You might also like

- International Macroeconomics 4th Edition Feenstra Solutions ManualDocument25 pagesInternational Macroeconomics 4th Edition Feenstra Solutions ManualElizabethPhillipsfztqc100% (64)

- International Economics 4th Edition Feenstra Solutions Manual DownloadDocument15 pagesInternational Economics 4th Edition Feenstra Solutions Manual DownloadJane Wright100% (22)

- International Macroeconomics 4th Edition Feenstra Solutions Manual DownloadDocument9 pagesInternational Macroeconomics 4th Edition Feenstra Solutions Manual DownloadArthur Gundrum100% (21)

- 1predicting Bond Returns 70 Years of International Evidence - RobecoDocument40 pages1predicting Bond Returns 70 Years of International Evidence - RobecopukkapadNo ratings yet

- Lecture 10. The Great ModerationDocument41 pagesLecture 10. The Great Moderation100331798No ratings yet

- P5000 (At3502064) 98725-45100 Cat Engine (1) (K21 and K25) (Upto March 2018) Engine Mechanical 102-01 Engine Gasket KitDocument243 pagesP5000 (At3502064) 98725-45100 Cat Engine (1) (K21 and K25) (Upto March 2018) Engine Mechanical 102-01 Engine Gasket Kit2119100146No ratings yet

- Less Than A Bubble, More Than A Burst: Randall DoddDocument36 pagesLess Than A Bubble, More Than A Burst: Randall DoddtofumasterNo ratings yet

- Employee ID Employee Name Policy No Salary Date Premium Increamental Premium Loan Received Loan InterestDocument18 pagesEmployee ID Employee Name Policy No Salary Date Premium Increamental Premium Loan Received Loan Interestimrahuljangir4uNo ratings yet

- Financial Crisis 2007-08Document24 pagesFinancial Crisis 2007-08lnt komatsuNo ratings yet

- International Economics 4th Edition Feenstra Solutions ManualDocument15 pagesInternational Economics 4th Edition Feenstra Solutions ManualAmberFranklinegrn100% (36)

- Introduction To The Fifth Power Plan: Figure 1-1 - Daily Average Firm Prices at Mid ColumbiaDocument11 pagesIntroduction To The Fifth Power Plan: Figure 1-1 - Daily Average Firm Prices at Mid Columbiawildan irfansyahNo ratings yet

- Tablename: Wellid DateDocument100 pagesTablename: Wellid DateAli maghrbiNo ratings yet

- Aluminium Warehousing, Premiums and PricesDocument11 pagesAluminium Warehousing, Premiums and Pricesfiki arifNo ratings yet

- MonetaryPolicyShocksAndStockReturns PreviewDocument44 pagesMonetaryPolicyShocksAndStockReturns PreviewcastjamNo ratings yet

- Real Business Cycles ComDocument30 pagesReal Business Cycles ComAnubrat SarmaNo ratings yet

- More Wealth Destruction Ahead Part One December 2 2022Document26 pagesMore Wealth Destruction Ahead Part One December 2 2022Chris BelchamberNo ratings yet

- Development of Local Currency Bond Markets: The Indian ExperienceDocument33 pagesDevelopment of Local Currency Bond Markets: The Indian ExperienceAvinash GambhirNo ratings yet

- Lecture Added Foreign Direct Investment UpdatedDocument32 pagesLecture Added Foreign Direct Investment UpdatedKaahlNo ratings yet

- Analyse The Relationship Between Government Spending and Investment Spending For The US Economy in The Past 20 YearsDocument7 pagesAnalyse The Relationship Between Government Spending and Investment Spending For The US Economy in The Past 20 YearsNeil VictorNo ratings yet

- Time Flies When You're Having FunDocument9 pagesTime Flies When You're Having FunMatt EbrahimiNo ratings yet

- Sie TABELDocument1 pageSie TABELlifetec2007No ratings yet

- Report OnDocument9 pagesReport Onapi-3712367No ratings yet

- Thailand's Monetary Policy Since The 1997 CrisisDocument14 pagesThailand's Monetary Policy Since The 1997 CrisisRafael FerreiraNo ratings yet

- Cirasino HollandersDocument14 pagesCirasino HollandersLovemore TshumaNo ratings yet

- Employee ID Employee Name Policy No Salary Date Premium Increamental Premium Loan Received Loan InterestDocument18 pagesEmployee ID Employee Name Policy No Salary Date Premium Increamental Premium Loan Received Loan Interestimrahuljangir4uNo ratings yet

- Employee ID Employee Name Policy No Salary Date Premium Increamental Premium Loan Received Loan InterestDocument18 pagesEmployee ID Employee Name Policy No Salary Date Premium Increamental Premium Loan Received Loan Interestimrahuljangir4uNo ratings yet

- Chart 3 The Coincident Index and The Malaysian Business CyclesDocument8 pagesChart 3 The Coincident Index and The Malaysian Business Cyclessmazadamha sulaimanNo ratings yet

