You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5810)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Induction Cap Sealing Machine Performance Qualification Report - Pharmaceutical UpdatesDocument5 pagesInduction Cap Sealing Machine Performance Qualification Report - Pharmaceutical UpdatesChetan Ganesh RautNo ratings yet

- PM-Kisan Samman Nidhi: Your Registration's Payment Done SuccessfullyDocument1 pagePM-Kisan Samman Nidhi: Your Registration's Payment Done SuccessfullyChetan Ganesh RautNo ratings yet

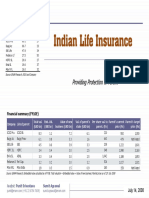

- Life Insurance - Sector ResearchDocument89 pagesLife Insurance - Sector ResearchChetan Ganesh RautNo ratings yet

- Risk Assumption LetterDocument5 pagesRisk Assumption LetterChetan Ganesh RautNo ratings yet

- Bank Privatization in DevelopingDocument39 pagesBank Privatization in DevelopingChetan Ganesh RautNo ratings yet

- Server Error in '/' Application.: The Resource Cannot Be FoundDocument1 pageServer Error in '/' Application.: The Resource Cannot Be FoundChetan Ganesh RautNo ratings yet

- LG Electronics: LG Electronics (Korean: LG 전자, KRX: 066570, LSE: LGLD) is the world'sDocument32 pagesLG Electronics: LG Electronics (Korean: LG 전자, KRX: 066570, LSE: LGLD) is the world'sChetan Ganesh RautNo ratings yet

- Scripwise Price Movement in BANKEX: Bse Bankex 01 January, 2002 1000 23 June, 2003 Free-Float Market CapitalizationDocument6 pagesScripwise Price Movement in BANKEX: Bse Bankex 01 January, 2002 1000 23 June, 2003 Free-Float Market CapitalizationChetan Ganesh RautNo ratings yet

- Our Corporate Profile: CompanyDocument36 pagesOur Corporate Profile: CompanyChetan Ganesh RautNo ratings yet

- How To Make A Deposit in ATM'sDocument7 pagesHow To Make A Deposit in ATM'sChetan Ganesh RautNo ratings yet

- Production and Material ManagementDocument34 pagesProduction and Material ManagementChetan Ganesh RautNo ratings yet

- Soft Drink: How Products Are MadeDocument11 pagesSoft Drink: How Products Are MadeChetan Ganesh RautNo ratings yet

- Our LeadershipDocument13 pagesOur LeadershipChetan Ganesh RautNo ratings yet

- Sara Lee CEO Brenda Barnes Discusses Career BreaksDocument6 pagesSara Lee CEO Brenda Barnes Discusses Career BreaksChetan Ganesh RautNo ratings yet

- Production and Material Management: OnidaDocument22 pagesProduction and Material Management: OnidaChetan Ganesh RautNo ratings yet

- "Production & Material Management": BY Aniket Gajanan Salunkhe ROLL NO:133 DIV: "B" atDocument21 pages"Production & Material Management": BY Aniket Gajanan Salunkhe ROLL NO:133 DIV: "B" atChetan Ganesh RautNo ratings yet

- Turn Over of TataDocument28 pagesTurn Over of TataChetan Ganesh RautNo ratings yet

- Incredible India (South) SandeshDocument9 pagesIncredible India (South) SandeshChetan Ganesh RautNo ratings yet

- Msedcl 150: Transaction ReceiptDocument1 pageMsedcl 150: Transaction ReceiptChetan Ganesh RautNo ratings yet

- Gujarat Cooperative Milk Marketing FederationDocument9 pagesGujarat Cooperative Milk Marketing FederationChetan Ganesh RautNo ratings yet

- LG Expands The CompanyDocument6 pagesLG Expands The CompanyChetan Ganesh RautNo ratings yet

- Guide To Monitoring and Evaluation v1 March2014 PDFDocument60 pagesGuide To Monitoring and Evaluation v1 March2014 PDFMetodio Caetano MonizNo ratings yet

- Agenda: Corangamite ShireDocument225 pagesAgenda: Corangamite ShireKyra GillespieNo ratings yet

- Transportation SystemDocument13 pagesTransportation SystemGurpreet SinghNo ratings yet

