUCLOS LONGOBARDINo ratings yet

- Tax - Planning - and - Managerial - Decisions 4th ChapterDocument16 pagesTax - Planning - and - Managerial - Decisions 4th ChapterVidya VidyaNo ratings yet

- Direct Taxation Code2Document8 pagesDirect Taxation Code2MahekNo ratings yet

- Definition of Tax: Chapter - 1Document12 pagesDefinition of Tax: Chapter - 1Joy NathNo ratings yet

- Issues and Ethics in Finance (Fin657) Assignment 1Document5 pagesIssues and Ethics in Finance (Fin657) Assignment 1ftnsyzwnyNo ratings yet

- The Economic Impacts of Taxation: The Effects of Direct Taxation, The Effects of Indirect TaxationDocument8 pagesThe Economic Impacts of Taxation: The Effects of Direct Taxation, The Effects of Indirect TaxationBiniamNo ratings yet

- Objectives and Principles of Taxation - GeeksforGeeksDocument5 pagesObjectives and Principles of Taxation - GeeksforGeeksLMRP2 LMRP2No ratings yet

- Bac Iv Law Course Taxation IiDocument168 pagesBac Iv Law Course Taxation IiGilbert SanoNo ratings yet

- Emerging Tax TrendsDocument10 pagesEmerging Tax TrendsJesreene Lee-BowraNo ratings yet

- Revenue Administration in The Philippines: Significant Collection Reforms, TRAIN Law, Fiscal Incentives, Excise Tax, and Rice Tariffication LawDocument9 pagesRevenue Administration in The Philippines: Significant Collection Reforms, TRAIN Law, Fiscal Incentives, Excise Tax, and Rice Tariffication LawRegine May AbarquezNo ratings yet

- Thesis TaxationDocument8 pagesThesis Taxationgjgm36vk100% (2)

- Tax Law 0.4Document21 pagesTax Law 0.4Tommy AdemolaNo ratings yet

- Assignment 4B: Research Methods (BCPC 301) BSC Accounting Group 2 (Morning) LEVEL 300 Group 6Document6 pagesAssignment 4B: Research Methods (BCPC 301) BSC Accounting Group 2 (Morning) LEVEL 300 Group 6Dzodzegbe Gabriel1No ratings yet

- Benefits and Impact of The Proposed Tax Reform To The People and The GovernmentDocument12 pagesBenefits and Impact of The Proposed Tax Reform To The People and The GovernmentGretchen CanedoNo ratings yet

- Revenue Administration in The Philippines Significant Collection Reforms, TRAIN Law, Fiscal Incentives, Excise Tax, and Rice Tariffication LawDocument8 pagesRevenue Administration in The Philippines Significant Collection Reforms, TRAIN Law, Fiscal Incentives, Excise Tax, and Rice Tariffication LawKent Elmann CadalinNo ratings yet

- Taxation Law 2021Document60 pagesTaxation Law 2021eayemeyemieNo ratings yet

- Chapter Seven Tax Planning BackgroundDocument9 pagesChapter Seven Tax Planning BackgroundTriila manillaNo ratings yet

- Tax Thesis PDFDocument4 pagesTax Thesis PDFemilyjoneswashington100% (2)

- Income Taxation ReviewerDocument9 pagesIncome Taxation ReviewerAira MabezaNo ratings yet

- The Indian Tax Scenario - Part 1Document5 pagesThe Indian Tax Scenario - Part 1rk_rkaushikNo ratings yet

- Design and Implementation of A Computerized Tax Collection SystemnDocument26 pagesDesign and Implementation of A Computerized Tax Collection SystemnIbrahim Abdulrazaq YahayaNo ratings yet

- Chapter 1 Taxation 2 Onsite Bba3 June To August 2021Document20 pagesChapter 1 Taxation 2 Onsite Bba3 June To August 2021hamidNo ratings yet

- Taxpayer Attitudes Vis-À-Vis The Tax Administration: Differentiate and Classify Taxpayer Behaviors Maria Helena CardozoDocument20 pagesTaxpayer Attitudes Vis-À-Vis The Tax Administration: Differentiate and Classify Taxpayer Behaviors Maria Helena CardozoHosh shNo ratings yet

- Tax Research Paper IdeasDocument4 pagesTax Research Paper Ideashjqojzakf100% (1)

- Public Fiscal Report ScriptDocument8 pagesPublic Fiscal Report ScriptMIS Informal Settler FamiliesNo ratings yet

- A Study On Filing of Return of Tax Deducted at SourceDocument65 pagesA Study On Filing of Return of Tax Deducted at SourceyopoNo ratings yet

- Block - 3FMA - Group4Document28 pagesBlock - 3FMA - Group4jay diazNo ratings yet

- Selam Proposal 2Document14 pagesSelam Proposal 2sebehadinahmed1992No ratings yet

