You might also like

- A Financial Analysis UnionBank of The PhilippinesDocument19 pagesA Financial Analysis UnionBank of The PhilippinesGenessa BasiliscoNo ratings yet

- CBM Individual Credit Report (Sample)Document7 pagesCBM Individual Credit Report (Sample)BotaNo ratings yet

- Cash Receipts System Narrative 2010 v3Document4 pagesCash Receipts System Narrative 2010 v3cristel jane FullonesNo ratings yet

- Reflection-Paper Chapter 1 International ManagementDocument2 pagesReflection-Paper Chapter 1 International ManagementJouhara G. San JuanNo ratings yet

- Inventory System For Marisol Grocery Store MODIFIEDDocument36 pagesInventory System For Marisol Grocery Store MODIFIEDpang testNo ratings yet

- General Mercantile Agency: Credit Bureau Public Company Short Hills Millburn Business-To-BusinessDocument2 pagesGeneral Mercantile Agency: Credit Bureau Public Company Short Hills Millburn Business-To-BusinessSteph BorinagaNo ratings yet

- Shakey's 2021Document69 pagesShakey's 2021Megan CastilloNo ratings yet

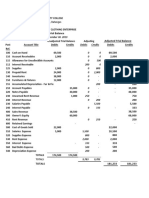

- Mabini Colleges, Inc. College of Business Administration and AccountancyDocument4 pagesMabini Colleges, Inc. College of Business Administration and AccountancyCarla Jane ApolinarioNo ratings yet

- Henry Ford College MATH-131 Mathematics For The Modern WorldDocument3 pagesHenry Ford College MATH-131 Mathematics For The Modern WorldRodalyn PagaduanNo ratings yet

- Cash and Cash EquivalentsDocument2 pagesCash and Cash Equivalentsyes it's kaiNo ratings yet

- 11 - Bank Reconciliation NotesDocument3 pages11 - Bank Reconciliation NotesJann GataNo ratings yet

- Week 5 CCP Target Market ID & PrescreeningDocument26 pagesWeek 5 CCP Target Market ID & PrescreeningAkii WingNo ratings yet

- Module 1 - Cash and Cash EquivalentsDocument10 pagesModule 1 - Cash and Cash EquivalentsGRACE ANN BERGONIONo ratings yet

- Tax 06 Capital Gains Taxation Part 4Document7 pagesTax 06 Capital Gains Taxation Part 4Panda CocoNo ratings yet

- Business TaxDocument65 pagesBusiness TaxSandia Espejo100% (1)

- RMC 71-2022 Annex ADocument13 pagesRMC 71-2022 Annex AKe VinNo ratings yet

- ExperimentDocument37 pagesExperimentErica Joy EscopeteNo ratings yet

- Impact of CWG ScamDocument19 pagesImpact of CWG ScamAlpana Varnwal100% (1)

- Chapter 02 - Statement of Financial Position and Income StatementDocument20 pagesChapter 02 - Statement of Financial Position and Income StatementThorngsokhom0% (1)

- 1.3 Introduction To Money and Interest RatesDocument2 pages1.3 Introduction To Money and Interest RatesJessa Lyn Gao LapinigNo ratings yet

- Donor's Tax - 10101Document44 pagesDonor's Tax - 10101aehy lznuscrfbjNo ratings yet

- PNBDocument3 pagesPNBLove KarenNo ratings yet

- Smith's Market Case StudyDocument9 pagesSmith's Market Case StudyDhanylane Phole Librea SeraficaNo ratings yet

- Week 1 - The Financial SystemDocument6 pagesWeek 1 - The Financial SystemKhen CaballesNo ratings yet

- Accounting For Merchandising Business - Sample TransactionsDocument12 pagesAccounting For Merchandising Business - Sample TransactionsLeica Jayme100% (1)

- Business Finance 1ST Chunk 1Document52 pagesBusiness Finance 1ST Chunk 1Mary Ann EstudilloNo ratings yet