- The Dynamics of U.S. Crude Oil ProductionDocument7 pagesThe Dynamics of U.S. Crude Oil ProductionMario Alejandro Mosqueda ThompsonNo ratings yet

- Competitive Devaluations and The Trade Balance in LessDocument13 pagesCompetitive Devaluations and The Trade Balance in LessDavid PaselloNo ratings yet

- Mach Dieu Khien 2 Dong Co (Dong Co 1 Chay Truoc Va Dung Sau Dong Co 2)Document2 pagesMach Dieu Khien 2 Dong Co (Dong Co 1 Chay Truoc Va Dung Sau Dong Co 2)Nguyen Le Hoang HuyNo ratings yet

- Prelist Presentation Final 2014Document29 pagesPrelist Presentation Final 2014Justin CarruthNo ratings yet

- Forex Portfolio For January 2011Document4 pagesForex Portfolio For January 2011Trading FloorNo ratings yet

- Name: Stefan Sookoo STUDENT NUMBER: 1002899562 Professor: Robert Mckeown Date Submitted: Monday 26 MARCH 2018 CLASS: ECO208Y1Document12 pagesName: Stefan Sookoo STUDENT NUMBER: 1002899562 Professor: Robert Mckeown Date Submitted: Monday 26 MARCH 2018 CLASS: ECO208Y1bcs36bearNo ratings yet

- Intro Energy Insurance GardDocument198 pagesIntro Energy Insurance GardMurat YilmazNo ratings yet

- 4.4 The Role of International TradeDocument5 pages4.4 The Role of International TradeMingyu LiangNo ratings yet

- GP35NM 98725-42000 Cat Engine (GK15/GK21/GK25) (From Aug 14 2018) Engine Fig.150aa Oil Pump and FilterDocument2 pagesGP35NM 98725-42000 Cat Engine (GK15/GK21/GK25) (From Aug 14 2018) Engine Fig.150aa Oil Pump and FilterclavergaraNo ratings yet

- Employee ID Employee Name Policy No Salary Date Premium Increamental Premium Loan Received Loan InterestDocument18 pagesEmployee ID Employee Name Policy No Salary Date Premium Increamental Premium Loan Received Loan Interestimrahuljangir4uNo ratings yet

- 1 Country Report AlbaniaDocument27 pages1 Country Report AlbaniaCarlos A GonzaNo ratings yet

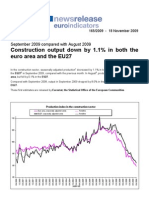

- Industy Output EU November: - 1,1%Document6 pagesIndusty Output EU November: - 1,1%Frode HaukenesNo ratings yet

- Employee ID Employee Name Policy No Salary Date Premium Increamental Premium Loan Received Loan InterestDocument18 pagesEmployee ID Employee Name Policy No Salary Date Premium Increamental Premium Loan Received Loan Interestimrahuljangir4uNo ratings yet

- Shopdrawing of Aluminum Window and Door - Revision 4 - 6.24.22Document22 pagesShopdrawing of Aluminum Window and Door - Revision 4 - 6.24.22Gerald DeOcampoNo ratings yet

- On InflationDocument10 pagesOn Inflationmajor raveendraNo ratings yet

- Combinepdf 2Document12 pagesCombinepdf 2hmue19902No ratings yet

- HDB Annual Report FY 20122013 Key Statistics PDFDocument20 pagesHDB Annual Report FY 20122013 Key Statistics PDFmahmudmuktafafifNo ratings yet

- External Debt Development and Management: Presentations On IndiaDocument22 pagesExternal Debt Development and Management: Presentations On IndiaYasser KhanNo ratings yet

- Morning News Notes:2010-03-15Document2 pagesMorning News Notes:2010-03-15glerner133926No ratings yet

- Brother Mfcj6510dw PL m11 eDocument33 pagesBrother Mfcj6510dw PL m11 eBenny BinjuaNo ratings yet

- The Stock Market in MarchDocument2 pagesThe Stock Market in MarchJohn Paul GroomNo ratings yet

- Chapter 2Document31 pagesChapter 2jrenceNo ratings yet

- Click GuideDocument1 pageClick GuideZyn VillanuevaNo ratings yet

- Most Recent Advances in Diesel Engine Catalytic SoDocument27 pagesMost Recent Advances in Diesel Engine Catalytic SoLe NamNo ratings yet

- Dervative Market, London School of EconomicDocument29 pagesDervative Market, London School of EconomicUyên NguyễnNo ratings yet

- Forex Portfolio For February 2011Document4 pagesForex Portfolio For February 2011Trading FloorNo ratings yet

- Parts Reference List: Model: DCP-8070D MFC-8370DN / MFC-8380DNDocument36 pagesParts Reference List: Model: DCP-8070D MFC-8370DN / MFC-8380DNPatrykNo ratings yet