- Taxation CTDocument8 pagesTaxation CTJoy NathNo ratings yet

- WEWAXX RRLDocument23 pagesWEWAXX RRLMERCY LEOLIGAONo ratings yet

- Project 1Document6 pagesProject 1Jagruti KisnaniNo ratings yet

- The Influence of Tax Knowledge, Taxpayer Awareness, And Tax Rates on the Compliance of Individual Taxpayers With Tax Sanctions as a Moderating Variable in E-Commerce Business Activities (Case Study at Online Shop Owner in IndoDocument12 pagesThe Influence of Tax Knowledge, Taxpayer Awareness, And Tax Rates on the Compliance of Individual Taxpayers With Tax Sanctions as a Moderating Variable in E-Commerce Business Activities (Case Study at Online Shop Owner in IndoInternational Journal of Innovative Science and Research Technology100% (1)

- WFH Income TaxationDocument71 pagesWFH Income TaxationnachtandyNo ratings yet

- Ans Taxation 1Document23 pagesAns Taxation 1Priscilla AdebolaNo ratings yet

- Income Taxation - MODULE 1Document13 pagesIncome Taxation - MODULE 1Joe P PokaranNo ratings yet

- Corporate Tax PlanningDocument7 pagesCorporate Tax PlanningimamNo ratings yet

- Escaping True Tax Liability of The Government Amidst PandemicsDocument7 pagesEscaping True Tax Liability of The Government Amidst PandemicsMaria Carla Roan AbelindeNo ratings yet

- Taxpayers' Awareness and Tax Compliance in Local Governments, A CaseDocument9 pagesTaxpayers' Awareness and Tax Compliance in Local Governments, A CaseKIU PUBLICATION AND EXTENSIONNo ratings yet

- Taxation 3Document5 pagesTaxation 3gerry henryNo ratings yet

- Chapter 9Document19 pagesChapter 9Nigussie BerhanuNo ratings yet

- C AE26 MODULE 2 Tax Laws and Tax AdministrationDocument6 pagesC AE26 MODULE 2 Tax Laws and Tax AdministrationBaek hyunNo ratings yet

- TAXATIONDocument33 pagesTAXATIONSsentongo NazilNo ratings yet

- Tax Savings Strategies for Small Businesses: A Comprehensive Guide For 2024From EverandTax Savings Strategies for Small Businesses: A Comprehensive Guide For 2024No ratings yet

- Catalino, Jerome N.Document1 pageCatalino, Jerome N.Jerome CatalinoNo ratings yet

- JeromeDocument2 pagesJeromeJerome CatalinoNo ratings yet

- First Year 2020 2021Document1 pageFirst Year 2020 2021Jerome CatalinoNo ratings yet

- Aefar 3 Intermediate Accounting: College of Business and AccountancyDocument4 pagesAefar 3 Intermediate Accounting: College of Business and AccountancyJerome CatalinoNo ratings yet

- Module 1 AEFAR 4Document13 pagesModule 1 AEFAR 4Jerome CatalinoNo ratings yet

- Ais Reviewer QuestionsDocument47 pagesAis Reviewer QuestionsJerome CatalinoNo ratings yet

- Topics For Final TermsDocument100 pagesTopics For Final TermsJerome CatalinoNo ratings yet

- Catalino, Jerome N. - Column - ChartDocument1 pageCatalino, Jerome N. - Column - ChartJerome CatalinoNo ratings yet

- Filipino Bilang Wikang Pambansa at CMO 20Document31 pagesFilipino Bilang Wikang Pambansa at CMO 20Jerome CatalinoNo ratings yet

- Currency Trade Today - CatalinoDocument1 pageCurrency Trade Today - CatalinoJerome CatalinoNo ratings yet

- Govt. Acctg-Ass#1 - FinalsDocument11 pagesGovt. Acctg-Ass#1 - FinalsJerome CatalinoNo ratings yet

- Conversioncyclesummary - Catalino PartDocument1 pageConversioncyclesummary - Catalino PartJerome CatalinoNo ratings yet

- 2021 GKS-G Available Universities & Fields of Study (English)Document182 pages2021 GKS-G Available Universities & Fields of Study (English)Noverdo Saputra0% (2)

- How Did Enron Disregard Their StakeholdersDocument2 pagesHow Did Enron Disregard Their StakeholdersJerome CatalinoNo ratings yet

- Business Law and RegulationsDocument14 pagesBusiness Law and RegulationsJerome CatalinoNo ratings yet

- SPOILER LAW ON NEGOTIABLE INSTRUMENTS Prelims NCBADocument10 pagesSPOILER LAW ON NEGOTIABLE INSTRUMENTS Prelims NCBAJerome CatalinoNo ratings yet

- Partnership Notes Chapter 1 General ProvDocument6 pagesPartnership Notes Chapter 1 General ProvHazel Jane AbaygarNo ratings yet

- Reflection About Negotiable Instruments LawDocument1 pageReflection About Negotiable Instruments LawJerome CatalinoNo ratings yet

- Conversioncyclesummary - Catalino PartDocument1 pageConversioncyclesummary - Catalino PartJerome CatalinoNo ratings yet

