You might also like

- Uk Angel InvestorsDocument38 pagesUk Angel InvestorsShaik Inayath0% (1)

- Book 02Document322 pagesBook 02tazimNo ratings yet

- Topic 2 - Concept of Shariah Compliance InvestmentDocument31 pagesTopic 2 - Concept of Shariah Compliance Investmenthidayatul raihanNo ratings yet

- Assignment V (B)Document23 pagesAssignment V (B)Shilpi KauntiaNo ratings yet

- Chapter-4 Investment and Risk: Investment: The Changing Framework and Methods of Investment ManagementDocument27 pagesChapter-4 Investment and Risk: Investment: The Changing Framework and Methods of Investment ManagementSiva MohanNo ratings yet

- Managment Assigment Ali Irtaza Islamic BankingDocument4 pagesManagment Assigment Ali Irtaza Islamic BankingaliNo ratings yet

- 06 Chapter1Document33 pages06 Chapter1touffiqNo ratings yet

- Investment EnvironmentDocument25 pagesInvestment EnvironmentK-Ayurveda WelexNo ratings yet

- INVESTMENT AlternativesDocument69 pagesINVESTMENT Alternativesdhvanichauhan476No ratings yet

- Book 02Document377 pagesBook 02tazimNo ratings yet

- Investment Emvironment BBA 7th Sem PYCDocument17 pagesInvestment Emvironment BBA 7th Sem PYCDeexyant TimilsinaNo ratings yet

- Real Estate Investment and Marketing Chapter 3 - 5Document57 pagesReal Estate Investment and Marketing Chapter 3 - 5Firaol Nigussie100% (1)

- Investment: An Investment Is An Asset or Item Acquired With The GoalDocument17 pagesInvestment: An Investment Is An Asset or Item Acquired With The GoalBCom 2 B RPD CollegeNo ratings yet

- Islamic Finance NotesDocument6 pagesIslamic Finance NotesHosea KanyangaNo ratings yet

- Chap 01 Understanding InvestmentDocument32 pagesChap 01 Understanding InvestmentRifat AnjanNo ratings yet

- Ty BMS Project Detail PDFDocument69 pagesTy BMS Project Detail PDFnarayan patelNo ratings yet

- Islamic Investment PlanningDocument29 pagesIslamic Investment Planningmuhammad arifNo ratings yet

- Top Ten - Islamic FinanceDocument4 pagesTop Ten - Islamic Financesadique_homeNo ratings yet

- Without This Message by Purchasing Novapdf : Print To PDFDocument35 pagesWithout This Message by Purchasing Novapdf : Print To PDFShweta VijayNo ratings yet

- Investment Analysis & Portfolio ManagementDocument65 pagesInvestment Analysis & Portfolio ManagementKaran Kumar100% (1)

- Islamic Studies 1: Syeda Gull Zainab GardeziDocument11 pagesIslamic Studies 1: Syeda Gull Zainab GardeziZainab GardeziNo ratings yet

- An Introduction To Islamic FinanceDocument14 pagesAn Introduction To Islamic FinanceThargistNo ratings yet

- Chapter 2Document26 pagesChapter 2Amanlal TapaseNo ratings yet

- Maksud Unit TrustDocument6 pagesMaksud Unit TrusthusainiNo ratings yet

- Investment Law EvolutionDocument39 pagesInvestment Law EvolutionAdarsh RanjanNo ratings yet

- Products of Islamic Finance: A Shariah Compliance AdvancementDocument6 pagesProducts of Islamic Finance: A Shariah Compliance AdvancementAreni SabrinaNo ratings yet

- Assientment 1Document6 pagesAssientment 1anvithapremagowdaNo ratings yet

- IslamicDocument4 pagesIslamicKumanan MunusamyNo ratings yet

- Securities Analysis and Portfolio Management PDFDocument64 pagesSecurities Analysis and Portfolio Management PDFShreya s shetty100% (1)

- II M.com. - 18PCO7 - Dr. R. Sathru Sankara VelsamyDocument80 pagesII M.com. - 18PCO7 - Dr. R. Sathru Sankara Velsamykiruthika2010No ratings yet

