You might also like

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- IT Module No. 7: Introduction To Regular Income TaxDocument13 pagesIT Module No. 7: Introduction To Regular Income TaxjakeNo ratings yet

- IT-11GA (New Form) For Private Service Tax Year 2020-21 19 Oct 20 - PDFDocument16 pagesIT-11GA (New Form) For Private Service Tax Year 2020-21 19 Oct 20 - PDFMASUD RANANo ratings yet

- Project Proposal Wajira Dhabaa Paper FinalggDocument36 pagesProject Proposal Wajira Dhabaa Paper FinalggTesfaye DegefaNo ratings yet

- Co-Ownership, Estates and TrustsDocument13 pagesCo-Ownership, Estates and TrustsRoronoa Zoro100% (1)

- Regular Income TaxDocument11 pagesRegular Income Taxwhat ever100% (4)

- Income Taxation Lecture Notes.6.TAX On CORPORATIONSDocument10 pagesIncome Taxation Lecture Notes.6.TAX On CORPORATIONSeinel dcNo ratings yet

- Module 3 Variable Costing As Management Tool-1Document4 pagesModule 3 Variable Costing As Management Tool-1Haika ContiNo ratings yet

- 03 Vat Subject TransactionsDocument5 pages03 Vat Subject TransactionsJaneLayugCabacungan100% (1)

- Chapter 7: Introduction To Regular Income Tax: 1. General in CoverageDocument19 pagesChapter 7: Introduction To Regular Income Tax: 1. General in CoverageJulie Mae Caling Malit33% (3)

- GCRO Module 120 - 07 Computation of TaxDocument34 pagesGCRO Module 120 - 07 Computation of TaxKezia100% (1)

- Introduction To Regular Income TaxDocument44 pagesIntroduction To Regular Income TaxGabriel Trinidad Soniel0% (1)

- CorporationDocument23 pagesCorporationLiyana Chua50% (2)

- Chapter 15 BDocument3 pagesChapter 15 BErinNo ratings yet

- Assessments and ReassessmentsDocument31 pagesAssessments and ReassessmentsRam PrasadNo ratings yet

- Format For Computation of Income Under Income Tax ActDocument3 pagesFormat For Computation of Income Under Income Tax ActAakash67% (3)

- Chapter 3Document8 pagesChapter 3Eunice SerneoNo ratings yet

- Chapter 7 Regular Income TaxationDocument4 pagesChapter 7 Regular Income TaxationMary Jane Pabroa100% (1)

- TaxaoneDocument20 pagesTaxaonedianne ballonNo ratings yet

- Provisional Tax - SlidesDocument17 pagesProvisional Tax - SlidesZwivhuya MaimelaNo ratings yet

- Computed Using Classification and Globalization Rule: or Business Income Such As Passive IncomeDocument10 pagesComputed Using Classification and Globalization Rule: or Business Income Such As Passive IncomelcNo ratings yet

- Saint John School: Learning Kit 1 - Fundamentals of Accountancy, Business and Management 2Document7 pagesSaint John School: Learning Kit 1 - Fundamentals of Accountancy, Business and Management 2Cynthia SantosNo ratings yet

- The Regular Income TaxDocument4 pagesThe Regular Income TaxJean Diane JoveloNo ratings yet

- Pro Forma Process For Tax Computation CompensationDocument2 pagesPro Forma Process For Tax Computation Compensationjessamaepinas5No ratings yet

- Taxable IncomeDocument18 pagesTaxable Incomerav danoNo ratings yet

- Taxation of Individuals: Step 1 Step 2: Step 3Document39 pagesTaxation of Individuals: Step 1 Step 2: Step 3Pratyanshi MehtaNo ratings yet

- Mat and Amt: Objective of Levying MATDocument16 pagesMat and Amt: Objective of Levying MATaNo ratings yet

- Allowable DeductionsDocument17 pagesAllowable DeductionsShanelle SilmaroNo ratings yet

- Mepa Unit 5Document18 pagesMepa Unit 5Tharaka RoopeshNo ratings yet

- Ho 09 - Computation of Individual Taxpayers Income Tax PDFDocument14 pagesHo 09 - Computation of Individual Taxpayers Income Tax PDFArah Opalec100% (1)

- Notes Income Taxation IndividualDocument10 pagesNotes Income Taxation IndividualTriscia QuiñonesNo ratings yet

- Chapter 13 - DeductionsDocument5 pagesChapter 13 - DeductionsDeviane CalabriaNo ratings yet

- Income Tax of IndividualsDocument27 pagesIncome Tax of IndividualsChristmaNo ratings yet

- Banking Company - Porfit and Loss Account FormatDocument8 pagesBanking Company - Porfit and Loss Account Formatgeetha sri100% (1)

- 10.mat and AmtDocument17 pages10.mat and AmtShailendra SainwalNo ratings yet

- Computation of TaxesDocument34 pagesComputation of TaxesIrish D DagmilNo ratings yet

- INCOTAX - 06 - Individuals, Estates, TrustsDocument6 pagesINCOTAX - 06 - Individuals, Estates, TrustsJainder de GuzmanNo ratings yet

- 16 - Income TaxDocument44 pages16 - Income Taxayushagarwal23No ratings yet

- Chapter 4-Mcit, Iaet, GitDocument22 pagesChapter 4-Mcit, Iaet, GitJayvee FelipeNo ratings yet

- AMT - Know About Alternative Minimum Tax Applicability, Exemptions, Credits & MoreDocument8 pagesAMT - Know About Alternative Minimum Tax Applicability, Exemptions, Credits & MoreRudrin DasNo ratings yet

- Clarification On The Amendment To Section 16 of Companies Income Tax Act in Relation To Taxation of Insurance CompaniesDocument7 pagesClarification On The Amendment To Section 16 of Companies Income Tax Act in Relation To Taxation of Insurance CompaniesOluwagbenga OgunsakinNo ratings yet

- CPTR 5 Optional Corporate Tax On Branch Profit Remittance 1Document5 pagesCPTR 5 Optional Corporate Tax On Branch Profit Remittance 1NaikNo ratings yet

- Gross Income TaxationDocument8 pagesGross Income TaxationJenelyn FloresNo ratings yet

- Computation of Income Tax Due and PayableDocument14 pagesComputation of Income Tax Due and Payablealia fauniNo ratings yet

- Introduction To TaxDocument18 pagesIntroduction To TaxVenniah MusundaNo ratings yet

- Morales Taxation Topic 5 Allowable DeductionsDocument33 pagesMorales Taxation Topic 5 Allowable DeductionsMary Joice Delos santosNo ratings yet

- Copy Individual Income TaxDocument10 pagesCopy Individual Income TaxMari Louis Noriell MejiaNo ratings yet

- Technical Article 07 Corporate TaxDocument3 pagesTechnical Article 07 Corporate TaxTawanda Tatenda HerbertNo ratings yet

- RMC 35-2011 IaetDocument2 pagesRMC 35-2011 IaetDyan de la FuenteNo ratings yet

- Mat and Amt: Objective of Levying MATDocument17 pagesMat and Amt: Objective of Levying MATSamuel AnthrayoseNo ratings yet

- Individual Income Taxation-ComputationDocument27 pagesIndividual Income Taxation-ComputationeuniNo ratings yet

- Ra 9337Document23 pagesRa 9337cheska_abigail950No ratings yet

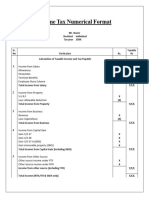

- Summary Sheet NumericalDocument2 pagesSummary Sheet NumericalSamina HyderNo ratings yet

- Income Tax Concept of Income 1 Discussion:: Sec. 31. Taxable Income Defined. - The Term 'Taxable Income' Means TheDocument6 pagesIncome Tax Concept of Income 1 Discussion:: Sec. 31. Taxable Income Defined. - The Term 'Taxable Income' Means TheApay GrajoNo ratings yet

- Income Tax in India - Wikipedia, The Free EncyclopediaDocument10 pagesIncome Tax in India - Wikipedia, The Free EncyclopediakandurimaruthiNo ratings yet

- VAT Part 1Document9 pagesVAT Part 1Sittee Raihana Talicop BansilNo ratings yet

- The Study Is of The Expressions Found in The Income-Tax Act, 1961Document27 pagesThe Study Is of The Expressions Found in The Income-Tax Act, 1961samrockmeNo ratings yet

- Mat and Amt: Objective of Levying MATDocument17 pagesMat and Amt: Objective of Levying MATNitin ChoudharyNo ratings yet

- Income Tax of IndividualsDocument4 pagesIncome Tax of IndividualsBhabhing EnriquezNo ratings yet

- It Goi Note On Mat and AmtDocument17 pagesIt Goi Note On Mat and AmtKapil AroraNo ratings yet

- Definations: Income TaxDocument6 pagesDefinations: Income Taxsini rayNo ratings yet

- PDF - Learn More - House Property Peoblems and SolutionsDocument4 pagesPDF - Learn More - House Property Peoblems and Solutionsbsc slpNo ratings yet