- Working Capital Management Practices and Sustainability of Barangay Micro Business Enterprises (BMBEs) in Ilocos Norte, PhilippinesDocument12 pagesWorking Capital Management Practices and Sustainability of Barangay Micro Business Enterprises (BMBEs) in Ilocos Norte, PhilippinesGeorgina De LiañoNo ratings yet

- Jerlene Joy I. Bruan Bsacc-1Document4 pagesJerlene Joy I. Bruan Bsacc-1Jochelle SorianoNo ratings yet

- Strategic Management Final Paper (Salazar Fitness Gym)Document42 pagesStrategic Management Final Paper (Salazar Fitness Gym)Mejielin PalmaNo ratings yet

- Consumer Spending Via Electronic/digital Wallets: A Study On Indian CommunityDocument10 pagesConsumer Spending Via Electronic/digital Wallets: A Study On Indian CommunityjankiNo ratings yet

- Unit 4 E-Business, E-Commerce, and M-CommerceDocument11 pagesUnit 4 E-Business, E-Commerce, and M-CommerceJenilyn CalaraNo ratings yet

- CHAPTER 10 Audit in CIS EnvironmentDocument56 pagesCHAPTER 10 Audit in CIS EnvironmentJenalyn OreñaNo ratings yet

- The Role of Strategic Planning On The Sustainability of Selected MSMEs in The 2nd District of AlbayDocument7 pagesThe Role of Strategic Planning On The Sustainability of Selected MSMEs in The 2nd District of AlbayInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Chase CoDocument58 pagesChase CoRatna Tazulazhar100% (1)

- Final Income TaxationDocument8 pagesFinal Income TaxationJade Ivy GarciaNo ratings yet

- Final PaperDocument82 pagesFinal PaperCristy Martin Yumul100% (1)

- Step AnalysisDocument13 pagesStep AnalysisLow El LaNo ratings yet

- Pandemic Contributed To Homicide in Houston TexasDocument32 pagesPandemic Contributed To Homicide in Houston TexasJeselyn MalaluanNo ratings yet

- Art Appreciation. Act. 2Document3 pagesArt Appreciation. Act. 2April Joy ObedozaNo ratings yet

- Chapter 2 Financial Statement Analysis For StudentsDocument49 pagesChapter 2 Financial Statement Analysis For StudentsRossetteDulinNo ratings yet

- Pricing Quiz With SolutionDocument4 pagesPricing Quiz With SolutionShieryl-Joy Postrero PorrasNo ratings yet

- I. Learning Activities: Sum of Weights (3+2+1) 6Document6 pagesI. Learning Activities: Sum of Weights (3+2+1) 6Valdez AlyssaNo ratings yet

- AE 25 Module 1 Lesson 1Document99 pagesAE 25 Module 1 Lesson 1Queeny Mae Cantre ReutaNo ratings yet

- Working Capital Management (Answer)Document1 pageWorking Capital Management (Answer)Ronalisa Manzano EdemNo ratings yet

- Accounting For MerchandisingDocument2 pagesAccounting For MerchandisingEvelyn MaligayaNo ratings yet

- Chapter Two Master BudgetDocument15 pagesChapter Two Master BudgetNigussie BerhanuNo ratings yet

- Accounting For FreightDocument4 pagesAccounting For FreightHearty HitutuaNo ratings yet

- Activity Number 5 Elasticity of Demand & SupplyDocument5 pagesActivity Number 5 Elasticity of Demand & SupplyLovely Madrid0% (1)

- Credit and Background: Microfinance Flow ChartDocument21 pagesCredit and Background: Microfinance Flow ChartJerry Sarabia JordanNo ratings yet

- Cash and CashDocument13 pagesCash and CashAnonymous WmvilCEFNo ratings yet

- Module 9 - Commercial Bank Management PDFDocument16 pagesModule 9 - Commercial Bank Management PDFRodel Novesteras ClausNo ratings yet

- Inventory Management and Cash BudgetDocument3 pagesInventory Management and Cash BudgetRashi MehtaNo ratings yet

- Payroll AccountingDocument26 pagesPayroll AccountingShean VasilićNo ratings yet

