You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5796)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- PayMe NocDocument2 pagesPayMe NocRmillionsque FinserveNo ratings yet

- Toward A Framework For Vietnamese American StudiesDocument4 pagesToward A Framework For Vietnamese American StudiesASIAANALYSISNo ratings yet

- Water Conflict ZMWKC-TransformativeAnalysis2019Document21 pagesWater Conflict ZMWKC-TransformativeAnalysis2019ASIAANALYSISNo ratings yet

- The Ming Invasion of VietnamDocument11 pagesThe Ming Invasion of VietnamASIAANALYSISNo ratings yet

- India Initiates Measures To Tackle Floods From Glacial Lake Outbursts in Himalayas - The DiplomatDocument5 pagesIndia Initiates Measures To Tackle Floods From Glacial Lake Outbursts in Himalayas - The DiplomatASIAANALYSISNo ratings yet

- ART - The Precarious State of The Mekong - The DiplomatDocument36 pagesART - The Precarious State of The Mekong - The DiplomatASIAANALYSISNo ratings yet

- What Is China's Role in Central Asia's Changing Climate - The DiplomatDocument7 pagesWhat Is China's Role in Central Asia's Changing Climate - The DiplomatASIAANALYSISNo ratings yet

- The Mekong Issue On ASEAN's Agenda and Vietnam's Middle-Power DiplomacyDocument11 pagesThe Mekong Issue On ASEAN's Agenda and Vietnam's Middle-Power DiplomacyASIAANALYSISNo ratings yet

- China-Financed Hydroelectric Power Plant Faces Popular Opposition in Mongolia - The DiplomatDocument7 pagesChina-Financed Hydroelectric Power Plant Faces Popular Opposition in Mongolia - The DiplomatASIAANALYSISNo ratings yet

- Martin Grossheim - The Sword and Shield of The Party - How The Vietnamese People'sDocument4 pagesMartin Grossheim - The Sword and Shield of The Party - How The Vietnamese People'sASIAANALYSISNo ratings yet

- Wildlife: Vietnam's Footprint in AfricaDocument32 pagesWildlife: Vietnam's Footprint in AfricaASIAANALYSISNo ratings yet

- Has Nguyen Phu Trong's Leadership Curbed Economic Reform - Economic Reform Trends in VietnamDocument18 pagesHas Nguyen Phu Trong's Leadership Curbed Economic Reform - Economic Reform Trends in VietnamASIAANALYSISNo ratings yet

- 19 184 Lykkes Little Three Legged Stool Part 1 TranscriptDocument7 pages19 184 Lykkes Little Three Legged Stool Part 1 TranscriptASIAANALYSISNo ratings yet

- Pesticide Use, Production Risk and Shocks. The Case of Rice Producers in VietnamDocument9 pagesPesticide Use, Production Risk and Shocks. The Case of Rice Producers in VietnamASIAANALYSISNo ratings yet

- 10 Steps To CybersecurityDocument14 pages10 Steps To CybersecurityASIAANALYSISNo ratings yet

- The US Military's Approach To Strategy and The Implications For Military TechnologyDocument56 pagesThe US Military's Approach To Strategy and The Implications For Military TechnologyASIAANALYSISNo ratings yet

- What We Know About PiracyDocument34 pagesWhat We Know About PiracyASIAANALYSISNo ratings yet

- The Southeast Asia Militant AtlasDocument15 pagesThe Southeast Asia Militant AtlasASIAANALYSISNo ratings yet

- Nsutant Buddhist Natlonalismt The Gam of PanDocument26 pagesNsutant Buddhist Natlonalismt The Gam of PanASIAANALYSISNo ratings yet

- International Hydro-DiplomacyDocument48 pagesInternational Hydro-DiplomacyASIAANALYSISNo ratings yet

- Winning The Fight Taiwan Cannot Afford To LoseDocument16 pagesWinning The Fight Taiwan Cannot Afford To LoseASIAANALYSISNo ratings yet

- China S Foreign Policy in Southeast AsiaDocument17 pagesChina S Foreign Policy in Southeast AsiaASIAANALYSISNo ratings yet

- South China Sea Intelligence BriefingsDocument18 pagesSouth China Sea Intelligence BriefingsASIAANALYSISNo ratings yet

- Are China'S Nationally Determined Contributions (NDCS) So Bad?Document5 pagesAre China'S Nationally Determined Contributions (NDCS) So Bad?ASIAANALYSISNo ratings yet

- Nuclear Belt and Road Chinas Ambition For Nuclear Exports and Its Implications For The WorldDocument32 pagesNuclear Belt and Road Chinas Ambition For Nuclear Exports and Its Implications For The WorldASIAANALYSISNo ratings yet