- Chap-11 Business Finance and Fundamentals of AccountingDocument23 pagesChap-11 Business Finance and Fundamentals of AccountingSiffat Bin AyubNo ratings yet

- Financial Management - SBSDocument158 pagesFinancial Management - SBSHamsa SrinivasNo ratings yet

- Islamic Invest PDFDocument12 pagesIslamic Invest PDFKarachiFashion ReplicaNo ratings yet

- 21BSPHH01C0084 AKSHITASK PMMFDocument4 pages21BSPHH01C0084 AKSHITASK PMMFAkshita SkNo ratings yet

- Islamic InstrumentsDocument7 pagesIslamic InstrumentslekshmiNo ratings yet

- Working With Islamic FinanceDocument3 pagesWorking With Islamic FinanceNaffay HussainNo ratings yet

- Introduction and Theoretical Background: Chapter - 1Document77 pagesIntroduction and Theoretical Background: Chapter - 1ranveer3854No ratings yet

- Chapter-1 Portfolio Management IntroDocument16 pagesChapter-1 Portfolio Management Intro8008 Aman GuptaNo ratings yet

- E7 Introduction To Islamic FinanceDocument5 pagesE7 Introduction To Islamic FinanceTENGKU ANIS TENGKU YUSMANo ratings yet

- FNM104 Prelim ReviewerDocument8 pagesFNM104 Prelim ReviewerjelciumNo ratings yet

- INSIGHT Potfolio MGNTDocument35 pagesINSIGHT Potfolio MGNTHari NairNo ratings yet

- Introduction To Investment ManagementDocument11 pagesIntroduction To Investment ManagementAsif Abdullah KhanNo ratings yet

- Assignment 1 Business Mathematics (MAT 402)Document4 pagesAssignment 1 Business Mathematics (MAT 402)biokimia 2018100% (1)

- Investement Analysis and Portfolio Management Chapter 1Document8 pagesInvestement Analysis and Portfolio Management Chapter 1Oumer Shaffi100% (3)

- Study On Islamic Finance and Products.: Mohammed Saleem .OADocument31 pagesStudy On Islamic Finance and Products.: Mohammed Saleem .OASaleem VettomNo ratings yet

- Domestic and Foreign Finance: Presented By: Virendra Kharbale (26) Mms-1 Year Cktimsr, New PanvelDocument31 pagesDomestic and Foreign Finance: Presented By: Virendra Kharbale (26) Mms-1 Year Cktimsr, New PanvelVirendra KharbaleNo ratings yet

- Chap 01 Understanding InvestmentDocument26 pagesChap 01 Understanding Investmentall friends100% (1)

- Unit 1Document52 pagesUnit 1vijay SNo ratings yet

- Mutual FundsDocument40 pagesMutual Fundsaditi anandNo ratings yet

- UTB ProjectDocument6 pagesUTB ProjectNoor AssignmentsNo ratings yet

- Ecm620t - Invest MGT MaterialDocument88 pagesEcm620t - Invest MGT Materialnivantheking123No ratings yet

- Products of Islamic FinanceDocument18 pagesProducts of Islamic FinanceTanveer Shah, MBA Scholar, Institute of Management Studies, UoPNo ratings yet

- Islamic FinaceDocument8 pagesIslamic Finacenur_light25No ratings yet

- Chapter Three Investment Process and AlternativesDocument36 pagesChapter Three Investment Process and AlternativesKume MezgebuNo ratings yet

- Lecture Notes - Investment Appraisal IDocument12 pagesLecture Notes - Investment Appraisal IKato mayanja100% (1)

- Top 5 Investment AlternativesDocument9 pagesTop 5 Investment AlternativesSrinivasan SrinivasanNo ratings yet

- Introduction To Investment Management: Bond, Real Estate, Mortgages EtcDocument25 pagesIntroduction To Investment Management: Bond, Real Estate, Mortgages EtcRavi GuptaNo ratings yet

- INVESTMENTDocument11 pagesINVESTMENTLAROA, Mychell D.No ratings yet

- Basics of Financial SystemDocument11 pagesBasics of Financial SystemammarNo ratings yet

- Investing Made Easy: Finding the Right Opportunities for YouFrom EverandInvesting Made Easy: Finding the Right Opportunities for YouNo ratings yet

