You might also like

- Clear Your Credit Card DebtDocument48 pagesClear Your Credit Card DebtYash ANo ratings yet

- KV Barkuhi student's debenture projectDocument19 pagesKV Barkuhi student's debenture projectMuffin RageNo ratings yet

- Company LawDocument19 pagesCompany LawAakankshaNo ratings yet

- Deb An TuresDocument10 pagesDeb An TuresWeNo ratings yet

- Corporate Law 5th SemDocument20 pagesCorporate Law 5th SemAayushiNo ratings yet

- 12 AccountancyDocument7 pages12 AccountancyAlim AbbasNo ratings yet

- First Horizon Advisors Client Investment GuideDocument20 pagesFirst Horizon Advisors Client Investment Guideporter siminourNo ratings yet

- Debentures and Debt MarketsDocument31 pagesDebentures and Debt MarketsVimal Singh100% (1)

- Capstone Project NBFC Loan Foreclosure PredictionDocument48 pagesCapstone Project NBFC Loan Foreclosure PredictionAbhay PoddarNo ratings yet

- Debentures - ProjectDocument30 pagesDebentures - ProjectCsAnkita Agarwal50% (16)

- Capital Markets BasicsDocument26 pagesCapital Markets BasicsudNo ratings yet

- Aadya Tiwary Shreya SharmaDocument19 pagesAadya Tiwary Shreya SharmaChandan TiwariNo ratings yet

- Aadya Tiwary Shreya SharmaDocument19 pagesAadya Tiwary Shreya SharmaChandan TiwariNo ratings yet

- Debentures ProjectDocument28 pagesDebentures ProjectMT RA100% (1)

- Debenture Types and IssuesDocument17 pagesDebenture Types and IssuesPriyaranjan Singh100% (1)

- Mba Assignment 2Document17 pagesMba Assignment 2Joanne LeoNo ratings yet

- NPAs and SecuritizationDocument18 pagesNPAs and SecuritizationVikku AgarwalNo ratings yet

- Accounting for Debentures Issue and RedemptionDocument31 pagesAccounting for Debentures Issue and RedemptionchaityashahNo ratings yet

- Unit IIDocument7 pagesUnit IIchithralegaNo ratings yet

- Business Finance Project - DebenturesDocument16 pagesBusiness Finance Project - DebenturesMuhammad TalhaNo ratings yet

- Project Report On "Debentures"Document14 pagesProject Report On "Debentures"Imran Shaikh88% (8)

- Types of DebenturesDocument3 pagesTypes of DebenturesTerfa JesseNo ratings yet

- Financial Glossary of TermsDocument30 pagesFinancial Glossary of TermsRishabh RanaNo ratings yet

- Tarika Sikarwar - A Handbook of Case Studies in Finance (2017, Cambridge Scholars Publishing) - libgen.li (1)Document147 pagesTarika Sikarwar - A Handbook of Case Studies in Finance (2017, Cambridge Scholars Publishing) - libgen.li (1)Zain ul AbidinNo ratings yet

- Company Law AssignmentDocument6 pagesCompany Law AssignmentKanishkaNo ratings yet

- CBSE Quick Revision Notes and Chapter Summary: Book Recommended: WarningDocument8 pagesCBSE Quick Revision Notes and Chapter Summary: Book Recommended: WarningiisjafferNo ratings yet

- Unit - 8 CLDocument3 pagesUnit - 8 CLKanishkaNo ratings yet

- Issue of Debentures Redemption of Debentures UnderwrtingDocument47 pagesIssue of Debentures Redemption of Debentures UnderwrtingRAMA ChauhanNo ratings yet

- Accounting Treatment of Debenture Issue and RedemptionDocument96 pagesAccounting Treatment of Debenture Issue and Redemptionsgangwar2005sgNo ratings yet

- Final SLP Accounting For ReceivablesDocument26 pagesFinal SLP Accounting For ReceivablesLovely Joy SantiagoNo ratings yet

- Issue of Debentures Redemption of Debentures UnderwrtingDocument47 pagesIssue of Debentures Redemption of Debentures UnderwrtingKeshav PantNo ratings yet

- Definition DebenturesDocument8 pagesDefinition DebenturesDipanjan DasNo ratings yet

- Monitor Receivables ComplianceDocument45 pagesMonitor Receivables CompliancenigusNo ratings yet

- Different Types of Debentures and Their UseDocument10 pagesDifferent Types of Debentures and Their UseMansangat Singh KohliNo ratings yet