- Inventories MethodDocument7 pagesInventories MethodJerome CatalinoNo ratings yet

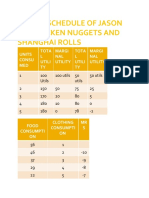

- Utility Schedule of Jason For Chicken Nuggets and Shanghai RollsDocument2 pagesUtility Schedule of Jason For Chicken Nuggets and Shanghai RollsJerome CatalinoNo ratings yet

- Business Law and RegulationsDocument14 pagesBusiness Law and RegulationsJerome CatalinoNo ratings yet

- SPOILER LAW ON NEGOTIABLE INSTRUMENTS Prelims NCBADocument10 pagesSPOILER LAW ON NEGOTIABLE INSTRUMENTS Prelims NCBAJerome CatalinoNo ratings yet

- How The Effect of Deferred Tax Expenses and Tax Planning On Earning Management ?Document6 pagesHow The Effect of Deferred Tax Expenses and Tax Planning On Earning Management ?Nurlita Puji AnggraeniNo ratings yet

- TXVNM 2019 Dec ADocument8 pagesTXVNM 2019 Dec AMinh AnhNo ratings yet

- Tax 1 Notes 2019 20 Part 2 For StudentsDocument109 pagesTax 1 Notes 2019 20 Part 2 For StudentsLegem DiscipulusNo ratings yet

- Bank of America NT & Sa, The Commissioner of Internal RevenueDocument4 pagesBank of America NT & Sa, The Commissioner of Internal RevenueHADTUGINo ratings yet

- Mahalife Gold Brou PDFDocument5 pagesMahalife Gold Brou PDFYogesh2323No ratings yet

- Palanca v. CIR PDFDocument11 pagesPalanca v. CIR PDFnichols greenNo ratings yet

- Syllabus For Taxation Bar Exam 2019Document5 pagesSyllabus For Taxation Bar Exam 2019Vebsie De la CruzNo ratings yet

- Income Taxation Case DigestDocument22 pagesIncome Taxation Case DigestCoyzz de Guzman100% (1)

- Syllabus Bainctax Income Taxationpdf PDF FreeDocument8 pagesSyllabus Bainctax Income Taxationpdf PDF FreePaul Edward GuevarraNo ratings yet

- Review of Income Tax Reporting For Individuals & Corporate TaxpayersDocument159 pagesReview of Income Tax Reporting For Individuals & Corporate TaxpayersRyan Christian BalanquitNo ratings yet

- Module 1. General Principles and Concepts of TaxationDocument214 pagesModule 1. General Principles and Concepts of TaxationCj SernaNo ratings yet

- 1 Taxpayer Identification Number (TIN) 2 RDO Code 3 Contact Number - 4 Registered NameDocument3 pages1 Taxpayer Identification Number (TIN) 2 RDO Code 3 Contact Number - 4 Registered NameRose O. DiscalzoNo ratings yet

- Finals Reviewer Tax 1Document10 pagesFinals Reviewer Tax 1xtinxtin5432No ratings yet

- Taxation EADocument14 pagesTaxation EALhulaan OrdanozoNo ratings yet

- Introduction To Income Tax Integ REVISED 2022 1Document14 pagesIntroduction To Income Tax Integ REVISED 2022 1brr brrNo ratings yet

- Napocor Vs Province of QuezonDocument11 pagesNapocor Vs Province of QuezonJedAdrianNo ratings yet

- Tax6148 Reviewer (Autorecovered)Document37 pagesTax6148 Reviewer (Autorecovered)Regine VegaNo ratings yet

- California Board of Equalization (BOE) Sales/Use Tax ExemptionsDocument50 pagesCalifornia Board of Equalization (BOE) Sales/Use Tax Exemptionswmartin46No ratings yet

- Gutierrez V Collector 101 Phil 743Document1 pageGutierrez V Collector 101 Phil 743Khian JamerNo ratings yet

- 2012 Ateneo LawTaxation Law Summer ReviewerDocument165 pages2012 Ateneo LawTaxation Law Summer ReviewerAllan Ydia89% (9)

- Tax by ItemDocument18 pagesTax by ItemBrooke ReaNo ratings yet

- Tax Treaties Between Philippines and USADocument32 pagesTax Treaties Between Philippines and USACzarina Danielle EsequeNo ratings yet

- 142 150Document7 pages142 150NikkandraNo ratings yet

- BIR Ruling No 455-93 DigestDocument2 pagesBIR Ruling No 455-93 DigestJason CertezaNo ratings yet

- Com. of Internal Revenue vs. United States Lines Company, 5 SCRA 175, No. L-16850 May 30, 1962Document6 pagesCom. of Internal Revenue vs. United States Lines Company, 5 SCRA 175, No. L-16850 May 30, 1962CherNo ratings yet

- Quiz 549Document16 pagesQuiz 549Haris NoonNo ratings yet

- Roxas vs. CTA, 23 SCRA 276Document10 pagesRoxas vs. CTA, 23 SCRA 276Machida AbrahamNo ratings yet