You might also like

- Project Report On Compensation ManagementDocument38 pagesProject Report On Compensation Managementmohit87% (15)

- Components of Pay StructureDocument6 pagesComponents of Pay StructurePrajakta Gokhale100% (2)

- ESOPDocument40 pagesESOPsimonebandrawala9No ratings yet

- Controlling Payroll Cost - Critical Disciplines for Club ProfitabilityFrom EverandControlling Payroll Cost - Critical Disciplines for Club ProfitabilityNo ratings yet

- Compensation Management MBA HRDocument67 pagesCompensation Management MBA HRAmardeep Upadhyay88% (25)

- SHEQ Monthly Report SummaryDocument17 pagesSHEQ Monthly Report SummaryArif NugrohoNo ratings yet

- Meaning of Wage/Compensation Payment:: Chapter-1 Compensation Management-IDocument22 pagesMeaning of Wage/Compensation Payment:: Chapter-1 Compensation Management-IRamit GuptaNo ratings yet

- Blockchain Financial Services ReportDocument57 pagesBlockchain Financial Services ReportPunita KumariNo ratings yet

- Wage and Salary AdministrationDocument34 pagesWage and Salary AdministrationSAVI100% (1)

- UK-eCommerce ListDocument16 pagesUK-eCommerce ListSheel ThakkarNo ratings yet

- Accounting of Labour and Cost ControlDocument70 pagesAccounting of Labour and Cost Controlaishwarya raikarNo ratings yet

- LABOR STANDARDS REVIEW MCQDocument5 pagesLABOR STANDARDS REVIEW MCQLiza MelgarNo ratings yet

- Compensation ManagementDocument27 pagesCompensation ManagementsachinmanjuNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Project Report On Compensation ManagementDocument37 pagesProject Report On Compensation Managementgmp_0755% (11)

- The Ultimate Guide to Achieving ISO 27001 CertificationDocument21 pagesThe Ultimate Guide to Achieving ISO 27001 CertificationTaraj O KNo ratings yet

- Wages and IncentivesDocument16 pagesWages and IncentivesMariya Johny100% (1)

- Tapas y Cuellos BericapDocument2 pagesTapas y Cuellos BericapMelvin Mateo Rodriguez100% (1)

- Labour CostDocument24 pagesLabour CostStiloflexindia EnterpriseNo ratings yet

- Factors Affecting CompensationDocument6 pagesFactors Affecting CompensationAlem AyahuNo ratings yet

- Labor Cost Computation & Control Presentation 4Document82 pagesLabor Cost Computation & Control Presentation 4NayanNo ratings yet

- UNIT 5 RemunerationDocument23 pagesUNIT 5 RemunerationRahul kumarNo ratings yet

- Acts Influence Compensation StructureDocument6 pagesActs Influence Compensation StructureCyrus FernzNo ratings yet

- CMAA Semester 2 PresentationDocument35 pagesCMAA Semester 2 PresentationGaurav PoddarNo ratings yet

- How compensation management improves employee performanceDocument60 pagesHow compensation management improves employee performanceUday GowdaNo ratings yet

- Explain Compensation As A Retention Strategy. Describe The Significant Compensation Issues Compensation As Retention StrategyDocument8 pagesExplain Compensation As A Retention Strategy. Describe The Significant Compensation Issues Compensation As Retention StrategyBhanu PratapNo ratings yet

- Project Report On Compensation ManagementDocument37 pagesProject Report On Compensation ManagementMadhu SunkapakaNo ratings yet

- Projrct Report Compensation BenchmarkingDocument37 pagesProjrct Report Compensation BenchmarkingPoornima GargNo ratings yet

- Salary & WagesDocument39 pagesSalary & Wagesvaishnavi patilNo ratings yet

- Group 4 HRMDocument18 pagesGroup 4 HRMMary Jean C. DedilNo ratings yet

- Compensation PlanningDocument26 pagesCompensation PlanningSaloni AgrawalNo ratings yet

- Components of CompensationDocument9 pagesComponents of Compensationshruti.shindeNo ratings yet

- Wage Components ExplainedDocument34 pagesWage Components ExplainedBharathRam100% (1)

- IncentivesDocument10 pagesIncentivesjgkonnullyNo ratings yet

- Unit-IV HRMDocument10 pagesUnit-IV HRMSaini Lakhvindar singhNo ratings yet

- MU0006 (2 CREDITS) Set 1 Compensation BenefitsDocument8 pagesMU0006 (2 CREDITS) Set 1 Compensation BenefitsafreenmineNo ratings yet