- PDF - Learn More - Capital Gains - Problems and SolutionsDocument5 pagesPDF - Learn More - Capital Gains - Problems and Solutionsbsc slpNo ratings yet

- Electrolux Convection Microwave EMB2527BA User Manual PDFDocument20 pagesElectrolux Convection Microwave EMB2527BA User Manual PDFbsc slpNo ratings yet

- Electrolux Convection Microwave EMB2527BA User Manual PDFDocument20 pagesElectrolux Convection Microwave EMB2527BA User Manual PDFbsc slpNo ratings yet

- Finals - II. Deductions & ExemptionsDocument13 pagesFinals - II. Deductions & ExemptionsJovince Daño DoceNo ratings yet

- TUGAS 2 B.Inggris NiagaDocument2 pagesTUGAS 2 B.Inggris NiagaYulia RossilawatiNo ratings yet

- Preparing and Using Financial StatementsDocument33 pagesPreparing and Using Financial StatementsMuhammad Imran50% (2)

- HW 1Document15 pagesHW 1ANo ratings yet

- 1 M3a2-Accounting-25Document4 pages1 M3a2-Accounting-25Henny DeWillisNo ratings yet

- Joint ArrangementsDocument22 pagesJoint ArrangementsJhoanNo ratings yet

- 2-Fisher vs. TrinidadDocument8 pages2-Fisher vs. TrinidadRadel LlagasNo ratings yet

- Accouc Payroll CH3Document15 pagesAccouc Payroll CH3Nimona Beyene50% (2)

- Southern Luzon Drug vs. DSWD - Senior Citizen Discount Exercise of Police Power - Separate Opn - LeonenDocument18 pagesSouthern Luzon Drug vs. DSWD - Senior Citizen Discount Exercise of Police Power - Separate Opn - LeonenhlcameroNo ratings yet

- MICROECONOMICS Gobind Kumar JhaDocument59 pagesMICROECONOMICS Gobind Kumar Jhabinay chaudharyNo ratings yet

- Swot of AbmlDocument24 pagesSwot of AbmlGaurav SinghNo ratings yet

- Problems and Prospects of The Rural Women Entrepreneurs in IndiaDocument10 pagesProblems and Prospects of The Rural Women Entrepreneurs in IndiamarishhhNo ratings yet

- Feasibility Study Bakery FinalDocument13 pagesFeasibility Study Bakery FinalVina Niña Mae ApiadoNo ratings yet

- Vietnam Food & Beverage IndustryDocument55 pagesVietnam Food & Beverage Industrybuihongmai171090No ratings yet

- Television Set Assembly PlantDocument28 pagesTelevision Set Assembly PlantAbebeNo ratings yet

- Kelompok 5 Akl 2Document4 pagesKelompok 5 Akl 2Khansa AuliaNo ratings yet

- Chapter Six: Fundamental Concepts of Macroeconomics and Macroeconomic ProblemsDocument33 pagesChapter Six: Fundamental Concepts of Macroeconomics and Macroeconomic ProblemsOromay EliasNo ratings yet

- Erika Eunice Silva - Piecewise Function-1st PTDocument6 pagesErika Eunice Silva - Piecewise Function-1st PTerika eunice silvaNo ratings yet

- Chapter Seven: Basic Accounting Principles & Budgeting FundamentalsDocument35 pagesChapter Seven: Basic Accounting Principles & Budgeting FundamentalsbelaynehNo ratings yet

- COMPANY/FINANCE/PROFIT AND LOSS/175/Nestle IndiaDocument1 pageCOMPANY/FINANCE/PROFIT AND LOSS/175/Nestle IndiabhuvaneshkmrsNo ratings yet

- COst of Capital - BringhamDocument16 pagesCOst of Capital - BringhamHammna AshrafNo ratings yet

- Managing in A Global Economy Demystifying International Macroeconomics 2nd Edition Marthinsen 128505542X Solution ManualDocument8 pagesManaging in A Global Economy Demystifying International Macroeconomics 2nd Edition Marthinsen 128505542X Solution Manualleigh100% (29)

- Cmeef KPK FormDocument11 pagesCmeef KPK FormShahid KhanNo ratings yet

- Income From House PropertyDocument28 pagesIncome From House PropertyAshish SharmaNo ratings yet

- 2022 - Taxation in SpainDocument26 pages2022 - Taxation in SpainManny ManNo ratings yet

- Meeting 1Document9 pagesMeeting 1erlina nurliaNo ratings yet

- Answer Key Chapter 4Document2 pagesAnswer Key Chapter 4Emily TanNo ratings yet