You might also like

- Unit IiDocument20 pagesUnit IinamianNo ratings yet

- Pdfcaie Igcse Accounting 0452 Theory v2 PDFDocument24 pagesPdfcaie Igcse Accounting 0452 Theory v2 PDFrumaisaaltaf287No ratings yet

- Journal: Double Entry System of AccountingDocument17 pagesJournal: Double Entry System of AccountingBole ShubhamNo ratings yet

- Caie Igcse Accounting 0452 Theory v2Document24 pagesCaie Igcse Accounting 0452 Theory v2Haaris UsmanNo ratings yet

- StudyGuideChap08 PDFDocument27 pagesStudyGuideChap08 PDFNarjes DehkordiNo ratings yet

- Double-Entry Book-KeepingDocument6 pagesDouble-Entry Book-KeepingFarman AfzalNo ratings yet

- Caie Igcse Accounting 0452 Theory v3Document23 pagesCaie Igcse Accounting 0452 Theory v3tarzan.shakilNo ratings yet

- IGSCE Accounts Theory NotesDocument3 pagesIGSCE Accounts Theory NotesThe Xplorer In Me CooksNo ratings yet

- Module 1 AccDocument6 pagesModule 1 Acc21-035 Dhanjit RoymedhiNo ratings yet

- AccountingDocument24 pagesAccountingnour mohammedNo ratings yet

- Book KeepingDocument11 pagesBook KeepingRocket SinghNo ratings yet

- IGCSE Grade 9th & 10thDocument6 pagesIGCSE Grade 9th & 10thThe Xplorer In Me CooksNo ratings yet

- Theory NotesDocument7 pagesTheory NotesThe Xplorer In Me CooksNo ratings yet

- Accountancy Class 11th T.S. Grewal Book PDF New Edition (Part 2) Pdf. by HELPING HAND ?? PDFDocument128 pagesAccountancy Class 11th T.S. Grewal Book PDF New Edition (Part 2) Pdf. by HELPING HAND ?? PDFGehna Jain80% (40)

- Chapter 2 Rules of Debit and Credit and General LedgerDocument3 pagesChapter 2 Rules of Debit and Credit and General LedgerDaniel Tan KtNo ratings yet

- What Is Accounting???Document15 pagesWhat Is Accounting???Modassar NazarNo ratings yet

- BAF3ME Unit 3 - Activity 7 - Summative Assessment Quiz NotesDocument9 pagesBAF3ME Unit 3 - Activity 7 - Summative Assessment Quiz NotesHibbah OwaisNo ratings yet

- Acctg Overview - 012023Document6 pagesAcctg Overview - 012023Czamille Rivera GonzagaNo ratings yet

- Control AccountsDocument3 pagesControl AccountsLilian OngNo ratings yet

- Accounting at A GlanceDocument14 pagesAccounting at A GlanceNiyaz AhamedNo ratings yet

- ACC525 Week 1 AssignmentDocument3 pagesACC525 Week 1 AssignmentRung'Minoz KittiNo ratings yet

- Chapter Two - Fundamentals of AcctDocument14 pagesChapter Two - Fundamentals of AcctGedionNo ratings yet

- Grdae 9 - Ems - Financial Literacy SummaryDocument17 pagesGrdae 9 - Ems - Financial Literacy SummarykotolograceNo ratings yet

- 1339 1Document9 pages1339 1Noaman AkbarNo ratings yet

- Session 2 - Income Statement and Transaction AnalysisDocument42 pagesSession 2 - Income Statement and Transaction Analysishieucaiminh155No ratings yet

- ACC406 - Topic 4a - Principle of Double Entry and Books of AccountDocument23 pagesACC406 - Topic 4a - Principle of Double Entry and Books of AccountCarol LeslyNo ratings yet

- Topic 1 - The Accounting EquationDocument10 pagesTopic 1 - The Accounting Equationgabriellemorgan714No ratings yet

- Book Keeping 101 by Tom Clendon 1688995453Document6 pagesBook Keeping 101 by Tom Clendon 1688995453amayarNo ratings yet

- As Level Accounting NotesDocument77 pagesAs Level Accounting NotesRoHan ChooramunNo ratings yet

- AccountsDocument4 pagesAccountsPranshu BansalNo ratings yet

- Accounting: Assets Liabilities + Equity A L + EDocument4 pagesAccounting: Assets Liabilities + Equity A L + EJohn LeeNo ratings yet

- Financial Accounting and ReportingDocument12 pagesFinancial Accounting and ReportingDiane GarciaNo ratings yet

