0% found this document useful (0 votes)

164 views13 pages4.1.1 Accounting Entries For Expenditure (General Ledger)

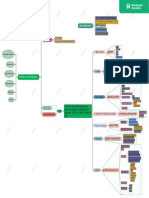

The document outlines accounting entries for various types of transactions including expenditures, receipts, payroll, grants, loans, and recoveries. For expenditures, entries are made to record the initial charge to an expenditure head and subsequent clearing from the bank. Receipts are recorded by crediting revenue and debits to the bank. Payroll transactions debit gross salary and credit net amounts. Loan receipts are initially recorded as capital receipts with an offsetting liability, and repayments debit the liability and credit the bank.

Uploaded by

Official SAGCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

164 views13 pages4.1.1 Accounting Entries For Expenditure (General Ledger)

The document outlines accounting entries for various types of transactions including expenditures, receipts, payroll, grants, loans, and recoveries. For expenditures, entries are made to record the initial charge to an expenditure head and subsequent clearing from the bank. Receipts are recorded by crediting revenue and debits to the bank. Payroll transactions debit gross salary and credit net amounts. Loan receipts are initially recorded as capital receipts with an offsetting liability, and repayments debit the liability and credit the bank.

Uploaded by

Official SAGCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd