You might also like

- John M CaseDocument10 pagesJohn M Caseadrian_simm100% (1)

- King Conan - Crown of Iron (P. 14)Document167 pagesKing Conan - Crown of Iron (P. 14)Rafa Eyesman100% (2)

- Unilever IFE EFE CPM MatrixDocument7 pagesUnilever IFE EFE CPM MatrixNabeel Raja73% (11)

- Acova RadiateursDocument10 pagesAcova RadiateursAnandNo ratings yet

- (S3) Butler Lumber - EnGDocument11 pages(S3) Butler Lumber - EnGdavidinmexicoNo ratings yet

- Titan Co Financial ModelDocument15 pagesTitan Co Financial ModelAtharva OrpeNo ratings yet

- Pacific Grove Spice CompanyDocument3 pagesPacific Grove Spice CompanyLaura JavelaNo ratings yet

- New Heritage Doll Company Case SolutionDocument31 pagesNew Heritage Doll Company Case SolutionSoundarya AbiramiNo ratings yet

- Model Assignment Aug-23Document3 pagesModel Assignment Aug-23Abner ogegaNo ratings yet

- Frivaldo Vs Comelec 1996Document51 pagesFrivaldo Vs Comelec 1996Eunice AmbrocioNo ratings yet

- Wittenberg University Constitution and BylawsDocument22 pagesWittenberg University Constitution and BylawsTrent SpragueNo ratings yet

- Gacal v. PALDocument2 pagesGacal v. PALLynne SanchezNo ratings yet

- Assignment File FMDocument4 pagesAssignment File FMvineeth kumarNo ratings yet

- Case IDocument20 pagesCase ICherry KanjanapornsinNo ratings yet

- New Microsoft Excel WorksheetDocument4 pagesNew Microsoft Excel WorksheetAlexandraNo ratings yet

- Past Papers2Document46 pagesPast Papers2leylaNo ratings yet

- IRR and NPV Analysis-3Document19 pagesIRR and NPV Analysis-3Sarah BunoNo ratings yet

- ACCOWTANCYDocument47 pagesACCOWTANCYleylaNo ratings yet

- The Project (Or Subsidiary) Cashflows: Lecture ExampleDocument15 pagesThe Project (Or Subsidiary) Cashflows: Lecture ExamplelucaNo ratings yet

- 322 Assignment 2 SubmissionDocument9 pages322 Assignment 2 SubmissionMirza Mushahid BaigNo ratings yet

- Food & Beverages Consists of 19 % of The Sector. Heathcare Consists of 31 % of The Sector Household & Personal Care Consists of 50% of The SectorDocument9 pagesFood & Beverages Consists of 19 % of The Sector. Heathcare Consists of 31 % of The Sector Household & Personal Care Consists of 50% of The SectorVivek PatwariNo ratings yet

- Prysor Co ExcelDocument4 pagesPrysor Co Excelsanjay gautamNo ratings yet

- Tata MotorsDocument5 pagesTata Motorsinsurana73No ratings yet

- Tata MotorsDocument24 pagesTata MotorsApurvAdarshNo ratings yet

- Interim Report q3 2023Document26 pagesInterim Report q3 2023jvnshrNo ratings yet

- h1 2021 Results PresentationDocument20 pagesh1 2021 Results PresentationGuilherme SouzaNo ratings yet

- NetscapeDocument3 pagesNetscapeulix1985No ratings yet

- MockDocument5 pagesMockamna noorNo ratings yet

- Nestle and Alcon - The Value of ADocument33 pagesNestle and Alcon - The Value of Akjpcs120% (1)

- Yilendwe ExcelDocument4 pagesYilendwe Excelsanjay gautamNo ratings yet

- Project 1 - Match My Doll Clothing Line: WC Assumption: 2010 2011 2012 2013 2014 2015Document4 pagesProject 1 - Match My Doll Clothing Line: WC Assumption: 2010 2011 2012 2013 2014 2015rohitNo ratings yet

- CocaCola and PepsiCo-2Document23 pagesCocaCola and PepsiCo-2Aditi KathinNo ratings yet

- Grupo Argos Reporte Resultados Trimestrales 4Q2022 ENGDocument27 pagesGrupo Argos Reporte Resultados Trimestrales 4Q2022 ENGSyvel EstevesNo ratings yet