- Chapter 5 Theory of Production UpdateDocument35 pagesChapter 5 Theory of Production Updatehidayatul raihanNo ratings yet

- Chapter 2 Theory of Demand and SupplyDocument25 pagesChapter 2 Theory of Demand and Supplyhidayatul raihanNo ratings yet

- Chapter 2 Theory of Demand and SupplyDocument25 pagesChapter 2 Theory of Demand and Supplyhidayatul raihanNo ratings yet

- Chapter 3 Theory of ElasticityDocument35 pagesChapter 3 Theory of Elasticityhidayatul raihanNo ratings yet

- Chapter 6 Theory of Firm and Market Structure - PART 2Document20 pagesChapter 6 Theory of Firm and Market Structure - PART 2hidayatul raihanNo ratings yet

- 2 - Generating and Exploiting New Entry StrategiesDocument25 pages2 - Generating and Exploiting New Entry StrategiesSiti Sarah Zalikha Binti Umar BakiNo ratings yet

- Chapter 3 Business Idea and OpportunityDocument13 pagesChapter 3 Business Idea and Opportunitydear sunwooNo ratings yet

- Equilibrium - Price - Application - Modelling - For - Affordable Housing Market in MalaysiaDocument7 pagesEquilibrium - Price - Application - Modelling - For - Affordable Housing Market in Malaysiahidayatul raihanNo ratings yet

- Topic 5 - Ethics in Islamic InvestmentDocument78 pagesTopic 5 - Ethics in Islamic Investmenthidayatul raihanNo ratings yet

- Topic 4 - Islamic Investment MethodsDocument53 pagesTopic 4 - Islamic Investment Methodshidayatul raihanNo ratings yet

- The Relationship Between House Prices and Economic Growth in MalaysiaDocument12 pagesThe Relationship Between House Prices and Economic Growth in Malaysiahidayatul raihanNo ratings yet

- Price Control in Housing Affordability From Islamic PerspectiveDocument9 pagesPrice Control in Housing Affordability From Islamic Perspectivehidayatul raihanNo ratings yet

- Topic 3 - Shariah Regulation in InvestmentDocument29 pagesTopic 3 - Shariah Regulation in Investmenthidayatul raihanNo ratings yet

- 2 - IMU150 - The Importance of SB and The PillarsDocument27 pages2 - IMU150 - The Importance of SB and The Pillarshidayatul raihanNo ratings yet

- IMU150 Al-'Uqud Al-Fiqh Al-Muamalah: Types of Islamic Selling & Buying: Bay' Al-MurabahahDocument28 pagesIMU150 Al-'Uqud Al-Fiqh Al-Muamalah: Types of Islamic Selling & Buying: Bay' Al-Murabahahhidayatul raihanNo ratings yet

- 2 - IMU150 - The Importance of SB and The PillarsDocument27 pages2 - IMU150 - The Importance of SB and The Pillarshidayatul raihanNo ratings yet

- 1 - Imu150 - Selling N Buying ConceptDocument22 pages1 - Imu150 - Selling N Buying Concepthidayatul raihanNo ratings yet

- Tawarruq As A Useful Instrument To Finance Retail The Halal WayDocument10 pagesTawarruq As A Useful Instrument To Finance Retail The Halal Wayhidayatul raihanNo ratings yet

- Tawarruq As A Useful Instrument To Finance Retail The Halal WayDocument10 pagesTawarruq As A Useful Instrument To Finance Retail The Halal WayzilaNo ratings yet

- 1 - Imu150 - Selling N Buying ConceptDocument22 pages1 - Imu150 - Selling N Buying Concepthidayatul raihanNo ratings yet

- IMU150 Al-'Uqud Al-Fiqh Al-Muamalah: Types of Islamic Selling & Buying: Bay' Al-MurabahahDocument28 pagesIMU150 Al-'Uqud Al-Fiqh Al-Muamalah: Types of Islamic Selling & Buying: Bay' Al-Murabahahhidayatul raihanNo ratings yet

- MM ModelDocument91 pagesMM ModelBenjamin TanNo ratings yet

- Fcma, Fpa, Ma (Economics), BSC Dubai, United Arab Emirates: Presentation byDocument42 pagesFcma, Fpa, Ma (Economics), BSC Dubai, United Arab Emirates: Presentation byAhmad Tariq Bhatti100% (1)