- Chapter - 2 @2003Document14 pagesChapter - 2 @2003Tariku KolchaNo ratings yet

- Accounting Equation and Double Entry BookkeepingDocument29 pagesAccounting Equation and Double Entry BookkeepingArvin ToraldeNo ratings yet

- Pointers To Review: FABM 2: Recording Phase: Answer KeyDocument9 pagesPointers To Review: FABM 2: Recording Phase: Answer KeyMaria Janelle BlanzaNo ratings yet

- As Level Accounting Notes.Document75 pagesAs Level Accounting Notes.SameerNo ratings yet

- Module 2 - The Use of Double-Entry and Accounting SystemsDocument22 pagesModule 2 - The Use of Double-Entry and Accounting SystemsJewel Philip50% (2)

- Lecture 5 - Books of Accounts and Double Entry SystemDocument7 pagesLecture 5 - Books of Accounts and Double Entry SystemmallarilecarNo ratings yet

- Chapter 4 AccountingDocument22 pagesChapter 4 AccountingChan Man SeongNo ratings yet

- Fra Notes JyotiDocument62 pagesFra Notes JyotiJyotirmayee NaikNo ratings yet

- Final AccountsDocument7 pagesFinal AccountsSushank Kumar 7278No ratings yet

- Accounting: Assets Liabilities + Equity A L + EDocument4 pagesAccounting: Assets Liabilities + Equity A L + EjermaineNo ratings yet

- Journal To Final AccountsDocument38 pagesJournal To Final Accountsguptagaurav131166100% (5)

- 8 Debtors, Creditors, and Promisory Notes UDDocument41 pages8 Debtors, Creditors, and Promisory Notes UDERICK MLINGWANo ratings yet

- Basic Financial Statements NotesDocument6 pagesBasic Financial Statements NotesNNo ratings yet

- 8 Debtors, Creditors, and Promisory NotesDocument30 pages8 Debtors, Creditors, and Promisory NotesERICK MLINGWANo ratings yet

- Ch7 英文(已G)Document93 pagesCh7 英文(已G)9dwdbthjtjNo ratings yet

- Accounts, Accountants and AccrualsDocument20 pagesAccounts, Accountants and Accrualsjcmail999446No ratings yet

- Chart of Accounts GuideDocument4 pagesChart of Accounts GuidekathNo ratings yet

- AccountingDocument2 pagesAccountingazazelrallosNo ratings yet

- PYQ FlashcardsDocument48 pagesPYQ Flashcardskala1975No ratings yet

- VU Accounting Lesson 24Document6 pagesVU Accounting Lesson 24ranawaseemNo ratings yet

- Green Beige Group Project PresentationDocument16 pagesGreen Beige Group Project PresentationwelchNo ratings yet

- Chapter 4-Handout (Double Entry System)Document7 pagesChapter 4-Handout (Double Entry System)jepsyut100% (1)

- AccountingDocument22 pagesAccountingjosephsamuelmojoNo ratings yet

- Full Download Accounting Volume 1 Canadian 9th Edition Horngren Solutions ManualDocument12 pagesFull Download Accounting Volume 1 Canadian 9th Edition Horngren Solutions Manualkotelamalbec6100% (19)

- Financial AccountingDocument53 pagesFinancial Accountingnikhil100% (1)

- The Barrington Guide to Property Management Accounting: The Definitive Guide for Property Owners, Managers, Accountants, and Bookkeepers to ThriveFrom EverandThe Barrington Guide to Property Management Accounting: The Definitive Guide for Property Owners, Managers, Accountants, and Bookkeepers to ThriveNo ratings yet

- POB - Lesson 5 - Cottage Industries Sizes of Organizations and MISDocument4 pagesPOB - Lesson 5 - Cottage Industries Sizes of Organizations and MISAudrey RolandNo ratings yet

- Lect. 5 Easements - Characteristics and AquisitionDocument23 pagesLect. 5 Easements - Characteristics and AquisitionAudrey RolandNo ratings yet

- POB - Lesson 2 - Money Scarcity SpecializationDocument2 pagesPOB - Lesson 2 - Money Scarcity SpecializationAudrey RolandNo ratings yet

- Lect. 2.3.1 ConsiderationDocument11 pagesLect. 2.3.1 ConsiderationAudrey RolandNo ratings yet

- Queries: TH TH TH THDocument2 pagesQueries: TH TH TH THAudrey RolandNo ratings yet