- Guide To Chinese Climate Policy - 2019Document169 pagesGuide To Chinese Climate Policy - 2019ASIAANALYSISNo ratings yet

- UNIT 1 PFP Classwork Sums RevisedDocument5 pagesUNIT 1 PFP Classwork Sums RevisedVarun jajalNo ratings yet

- The Non-Performing Loans: Some Bank-Level EvidencesDocument34 pagesThe Non-Performing Loans: Some Bank-Level EvidencesJORKOS1No ratings yet

- Fore Closure 47119583Document1 pageFore Closure 47119583Shuvajit PradhanNo ratings yet

- Ra 9243Document3 pagesRa 9243Chino SisonNo ratings yet

- KrazyBee Services Private LimitedDocument9 pagesKrazyBee Services Private LimitedBalakrishnan IyerNo ratings yet

- Alishba Internship ReportDocument48 pagesAlishba Internship ReportAlishba NadeemNo ratings yet

- ABBA (Housing Loan)Document8 pagesABBA (Housing Loan)Nurul JannahNo ratings yet

- Stinnett's Pontiac Service, Inc., Richard W. Stinnett and Gay P. Stinnett v. Commissioner of Internal Revenue Service, 730 F.2d 634, 11th Cir. (1984)Document11 pagesStinnett's Pontiac Service, Inc., Richard W. Stinnett and Gay P. Stinnett v. Commissioner of Internal Revenue Service, 730 F.2d 634, 11th Cir. (1984)Scribd Government DocsNo ratings yet

- World Bank GlossaryDocument435 pagesWorld Bank Glossarydon_isauroNo ratings yet

- Tutorial Letter 104/2/2021: Interactive ProgrammingDocument11 pagesTutorial Letter 104/2/2021: Interactive ProgrammingHendrick T HlungwaniNo ratings yet

- Banking ReviewerDocument41 pagesBanking ReviewerCindy-chan DelfinNo ratings yet

- Final Review QuestionsDocument2 pagesFinal Review QuestionshatanoloveNo ratings yet

- Loan Application: Annex 1Document18 pagesLoan Application: Annex 1NinoSawiranNo ratings yet

- Finacle 19A - Cbs Menu - UpgbDocument27 pagesFinacle 19A - Cbs Menu - UpgbyezdiarwNo ratings yet

- T4. How Do You Answer This Ques - GreenwoodDocument11 pagesT4. How Do You Answer This Ques - Greenwood嘉慧No ratings yet

- Faculty of Law Jamia Millia Islamia: Income From House PropertyDocument21 pagesFaculty of Law Jamia Millia Islamia: Income From House PropertyMohdSaqibNo ratings yet

- Will Problem - 4: TH STDocument17 pagesWill Problem - 4: TH STMohamed RaaziqNo ratings yet

- 1817 RulesDocument24 pages1817 RulesLuis Evangelista100% (2)

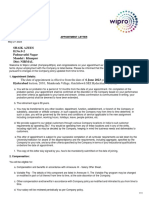

- Appointment LetterDocument11 pagesAppointment LetterramNo ratings yet

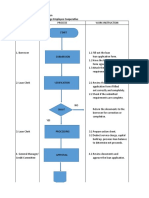

- Process Flow of Loan Application UMTEMPCO - UM Tagum College Employee CooperativeDocument4 pagesProcess Flow of Loan Application UMTEMPCO - UM Tagum College Employee CooperativeJao FloresNo ratings yet

- Partnership - Installment Liquidation Joint Ventures: Roxas, Soto, and TodaDocument27 pagesPartnership - Installment Liquidation Joint Ventures: Roxas, Soto, and TodamarieieiemNo ratings yet

- Group Assignment 2 English ProfesionalDocument13 pagesGroup Assignment 2 English ProfesionalNurfadilla ZahraNo ratings yet

- Reconstitution of Partnership DeedDocument5 pagesReconstitution of Partnership Deedsavaliyamahesh100% (2)

- Letter of GuaranteeDocument9 pagesLetter of GuaranteeMd Jahirul Islam RaselNo ratings yet

- Evaluating External EnvironmentDocument8 pagesEvaluating External EnvironmentSaadiyah muNo ratings yet

- Criminal Law: Chairperson 20006 Bar Examination CommitteeDocument6 pagesCriminal Law: Chairperson 20006 Bar Examination CommitteeJms SapNo ratings yet

- Report On General TyreDocument21 pagesReport On General TyreTahir KhanNo ratings yet

- MODULE 5 Business and Consumer Loans - Part 1 PDFDocument24 pagesMODULE 5 Business and Consumer Loans - Part 1 PDFKimberlyn Granzo0% (1)

- PIP Lender List CountyDocument6 pagesPIP Lender List CountyKimberliNo ratings yet