- GS 2011 Annual ReportDocument228 pagesGS 2011 Annual ReportEric PlattNo ratings yet

- Asset Management Company AnalysisDocument2 pagesAsset Management Company AnalysisDhoni KhanNo ratings yet

- Replacement Theory: 20P204 - ASHWIN R 20P217 - Prithivirajan V 20P220 - Vijay Vignesh S 21P402 - Gurumoorthy DDocument20 pagesReplacement Theory: 20P204 - ASHWIN R 20P217 - Prithivirajan V 20P220 - Vijay Vignesh S 21P402 - Gurumoorthy D21P410 - VARUN MNo ratings yet

- Top 6 Bollinger Bands® Trading Strategies: Learn How (/)Document20 pagesTop 6 Bollinger Bands® Trading Strategies: Learn How (/)bhavin shahNo ratings yet

- Ignacio Vinke - Investments Homework 1Document19 pagesIgnacio Vinke - Investments Homework 1Ignacio Andrés VinkeNo ratings yet

- Yearbook 2009Document274 pagesYearbook 2009mkasi2k9No ratings yet

- Cash Flow Statement Important QuestionsDocument20 pagesCash Flow Statement Important QuestionsSatinder SinghNo ratings yet

- An Overview of Strategic ManagementDocument20 pagesAn Overview of Strategic ManagementRick dharNo ratings yet

- Vale Day - Capex, Iron Ore Market, Partnerships & Cost Cuts - 04dez13 - BBDDocument13 pagesVale Day - Capex, Iron Ore Market, Partnerships & Cost Cuts - 04dez13 - BBDbenjah2No ratings yet

- Demystifying Private Climate FinanceDocument62 pagesDemystifying Private Climate FinanceSaurav SumanNo ratings yet

- Staff Salary CIMB AccountDocument26 pagesStaff Salary CIMB Accountmieka8687631No ratings yet

- Technical AnalysisDocument69 pagesTechnical AnalysisNikhil KhandelwalNo ratings yet

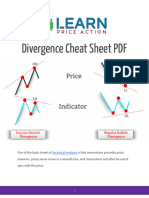

- Divergence Cheat Sheet PDFDocument17 pagesDivergence Cheat Sheet PDFlightbarq100% (1)

- FSA Chapter 7Document3 pagesFSA Chapter 7Nadia ZahraNo ratings yet

- UAW 2015 LM2 BDocument288 pagesUAW 2015 LM2 Bthe kingfishNo ratings yet

- WACC & PaybackDocument9 pagesWACC & PaybackBelle Dela CruzNo ratings yet

- Forex Strategies Ebook PDFDocument10 pagesForex Strategies Ebook PDFBOLA AJAIBNo ratings yet

- Cash Flow Analysis For Nestle India LTDDocument2 pagesCash Flow Analysis For Nestle India LTDVinayak Arun SahiNo ratings yet

- 04 Chapter1Document42 pages04 Chapter1Motiram paudelNo ratings yet

- Accounting Oct 21:2022Document20 pagesAccounting Oct 21:2022SamarahNo ratings yet

- Initiating Coverage On JP Associates LTDDocument23 pagesInitiating Coverage On JP Associates LTDVarun YadavNo ratings yet

- Ttel.: Resa of Accountancy 735-98O7 & 734-3989Document1 pageTtel.: Resa of Accountancy 735-98O7 & 734-3989KyohyunNo ratings yet

- Profit & LossDocument12 pagesProfit & Losskrish589748No ratings yet

- Lesson 3 Value Investing For Smart People Safal NiveshakDocument3 pagesLesson 3 Value Investing For Smart People Safal NiveshakKohinoor RoyNo ratings yet

- SOIC-Financial Literacy 2 1 Lyst9826Document62 pagesSOIC-Financial Literacy 2 1 Lyst9826bradburywillsNo ratings yet

- The Marketing Mix: Entrepreneurship Myra F. de LeonDocument21 pagesThe Marketing Mix: Entrepreneurship Myra F. de LeonguiaNo ratings yet

- WaccDocument33 pagesWaccAnkitNo ratings yet