- 8 TopicDocument2 pages8 TopicOtabek QurbonovNo ratings yet

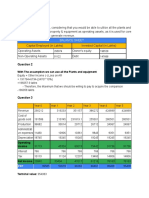

- Balance Sheet: With The Assumption We Can Use All The Plants and EquipmentDocument4 pagesBalance Sheet: With The Assumption We Can Use All The Plants and EquipmentPriadarshini Subramanyam DM21B093No ratings yet

- Qs Answers p4Document214 pagesQs Answers p4HunainNo ratings yet

- Project Appraisal CIA 3Document10 pagesProject Appraisal CIA 3Kush BafnaNo ratings yet

- Chapter 3. Exhibits y AnexosDocument24 pagesChapter 3. Exhibits y AnexosJulio Arroyo GilNo ratings yet

- Wipro Afm DataDocument5 pagesWipro Afm DataDevam DixitNo ratings yet

- Hori, Trend, VertiDocument10 pagesHori, Trend, VertiRishav BhattacharjeeNo ratings yet

- Degnis CoDocument3 pagesDegnis CoPubg DonNo ratings yet

- AirThread SecBC Group9Document4 pagesAirThread SecBC Group9Vishal BhanushaliNo ratings yet

- DCF 2 CompletedDocument4 pagesDCF 2 CompletedPragathi T NNo ratings yet

- 2.+average+of+price+models BeforeDocument23 pages2.+average+of+price+models BeforeMuskan AroraNo ratings yet

- 6.+Energy+and+Other+revenue BeforeDocument37 pages6.+Energy+and+Other+revenue BeforeThe SturdyTubersNo ratings yet

- 8.+opex BeforeDocument45 pages8.+opex BeforeThe SturdyTubersNo ratings yet

- .+Energy+and+Other+gross+profit AfterDocument41 pages.+Energy+and+Other+gross+profit AfterAkash ChauhanNo ratings yet

- 6.+Energy+and+Other+Revenue AfterDocument37 pages6.+Energy+and+Other+Revenue AftervictoriaNo ratings yet

- Projected 2013 2014 2015 2016 2017Document11 pagesProjected 2013 2014 2015 2016 2017Aijaz AslamNo ratings yet

- Presentation Group F Update T6Document21 pagesPresentation Group F Update T6Phạm Hồng SơnNo ratings yet

- Tata Motors FY20-21 FY19-20 FY18-19: ExpenditureDocument6 pagesTata Motors FY20-21 FY19-20 FY18-19: ExpenditureJyothish JbNo ratings yet

- DiviđenDocument12 pagesDiviđenPhan GiápNo ratings yet

- EOG ResourcesDocument16 pagesEOG ResourcesAshish PatwardhanNo ratings yet

- Tesla FinModelDocument58 pagesTesla FinModelPrabhdeep DadyalNo ratings yet

- GMR Financial Overview-Q2 FY11Document44 pagesGMR Financial Overview-Q2 FY11anilgupta_1No ratings yet

- Gross Profit Ad Expenses Depreciation (Dedicated Inv) Jell-O Equipment DepreciationDocument11 pagesGross Profit Ad Expenses Depreciation (Dedicated Inv) Jell-O Equipment Depreciationanmolsaini01No ratings yet

- Key Ratios 5yrs 3yrs Latest: Sales Other Income Total Income Total Expenditure Ebit Interest Tax Net ProfitDocument2 pagesKey Ratios 5yrs 3yrs Latest: Sales Other Income Total Income Total Expenditure Ebit Interest Tax Net ProfitmohithNo ratings yet

- V-Mart Cost of Goods Sold (Cogs)Document12 pagesV-Mart Cost of Goods Sold (Cogs)VinayakNo ratings yet

- CH 3 FCFF MODELDocument11 pagesCH 3 FCFF MODELJaya Mamta ProsadNo ratings yet

- PV OIl Financial Spreadsheet AnalysisDocument32 pagesPV OIl Financial Spreadsheet AnalysisNguyễn Minh ThànhNo ratings yet

- Tesla Company AnalysisDocument83 pagesTesla Company AnalysisStevenTsaiNo ratings yet