- Bba Unit 4 HRMDocument22 pagesBba Unit 4 HRMKeshav KatariaNo ratings yet

- Mu0015 Compensation and BenefitsDocument9 pagesMu0015 Compensation and BenefitsSandeep Kanyal100% (1)

- MGL Comp - Intro-4Document24 pagesMGL Comp - Intro-4Ehtesam khanNo ratings yet

- Compensation: Beliefs About The Worth of Jobs: Individual CharacteristicsDocument6 pagesCompensation: Beliefs About The Worth of Jobs: Individual CharacteristicsHimanshu ShrivastavaNo ratings yet

- Compensation MGMT - 1708000028Document9 pagesCompensation MGMT - 1708000028Abhishek Kumar SahayNo ratings yet

- Compensation and BenefitsDocument9 pagesCompensation and BenefitsKaran ChandhokNo ratings yet

- Module 9. CompensationDocument8 pagesModule 9. Compensationriyanshi.natani398No ratings yet

- AttachmentDocument34 pagesAttachmentSiraj ShaikhNo ratings yet

- Compensation ManagementDocument12 pagesCompensation Managementprakhyasingh1905No ratings yet

- Assignment On LaborDocument33 pagesAssignment On LaborlivabaniNo ratings yet

- CH 7Document5 pagesCH 7hailu mekonenNo ratings yet

- Chapter 1 - INTRODUCTION TO COMPENSATIONDocument11 pagesChapter 1 - INTRODUCTION TO COMPENSATIONFrancis GumawaNo ratings yet

- Remuneration 1Document17 pagesRemuneration 1Pavithra JNo ratings yet

- Two Tiered Wage SystemDocument6 pagesTwo Tiered Wage Systemrhozel2010No ratings yet

- Employment Laws in India Relating to Wages, Minimum Wages and Bonus PaymentsDocument63 pagesEmployment Laws in India Relating to Wages, Minimum Wages and Bonus PaymentsSAUMYA DWIVEDI FPM Student, Jaipuria LucknowNo ratings yet

- Compensation and Salary AdministrationDocument4 pagesCompensation and Salary AdministrationabmbithaNo ratings yet

- Labor Cost Computation & Control Presentation 4Document82 pagesLabor Cost Computation & Control Presentation 4fatemaNo ratings yet

- Obhrm Unit-5-1Document17 pagesObhrm Unit-5-1Abhishek KunchalaNo ratings yet

- Compensation Management HRMDocument31 pagesCompensation Management HRMVivek Singh0% (1)

- National wage policy objectives, concepts of labour marketDocument12 pagesNational wage policy objectives, concepts of labour marketAshish KhadakhadeNo ratings yet

- Compensation MGT 260214Document224 pagesCompensation MGT 260214Thiru VenkatNo ratings yet

- Principles of WagesDocument10 pagesPrinciples of WagesDaniel PeterNo ratings yet

- Wage Admin Concepts, Factors, Levels & MethodsDocument28 pagesWage Admin Concepts, Factors, Levels & MethodsNeeru SharmaNo ratings yet

- Unit 4 Contextual FactorsDocument5 pagesUnit 4 Contextual FactorsRicha TripathiNo ratings yet

- Wages and Salary Unit 1Document13 pagesWages and Salary Unit 1पशुपति नाथNo ratings yet

- HRM Unit 4Document44 pagesHRM Unit 4Manigandan .RNo ratings yet

- CompensationDocument6 pagesCompensationkanikasinghalNo ratings yet

- The Incentive Plan for Efficiency in Government Operations: A Program to Eliminate Government DeficitsFrom EverandThe Incentive Plan for Efficiency in Government Operations: A Program to Eliminate Government DeficitsNo ratings yet

- Textbook of Urgent Care Management: Chapter 12, Pro Forma Financial StatementsFrom EverandTextbook of Urgent Care Management: Chapter 12, Pro Forma Financial StatementsNo ratings yet

- Summer Training ProjectDocument8 pagesSummer Training ProjectPunita KumariNo ratings yet

- Courses Offered for EntrepreneursDocument4 pagesCourses Offered for EntrepreneursPunita KumariNo ratings yet

- Analysis of Vision of Top 5 CompaniesDocument6 pagesAnalysis of Vision of Top 5 CompaniesPunita KumariNo ratings yet

- Customers' Perception of Digital Payments in IndiaDocument61 pagesCustomers' Perception of Digital Payments in IndiaPunita Kumari100% (1)

- Four main types of data analytics: predictive, prescriptive, diagnostic and descriptiveDocument4 pagesFour main types of data analytics: predictive, prescriptive, diagnostic and descriptivePunita KumariNo ratings yet