- Understanding Debentures and the Role of a Debenture TrusteeDocument11 pagesUnderstanding Debentures and the Role of a Debenture TrusteeShalvin SharmaNo ratings yet

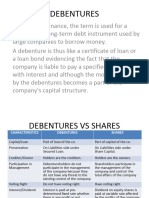

- debenture_vs_shares-2Document19 pagesdebenture_vs_shares-2nemewep527No ratings yet

- Summaries of 3-5 Chapters: ZUBAIR AHMED (16BBA-012)Document10 pagesSummaries of 3-5 Chapters: ZUBAIR AHMED (16BBA-012)NoorNo ratings yet

- Fin533 Group AssignmentDocument23 pagesFin533 Group AssignmentAzwin YusoffNo ratings yet

- Financial Fitness Report: Nishant ChauhanDocument7 pagesFinancial Fitness Report: Nishant ChauhanNishantNo ratings yet

- Corporate Finance CompendiumDocument21 pagesCorporate Finance CompendiumAman SharanNo ratings yet

- Bond Fundamentals AssignDocument12 pagesBond Fundamentals AssignkennethNo ratings yet

- Student declaration analysisDocument17 pagesStudent declaration analysisHuda waseemNo ratings yet

- Redemption of Debentures.Document11 pagesRedemption of Debentures.Basil shibuNo ratings yet

- SecuritizationDocument5 pagesSecuritizationAnand MishraNo ratings yet

- Definition and Type DebenturesDocument4 pagesDefinition and Type DebenturesAshutosh KumarNo ratings yet

- DebenturesDocument6 pagesDebenturesUmesh GaikwadNo ratings yet

- 2017 Understanding Credit BookDocument28 pages2017 Understanding Credit BookDinu MariusNo ratings yet

- Mohit's Company Law ProjectDocument18 pagesMohit's Company Law ProjectMohit MunjaalNo ratings yet

- Definition, Type and Issue of Debentures: New Inspiron™ 14R LaptopsDocument3 pagesDefinition, Type and Issue of Debentures: New Inspiron™ 14R LaptopsGause KaniNo ratings yet

- Issue and Redemption of DebenturesDocument22 pagesIssue and Redemption of DebenturesVikas MandloiNo ratings yet

- Interim Report I032Document16 pagesInterim Report I032Surbhi SejraNo ratings yet

- Effects of Rising NPAs on BanksDocument27 pagesEffects of Rising NPAs on BanksNavneet NandaNo ratings yet

- CAPITAL MARKET (VAC) - AssignmentDocument9 pagesCAPITAL MARKET (VAC) - Assignment22mba221No ratings yet

- 19 DebenturesDocument2 pages19 DebenturesTEXTILIONSNo ratings yet

- Various Types of Corporate BondsDocument7 pagesVarious Types of Corporate BondsAbdul LatifNo ratings yet

- ChapterDocument78 pagesChaptershaannivasNo ratings yet

- 062 - Prem Prakash Poddar - FACA CIA AssignmentDocument4 pages062 - Prem Prakash Poddar - FACA CIA AssignmentPrem Prakash PoddarNo ratings yet

- DebentureDocument9 pagesDebenturedrsurendrakumarNo ratings yet

- Digital Finance - Unit 4Document5 pagesDigital Finance - Unit 4NAVYA JUNEJA 2023323No ratings yet

- Unit 4: Business Models For Digital Financial Services: DR, Anand Patil, Christ University, Bangalore, IndiaDocument7 pagesUnit 4: Business Models For Digital Financial Services: DR, Anand Patil, Christ University, Bangalore, IndiaNAVYA JUNEJA 2023323No ratings yet

- Digital Finance - UNIT 2Document8 pagesDigital Finance - UNIT 2NAVYA JUNEJA 2023323No ratings yet

- Digital Finance - UNIT 3Document8 pagesDigital Finance - UNIT 3NAVYA JUNEJA 2023323No ratings yet

- Digital Finance - UNIT 1Document7 pagesDigital Finance - UNIT 1NAVYA JUNEJA 2023323No ratings yet

- Commissioner of Internal Revenue Vs Tours SpecialistsDocument10 pagesCommissioner of Internal Revenue Vs Tours SpecialistsVincent OngNo ratings yet

- Yara Annual Report 2015Document168 pagesYara Annual Report 2015RudraNo ratings yet