- Digital Media BackgroundDocument5 pagesDigital Media BackgroundAudrey RolandNo ratings yet

- Digital MediaDocument9 pagesDigital MediaAudrey RolandNo ratings yet

- Information Technology Internal AssessmentDocument17 pagesInformation Technology Internal AssessmentAudrey RolandNo ratings yet

- Savings Plan WorksheetDocument4 pagesSavings Plan Worksheetnuri90No ratings yet

- 100 Most Important Banking Awareness QuestionsDocument9 pages100 Most Important Banking Awareness QuestionsKing VegetaNo ratings yet

- Accounts and TaxationDocument3 pagesAccounts and TaxationnishantsmeNo ratings yet

- Chapter-3 Managing Cash and Marketable SecuritiesDocument9 pagesChapter-3 Managing Cash and Marketable SecuritiesSintu TalefeNo ratings yet

- Job Analysis NIB BankDocument15 pagesJob Analysis NIB BankKiran ReshiNo ratings yet

- 21st Century in BangaldeshDocument7 pages21st Century in BangaldeshRifat KhanNo ratings yet

- The Rothschilds' Family Fortune - Financial TimesDocument3 pagesThe Rothschilds' Family Fortune - Financial TimeshahulaniNo ratings yet

- Chap, 009Document17 pagesChap, 009Salman KhalidNo ratings yet

- PPMI-Form No. 1-Application For Membership - Thrift & Rural Bank - Revised102418Document3 pagesPPMI-Form No. 1-Application For Membership - Thrift & Rural Bank - Revised102418Reniel Dollete Taborada100% (2)

- Chapter - I: Profile of TMB Tamilnad Mercantile Bank Limited (TMB) Is A Bank Headquartered atDocument29 pagesChapter - I: Profile of TMB Tamilnad Mercantile Bank Limited (TMB) Is A Bank Headquartered atPoojaNo ratings yet

- August 19Document48 pagesAugust 19fijitimescanadaNo ratings yet

- Project Proposal-West Timawa PO With Complete AnnexesDocument29 pagesProject Proposal-West Timawa PO With Complete AnnexesStewart Paul TorreNo ratings yet

- Case Hamilton Jacobs JPYDocument3 pagesCase Hamilton Jacobs JPYAndré Felipe de MedeirosNo ratings yet

- Non-DBT Customers - Aadhaar Consent - Version - August19Document1 pageNon-DBT Customers - Aadhaar Consent - Version - August19sauravNo ratings yet

- Transferring Funds : International Personal BankDocument4 pagesTransferring Funds : International Personal BankGarbo BentleyNo ratings yet

- Investment in Allied UndertakingsDocument4 pagesInvestment in Allied Undertakingssop_pologNo ratings yet

- 1067 1001 File PDFDocument256 pages1067 1001 File PDFpriya.sunderNo ratings yet

- Ash and Cash EquivalentsDocument2 pagesAsh and Cash EquivalentsYassi CurtisNo ratings yet

- Fair Practices Code: ObjectiveDocument16 pagesFair Practices Code: ObjectiveBADRI VENKATESHNo ratings yet

- 25 Truths About MoneyDocument3 pages25 Truths About MoneyBarney CordovaNo ratings yet

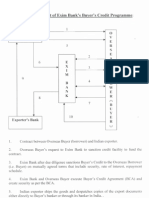

- Procedural Flow Chart of Exim BankDocument3 pagesProcedural Flow Chart of Exim BankMilan DasNo ratings yet

- Trece Martires: Turns Into Virtual CityDocument3 pagesTrece Martires: Turns Into Virtual CityAbby YambaoNo ratings yet

- Beginners Guide To CryptocurrenciesDocument10 pagesBeginners Guide To CryptocurrenciesAmb Patrick OghateNo ratings yet

- International Management Journals: International Journal of Applied Public-Private PartnershipsDocument11 pagesInternational Management Journals: International Journal of Applied Public-Private Partnershipsarup_halderNo ratings yet

- Artikel Ilmiah PDFDocument15 pagesArtikel Ilmiah PDFelseNo ratings yet

- Soneri Bank LTDDocument33 pagesSoneri Bank LTDishfaq_allahNo ratings yet

- Firestone vs. Ca GR No. 113236Document2 pagesFirestone vs. Ca GR No. 113236REA RAMIREZNo ratings yet

- Final Law Report 1876-1879Document11 pagesFinal Law Report 1876-1879Rae Anne ÜNo ratings yet

- Banamex 2015Document144 pagesBanamex 2015Arpita KapoorNo ratings yet