- Developing Online Shopping Application and Data AnalysisDocument5 pagesDeveloping Online Shopping Application and Data AnalysisInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Credit Union in The PhilippinesDocument4 pagesCredit Union in The PhilippinesJoyce-An Nicole MercadoNo ratings yet

- XYZ COMPANY (Balance Sheet)Document2 pagesXYZ COMPANY (Balance Sheet)Shielah De JesusNo ratings yet

- Chapter 4 Question ReviewDocument11 pagesChapter 4 Question ReviewNayan SahaNo ratings yet

- Bhebu Lero TransactionDocument5 pagesBhebu Lero TransactionLeo Marbeda FeigenbaumNo ratings yet

- Problem 7-1 (Iaa)Document13 pagesProblem 7-1 (Iaa)Chloe CatalunaNo ratings yet

- Financial StatementDocument12 pagesFinancial StatementCecilia CajipoNo ratings yet

- Chapter 1 Introduction To Personal Financial ManagementDocument9 pagesChapter 1 Introduction To Personal Financial ManagementLee K.No ratings yet

- Human Behavior in OrganizationDocument8 pagesHuman Behavior in OrganizationLee K.No ratings yet

- Philippine Business Enviroment PresentationDocument29 pagesPhilippine Business Enviroment PresentationLee K.No ratings yet

- Introduction Personal Financial ManagementDocument3 pagesIntroduction Personal Financial ManagementLee K.No ratings yet

- 08 - PFM - Chapter 7 - Introduction To Personal Financial Management - Major ExpenditureDocument5 pages08 - PFM - Chapter 7 - Introduction To Personal Financial Management - Major ExpenditureLee K.No ratings yet

- 09 PFM Chapter 8 Purchasing Consumer DurablesDocument6 pages09 PFM Chapter 8 Purchasing Consumer DurablesLee K.No ratings yet

- Slide Presentation by Lesley Allen Kabigting For The Role of Economics in Environmental ManagementDocument35 pagesSlide Presentation by Lesley Allen Kabigting For The Role of Economics in Environmental ManagementLee K.No ratings yet

- 07 PFM Chapter 6 Establishing Consumer CreditDocument4 pages07 PFM Chapter 6 Establishing Consumer CreditLee K.No ratings yet

- 11 - PFM - Chapter 10 - Financing Health and Care LiabilityDocument9 pages11 - PFM - Chapter 10 - Financing Health and Care LiabilityLee K.No ratings yet

- 02 - PFM - Chapter 1 - Introduction To Personal Financial ManagementDocument9 pages02 - PFM - Chapter 1 - Introduction To Personal Financial ManagementLee K.No ratings yet

- 14 - PFM - Chapter 13 - Retirement and Estate PlanningDocument2 pages14 - PFM - Chapter 13 - Retirement and Estate PlanningLee K.No ratings yet

- Lesley Allen Kabigting: Chapter 02 Business Notion From The PhilosophersDocument7 pagesLesley Allen Kabigting: Chapter 02 Business Notion From The PhilosophersLee K.No ratings yet

- Lesley Kabigting Presentation For Ethics and Accountability: Light OffensesDocument3 pagesLesley Kabigting Presentation For Ethics and Accountability: Light OffensesLee K.No ratings yet

- Guagua National Colleges Graduate School Master's in Business AdministrationDocument25 pagesGuagua National Colleges Graduate School Master's in Business AdministrationLee K.No ratings yet

- Business Policy: International Expansion: A Company's Motivation and Risks / Child Labor in Global MarketingDocument20 pagesBusiness Policy: International Expansion: A Company's Motivation and Risks / Child Labor in Global MarketingLee K.No ratings yet

- 01 - OM - Introduction To Operations ManagementDocument2 pages01 - OM - Introduction To Operations ManagementLee K.No ratings yet

- 03 - OM - Chapter 2 - Product and Service DesignDocument6 pages03 - OM - Chapter 2 - Product and Service DesignLee K.No ratings yet

- 02 OM Chapter 1 ForecastingDocument15 pages02 OM Chapter 1 ForecastingLee K.No ratings yet