- Conclusions - The Role of Project Management in Organisational Sustainab - 2017 - Technology IDocument9 pagesConclusions - The Role of Project Management in Organisational Sustainab - 2017 - Technology IBryan EstacioNo ratings yet

- Green Retailing FinalDocument36 pagesGreen Retailing FinalSandhya DixonNo ratings yet

- An Implemtation GuidelineDocument79 pagesAn Implemtation GuidelineaberraNo ratings yet

- Smart Technologies and Urban Life A Behavioral and Social PerspectiveDocument4 pagesSmart Technologies and Urban Life A Behavioral and Social PerspectiveDeyvid AlmonacidNo ratings yet

- 3-Ecotourism ConceptDocument41 pages3-Ecotourism ConceptMy SpiceNo ratings yet

- Free ElectiveDocument7 pagesFree ElectiveMona Grace100% (2)

- Drempetic 2019Document28 pagesDrempetic 2019Ahmadi AliNo ratings yet

- Eco Tourism - Places and TraditionsDocument93 pagesEco Tourism - Places and TraditionsCognosferaNo ratings yet

- Matos Et Al (2015)Document31 pagesMatos Et Al (2015)Israel Sanches MarcellinoNo ratings yet

- Sports Tourism Literature ReviewDocument8 pagesSports Tourism Literature Reviewea5zjs6a100% (1)

- Environment Final EssayDocument6 pagesEnvironment Final EssayShaila ShamNo ratings yet

- Sustainable DevelopmentDocument2 pagesSustainable Developmentapi-241242931100% (1)

- The Three Star Approach To WASH in SchoolsDocument11 pagesThe Three Star Approach To WASH in SchoolsGlobal Public-Private Partnership for Handwashing100% (4)

- Environmental Ethics in The Perception of Urban PlannersDocument18 pagesEnvironmental Ethics in The Perception of Urban PlannersJhakash Boy TripathiNo ratings yet

- Johannesburg Roads Agency SOC LimitedDocument38 pagesJohannesburg Roads Agency SOC LimitedMirash Moossa ValiyakathNo ratings yet

- Contemporary WorldDocument4 pagesContemporary WorldCarlos Levi BarawelNo ratings yet

- Sustainable Construction Materials and TechnologiesDocument821 pagesSustainable Construction Materials and TechnologiesAhmed Zidan100% (6)

- Joshi y Rahman (2019)Document9 pagesJoshi y Rahman (2019)Felipe CorreaNo ratings yet

- Exploring Socio-Cultural Impacts of Ecotourism in The Annapurna Conservation Area, NepalDocument21 pagesExploring Socio-Cultural Impacts of Ecotourism in The Annapurna Conservation Area, Nepalsakshi meherNo ratings yet

- R - IGCSE Resources - Global Perspectives 0457 Individual ReportDocument57 pagesR - IGCSE Resources - Global Perspectives 0457 Individual Reportaadxt11No ratings yet

- Environmental Sustainability Proposal: International Youth Earth SummitDocument2 pagesEnvironmental Sustainability Proposal: International Youth Earth SummitMohammed A. AbuShanabNo ratings yet

- 2012-08 Canterbury Landscape Character Biodiversity Appraisal DraftDocument222 pages2012-08 Canterbury Landscape Character Biodiversity Appraisal DraftHerneBayMattersNo ratings yet

- CHN Ms Palmer PsycheDocument102 pagesCHN Ms Palmer PsycheJL V. Adriano100% (1)

- Bambu Sebagai Alternatif Penerapan Material Ekologis: Potensi Dan TantangannyaDocument10 pagesBambu Sebagai Alternatif Penerapan Material Ekologis: Potensi Dan Tantangannyaaldi9aNo ratings yet

- Cooperative Economies in A Global AgeDocument193 pagesCooperative Economies in A Global AgestefansiebelNo ratings yet

- Sustainable Precast Concrete Design, Production and ConstructionDocument4 pagesSustainable Precast Concrete Design, Production and ConstructionAfsin Ecer.No ratings yet

- DDU Strategic Plan FinalDocument118 pagesDDU Strategic Plan FinalGirmaye Haile100% (2)