You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Anger Discussion QuestionsDocument27 pagesAnger Discussion QuestionsSteven RichardsNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Costing NotebookDocument123 pagesCosting NotebookremarkuNo ratings yet

- RJ ThemesDocument47 pagesRJ Themesapi-249583009No ratings yet

- Uy V. Judge JavellanaDocument3 pagesUy V. Judge JavellanaBianca PalomaNo ratings yet

- Cases VoidableDocument25 pagesCases VoidablechrisNo ratings yet

- 2.7 Turbines For Hydroelectric Power PDFDocument26 pages2.7 Turbines For Hydroelectric Power PDFEnrique FloresNo ratings yet

- AprilDocument51 pagesAprilcườngNo ratings yet

- HUL - Snippet Analysis 2Document7 pagesHUL - Snippet Analysis 2snithisha chandranNo ratings yet

- Bank ValuationDocument88 pagesBank Valuationsnithisha chandranNo ratings yet

- Banking - (Pages 1 To 25)Document25 pagesBanking - (Pages 1 To 25)snithisha chandranNo ratings yet

- 89029art of QuestioningDocument6 pages89029art of Questioningsnithisha chandranNo ratings yet

- TASK-20 Valuation of Banks Part-2Document4 pagesTASK-20 Valuation of Banks Part-2snithisha chandranNo ratings yet

- Valuation of Bank (Part-3) - Task 21Document10 pagesValuation of Bank (Part-3) - Task 21snithisha chandranNo ratings yet

- Task 17: Analysis of Non Performing Assets of Bank Non Performing AssetDocument8 pagesTask 17: Analysis of Non Performing Assets of Bank Non Performing Assetsnithisha chandranNo ratings yet

- Valuation of Bank (Part-2) - Task-20Document6 pagesValuation of Bank (Part-2) - Task-20snithisha chandranNo ratings yet

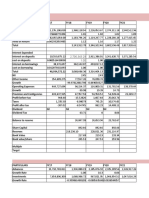

- Interest Earned: Valuation Sheet of State Bank of India Income StatementDocument9 pagesInterest Earned: Valuation Sheet of State Bank of India Income Statementsnithisha chandranNo ratings yet

- Hedge Your Weatlh: Life ParametersDocument3 pagesHedge Your Weatlh: Life Parameterssnithisha chandranNo ratings yet

- 110620-Top Management Org Structure, SBI Corporate CentreDocument1 page110620-Top Management Org Structure, SBI Corporate Centresnithisha chandranNo ratings yet

- Task-7 Crude Oil: Impact of Crude Oil Fluctuations in Different Sectors Refiners and Oil Marketing CompaniesDocument17 pagesTask-7 Crude Oil: Impact of Crude Oil Fluctuations in Different Sectors Refiners and Oil Marketing Companiessnithisha chandranNo ratings yet

- Getting Things DoneDocument20 pagesGetting Things Donesnithisha chandranNo ratings yet

- HUL - Snippet Analysis 2Document7 pagesHUL - Snippet Analysis 2snithisha chandranNo ratings yet

- Covid 19 PCR Test Results - JTH LAB - 2021.10.28 - For THJaffnaDocument2 pagesCovid 19 PCR Test Results - JTH LAB - 2021.10.28 - For THJaffnaArshathNo ratings yet

- Philodemus - On Property ManagementDocument174 pagesPhilodemus - On Property ManagementAndres Azael Mendoza ChavezNo ratings yet

- Executive Trainee - 2013: Registration SlipDocument1 pageExecutive Trainee - 2013: Registration Slipamanpreet2190No ratings yet

- HRM Practices Contribute To Organizational InnovationDocument11 pagesHRM Practices Contribute To Organizational InnovationSasi PreethamNo ratings yet

- Economic Solution All ChapterDocument212 pagesEconomic Solution All ChapterSHUKLA TUSHARNo ratings yet

- Community Stakeholder Engagement Within A NonDocument6 pagesCommunity Stakeholder Engagement Within A NonAmar narayanNo ratings yet

- Half Knowledge of Everything Including Islam Is Dangerous !Document5 pagesHalf Knowledge of Everything Including Islam Is Dangerous !ismailp996262No ratings yet

- Petitioners Vs Vs Respondents: Second DivisionDocument11 pagesPetitioners Vs Vs Respondents: Second DivisionVener MargalloNo ratings yet

- Part A: 1. Differentiate Among Financial Accounting, Cost Accounting & Management AccountingDocument5 pagesPart A: 1. Differentiate Among Financial Accounting, Cost Accounting & Management AccountingSisir AhammedNo ratings yet

- 41136bos30870 SM Ref NoRestrictionDocument2 pages41136bos30870 SM Ref NoRestrictionvikash1905No ratings yet

- Dr. Jeffrey Kamlet Litigation Documents 10.18Document172 pagesDr. Jeffrey Kamlet Litigation Documents 10.18Phil AmmannNo ratings yet

- Ignao v. IACDocument9 pagesIgnao v. IACChristopher Martin GunsatNo ratings yet

- CJUE Multil Terms All Languages IATE ListDocument2,572 pagesCJUE Multil Terms All Languages IATE Listmlebourg63No ratings yet

- Pension Portion: Hints For Calculation of Pension "1 Step"Document55 pagesPension Portion: Hints For Calculation of Pension "1 Step"Willeuge100% (1)

- Kumagai Ishii-Kuntz Eds. Family Violence Japan Life Course 2016Document190 pagesKumagai Ishii-Kuntz Eds. Family Violence Japan Life Course 2016Beatrix Zsuzsanna HandaNo ratings yet

- Exercícios Inglês Discurso Direto IndiretoDocument2 pagesExercícios Inglês Discurso Direto IndiretoMário André De Oliveira CruzNo ratings yet

- 80219a 02Document32 pages80219a 02Indaia RufinoNo ratings yet

- United States v. Rao Gollapudi, 130 F.3d 66, 3rd Cir. (1997)Document16 pagesUnited States v. Rao Gollapudi, 130 F.3d 66, 3rd Cir. (1997)Scribd Government DocsNo ratings yet

- Comfort Women: Slave of Destiny: Maria Rosa HensonDocument5 pagesComfort Women: Slave of Destiny: Maria Rosa HensonEmmarlone96No ratings yet

- Accounting For Labor Part 1Document17 pagesAccounting For Labor Part 1Ghillian Mae GuiangNo ratings yet

- Atomic Iran by Mike Evans Chapter 17 PreviewDocument14 pagesAtomic Iran by Mike Evans Chapter 17 PreviewDr. Michael D. Evans100% (1)

- Water Hacks Aff - Gonzaga 2021Document206 pagesWater Hacks Aff - Gonzaga 2021Easton LargentNo ratings yet

- Traffic Problem in Chittagong Metropolitan CityDocument2 pagesTraffic Problem in Chittagong Metropolitan CityRahmanNo ratings yet