- Philippine First Insurance CompanyDocument2 pagesPhilippine First Insurance CompanyRoda May DiñoNo ratings yet

- Cfap 5 2019 PKDocument194 pagesCfap 5 2019 PKSummar FarooqNo ratings yet

- Azure SOX Guidance PDFDocument7 pagesAzure SOX Guidance PDFajsosaNo ratings yet

- Vietnamese Law On Credit InstitutionDocument101 pagesVietnamese Law On Credit InstitutionBosin NhiNo ratings yet

- Overview of Business ProcessesDocument9 pagesOverview of Business ProcessesNoha KhaledNo ratings yet

- 2dd3c613 1670283438180Document8 pages2dd3c613 1670283438180Kyla Gacula NatividadNo ratings yet

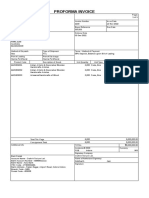

- Craft-A-Torium Proforma InvoiceDocument1 pageCraft-A-Torium Proforma InvoiceSiddharth JainNo ratings yet

- MONZO Crowdfunding-Prospectus-2018Document203 pagesMONZO Crowdfunding-Prospectus-2018Kiran DhootNo ratings yet

- Mahler 3F MAH-13SSM-E Sample 12-10-12Document235 pagesMahler 3F MAH-13SSM-E Sample 12-10-12callistaNo ratings yet

- Brazil Accounting Tax Processes v1 PDFDocument163 pagesBrazil Accounting Tax Processes v1 PDFGustavo GonçalvesNo ratings yet

- Contract of Loan: WitnessethDocument2 pagesContract of Loan: WitnessethJameson UyNo ratings yet

- CIR vs CA on VAT liability of non-profit service providerDocument2 pagesCIR vs CA on VAT liability of non-profit service providerEllen Glae DaquipilNo ratings yet

- Get Payslip by Offset PDFDocument1 pageGet Payslip by Offset PDFanon_535796411100% (1)

- GLEF 4020 International Banking and Financial Regulation 2020-21 Term 2 Course OutlineDocument3 pagesGLEF 4020 International Banking and Financial Regulation 2020-21 Term 2 Course Outlinewang wendaNo ratings yet

- Jakel Capital Welcomes Datuk Ami Moris's Appointment As Director at Cypark ResourcesDocument3 pagesJakel Capital Welcomes Datuk Ami Moris's Appointment As Director at Cypark ResourcesHan JinNo ratings yet

- The Rise and Evolution of the Global CorporationDocument14 pagesThe Rise and Evolution of the Global Corporationmeca DURAN50% (4)

- The Importance of Cost ControlDocument36 pagesThe Importance of Cost ControlfajarNo ratings yet

- Solved Carlos Opens A Dry Cleaning Store During The Year He PDFDocument1 pageSolved Carlos Opens A Dry Cleaning Store During The Year He PDFAnbu jaromiaNo ratings yet

- EM5 UNIT 3 INTEREST FORMULAS & RATES Part 2Document7 pagesEM5 UNIT 3 INTEREST FORMULAS & RATES Part 2MOBILEE CANCERERNo ratings yet

- Statement of Comprehensive Income and Changes in Equity ModuleDocument18 pagesStatement of Comprehensive Income and Changes in Equity ModuleCJ GranadaNo ratings yet

- Tugas Kelompok 5 - Studi Kasus Franklin LumberDocument30 pagesTugas Kelompok 5 - Studi Kasus Franklin LumberAgung IswaraNo ratings yet

- Project Profile On Aluminium FabricationsDocument6 pagesProject Profile On Aluminium FabricationsHarsh Ulhas DaveNo ratings yet

- Errata 2020Document3 pagesErrata 2020SamNo ratings yet

- Ash Corporation Comprehensive Audit AdjustmentsDocument8 pagesAsh Corporation Comprehensive Audit AdjustmentsJoshua Philippe PelegrinoNo ratings yet

- SChedule VIDocument88 pagesSChedule VIbhushan2011No ratings yet

- Abu Girma - Determinants Domestic Savings in EthDocument34 pagesAbu Girma - Determinants Domestic Savings in Ethwondimg100% (3)

- Warren Buffett 1997 BRK Annual Report To ShareholdersDocument20 pagesWarren Buffett 1997 BRK Annual Report To ShareholdersBrian McMorrisNo ratings yet

- Philguarantee Vs VPECI and 3plexDocument1 pagePhilguarantee Vs VPECI and 3plexChaNo ratings yet