- Four main types of data analytics: predictive, prescriptive, diagnostic and descriptiveDocument4 pagesFour main types of data analytics: predictive, prescriptive, diagnostic and descriptivePunita KumariNo ratings yet

- Open Culture.: No. Courses Offered Duration Free Skill You Will Gain. 1Document1 pageOpen Culture.: No. Courses Offered Duration Free Skill You Will Gain. 1Punita KumariNo ratings yet

- Exam Assigment of CCMDocument12 pagesExam Assigment of CCMPunita KumariNo ratings yet

- Exam Assigment of IFMDocument9 pagesExam Assigment of IFMPunita KumariNo ratings yet

- IBS Selection Process GuideDocument24 pagesIBS Selection Process GuideApna time aayegaNo ratings yet

- Accomplishment February 2019Document8 pagesAccomplishment February 2019saphire donsolNo ratings yet

- Ijcs 127281Document34 pagesIjcs 127281Faten bakloutiNo ratings yet

- Technical Letter StructureDocument33 pagesTechnical Letter Structuresayed Tamir janNo ratings yet

- Samir Samuel Site Engineer 2021Document2 pagesSamir Samuel Site Engineer 2021Samir SamuelNo ratings yet

- Rajasthan Technical University, Kota: Syllabus IV Year-VIII Semester: B. Tech. (Civil Engineering)Document1 pageRajasthan Technical University, Kota: Syllabus IV Year-VIII Semester: B. Tech. (Civil Engineering)Bhavy Kumar JainNo ratings yet

- Sustainbook PDFDocument225 pagesSustainbook PDFjNo ratings yet

- Mark 261-PROMOTIONS OPPORTUNITY ANALYSIS - CHP 5Document11 pagesMark 261-PROMOTIONS OPPORTUNITY ANALYSIS - CHP 5priyapamNo ratings yet

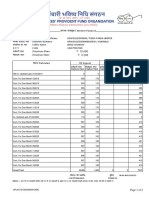

- Member Passbook DetailsDocument2 pagesMember Passbook DetailsNaveen SinghNo ratings yet

- Explore and Explain:: Grade 12 - EntrepreneurshipDocument12 pagesExplore and Explain:: Grade 12 - EntrepreneurshipLatifah EmamNo ratings yet

- RBI's Vital Role in Regulating India's Economy and Financial SystemDocument2 pagesRBI's Vital Role in Regulating India's Economy and Financial SystemSimran hreraNo ratings yet

- M&ADocument27 pagesM&ArinacharNo ratings yet

- Chapter 7 (Basic Elements of Planning and Decision Making)Document21 pagesChapter 7 (Basic Elements of Planning and Decision Making)babon.eshaNo ratings yet

- FMCSA Rules on Marking Commercial Motor VehiclesDocument3 pagesFMCSA Rules on Marking Commercial Motor VehiclesfreeNo ratings yet

- Accounting Information System: Midterm ExamDocument35 pagesAccounting Information System: Midterm ExamHeidi OpadaNo ratings yet

- Business 5511 Group Project 0007ADocument15 pagesBusiness 5511 Group Project 0007ALinh NguyenNo ratings yet

- 3-in-1 Stylus Business PlanDocument24 pages3-in-1 Stylus Business Planalliahdane valenciaNo ratings yet

- Vinamilk Yogurt Report 2019: CTCP Sữa Việt Nam (Vinamilk)Document24 pagesVinamilk Yogurt Report 2019: CTCP Sữa Việt Nam (Vinamilk)Nguyễn Hoàng TrườngNo ratings yet

- Pre ProductionDocument2 pagesPre ProductionRajrupa SahaNo ratings yet

- P7112bgm-Catalogueb2010 0811 en A4 FullDocument810 pagesP7112bgm-Catalogueb2010 0811 en A4 FullShri ShriNo ratings yet

- Urban MarketplaceDocument20 pagesUrban MarketplaceMae LafortezaNo ratings yet

- MSc Sales & Marketing Statement of PurposeDocument1 pageMSc Sales & Marketing Statement of PurposeDaud LawrenceNo ratings yet

- Spare Parts List: R900772317 R961001350 Drawing: Material NumberDocument6 pagesSpare Parts List: R900772317 R961001350 Drawing: Material NumberbuddhivasuNo ratings yet

- ONLINE QUIZ Pledge Morgage and AntichresisDocument2 pagesONLINE QUIZ Pledge Morgage and AntichresisSophia PerezNo ratings yet

- The Following Information Is Available To Reconcile Style Co SDocument2 pagesThe Following Information Is Available To Reconcile Style Co SAmit PandeyNo ratings yet