- Chmura Co ExcelDocument3 pagesChmura Co Excelsanjay gautamNo ratings yet

- IndusDocument5 pagesIndusFateen HabibNo ratings yet

- Power Markets and Economics: Energy Costs, Trading, EmissionsFrom EverandPower Markets and Economics: Energy Costs, Trading, EmissionsNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- A. To Calculate The Ratios of Fit Co and Sporty Co Ratios 42.6%Document2 pagesA. To Calculate The Ratios of Fit Co and Sporty Co Ratios 42.6%Elsitta Maria SabuNo ratings yet

- Text DocumentDocument1 pageText DocumentElsitta Maria SabuNo ratings yet

- TechnologyDocument1 pageTechnologyElsitta Maria SabuNo ratings yet

- Akshaya Project1 PDFDocument75 pagesAkshaya Project1 PDFElsitta Maria Sabu100% (1)

- How To Prepare A SynopsisDocument1 pageHow To Prepare A SynopsisElsitta Maria SabuNo ratings yet

- Jo LibbeDocument4 pagesJo LibbejacNo ratings yet

- All JD 2019 For StudentsDocument110 pagesAll JD 2019 For StudentsShivam JadhavNo ratings yet

- Intra-Class Moot Court 2021 B.A.Ll.B 3 Year: DwelhiDocument17 pagesIntra-Class Moot Court 2021 B.A.Ll.B 3 Year: DwelhiDinesh SharmaNo ratings yet

- Moodys SC - Russian Banks M&ADocument12 pagesMoodys SC - Russian Banks M&AKsenia TerebkovaNo ratings yet

- Artificial Intelligence IBM FinalDocument35 pagesArtificial Intelligence IBM FinalnonieshzNo ratings yet

- Axess Group - Brazilian ComplianceDocument1 pageAxess Group - Brazilian ComplianceRicardoNo ratings yet

- Vidrine Racism in AmericaDocument12 pagesVidrine Racism in Americaapi-512868919No ratings yet

- Purging CostSavingsDocument2 pagesPurging CostSavingscanakyuzNo ratings yet

- Industry ProfileDocument16 pagesIndustry Profileactive1cafeNo ratings yet

- US Internal Revenue Service: Irb04-43Document27 pagesUS Internal Revenue Service: Irb04-43IRSNo ratings yet

- Notes: 1 Yorùbá Riddles in Performance: Content and ContextDocument25 pagesNotes: 1 Yorùbá Riddles in Performance: Content and ContextDofono ty NísèwèNo ratings yet

- C.V ZeeshanDocument1 pageC.V ZeeshanZeeshan ArshadNo ratings yet

- Our American HeritageDocument18 pagesOur American HeritageJeremiah Nayosan0% (1)

- NYS OPRHP Letter Re IccDocument3 pagesNYS OPRHP Letter Re IccDaily FreemanNo ratings yet

- Managing Transaction ExposureDocument34 pagesManaging Transaction Exposureg00028007No ratings yet

- Merger and Demerger of CompaniesDocument11 pagesMerger and Demerger of CompaniesSujan GaneshNo ratings yet

- P 141Document1 pageP 141Ma RlNo ratings yet

- Case Study of Asahi Glass CompanyDocument22 pagesCase Study of Asahi Glass CompanyJohan ManurungNo ratings yet

- ISA UPANISHAD, Translated With Notes by Swami LokeswaranandaDocument24 pagesISA UPANISHAD, Translated With Notes by Swami LokeswaranandaEstudante da Vedanta100% (4)

- The Last LeafDocument42 pagesThe Last LeafNguyen LeNo ratings yet

- 1.1.1partnership FormationDocument12 pages1.1.1partnership FormationCundangan, Denzel Erick S.100% (3)

- Research ProposalDocument8 pagesResearch ProposalZahida AfzalNo ratings yet

- Accounting Concepts and Conventions MCQs Financial Accounting MCQs Part 2 Multiple Choice QuestionsDocument9 pagesAccounting Concepts and Conventions MCQs Financial Accounting MCQs Part 2 Multiple Choice QuestionsKanika BajajNo ratings yet

- Anouk - Hotel New YorkDocument46 pagesAnouk - Hotel New YorkRossi Tan100% (2)

- Bhuri Nath v. State of J&K (1997) 2 SCC 745Document30 pagesBhuri Nath v. State of J&K (1997) 2 SCC 745atuldubeyNo ratings yet