- Parts Reference List: Model: DCP-8070D MFC-8370DN / MFC-8380DNDocument36 pagesParts Reference List: Model: DCP-8070D MFC-8370DN / MFC-8380DNPatrykNo ratings yet

- Impact of Foreign Exchange Reserves On Nigerian Stock MarketDocument8 pagesImpact of Foreign Exchange Reserves On Nigerian Stock MarketAaronNo ratings yet

- Petroleum Euro EmissionDocument8 pagesPetroleum Euro EmissionRendra Ananta Prima HardiyantaNo ratings yet

- FindingsDocument88 pagesFindingsValerie Din-din Charcos AlegadoNo ratings yet

- IFIN - Lecture 5: Foreign Exchange Exposure and Hedging - Part 1Document26 pagesIFIN - Lecture 5: Foreign Exchange Exposure and Hedging - Part 1PhilipNo ratings yet

- IFIN - Lecture 4: International Parity Conditions Predicting Exchange RatesDocument27 pagesIFIN - Lecture 4: International Parity Conditions Predicting Exchange RatesPhilipNo ratings yet

- IFIN - Lecture 1: International Trade TheoryDocument26 pagesIFIN - Lecture 1: International Trade TheoryPhilipNo ratings yet

- IFIN - Lecture 2: Basics of Currency ExchangeDocument28 pagesIFIN - Lecture 2: Basics of Currency ExchangePhilipNo ratings yet

- FinalDocument16 pagesFinalAshish Saini0% (1)

- A Tale of Two Exchange Rate Systems: Singapore and Hong Kong. How Well Have Their Respective Monetary/exchange Rate Systems Served Their Economies?Document23 pagesA Tale of Two Exchange Rate Systems: Singapore and Hong Kong. How Well Have Their Respective Monetary/exchange Rate Systems Served Their Economies?kangweeeeeNo ratings yet

- Foreign ExchangeDocument9 pagesForeign ExchangeTopuNo ratings yet

- Case Chap-09Document4 pagesCase Chap-09Kamrul RakibNo ratings yet

- 7.2credit Creation & MBDocument49 pages7.2credit Creation & MBJacquelyn ChungNo ratings yet

- Man - Solutions - Insights - Inflation RegimeDocument30 pagesMan - Solutions - Insights - Inflation RegimemohammedNo ratings yet

- W7 Module 008 Determinants of The Money SupplyDocument9 pagesW7 Module 008 Determinants of The Money SupplyJustin GutierrezNo ratings yet

- Money Growth InflationDocument55 pagesMoney Growth InflationSimantoPreeom100% (1)

- Friendly Loan AgreementDocument2 pagesFriendly Loan AgreementKenny Loh Li Wei0% (2)

- Class Assignment No: 01Document5 pagesClass Assignment No: 01Umar Shahzad NasirNo ratings yet

- Relationships Among Inflation, Interest Rates, and Exchange RatesDocument13 pagesRelationships Among Inflation, Interest Rates, and Exchange RatesibrahimNo ratings yet

- Bems Et Al (2018)Document26 pagesBems Et Al (2018)Gustavo QuintulenNo ratings yet

- 5) Exam Is Due Back Before Midnight (EST) On Nov 5: WWW - Federalreserve.govDocument3 pages5) Exam Is Due Back Before Midnight (EST) On Nov 5: WWW - Federalreserve.govTrevor TwardzikNo ratings yet

- Spec 2008 - Unit 2 - Paper 1Document11 pagesSpec 2008 - Unit 2 - Paper 1capeeconomics83% (12)

- Quantitative and Qualitative Instruments of Monetary PolicyDocument11 pagesQuantitative and Qualitative Instruments of Monetary PolicyVenkat SaiNo ratings yet

- Delhi Public School Sangrur: Multiple Choice QuestionsDocument9 pagesDelhi Public School Sangrur: Multiple Choice Questionsprateek gargNo ratings yet

- Measuring The Cost of LivingDocument43 pagesMeasuring The Cost of LivingAman MallNo ratings yet

- Contoh Soalan InsakDocument5 pagesContoh Soalan InsakPai YeeNo ratings yet

- Why Study Money, Banking, and Financial Markets?Document25 pagesWhy Study Money, Banking, and Financial Markets?Ahmad RahhalNo ratings yet

- Monetary Policy, Instuments of Monetary Policy andDocument37 pagesMonetary Policy, Instuments of Monetary Policy andkunkunkunkunNo ratings yet

- Mnitest Chapter 18Document2 pagesMnitest Chapter 18An DoNo ratings yet

- (ST) 02-Measuring The Cost of LivingDocument55 pages(ST) 02-Measuring The Cost of LivingThanh Ngan DuongNo ratings yet

- Exchange Rate QuestionsDocument5 pagesExchange Rate QuestionsHoàngAnhNo ratings yet

- Islamic Credit ManagementDocument14 pagesIslamic Credit ManagementAncoi Ariff CyrilNo ratings yet

- Monetary Policy in Developing CountryDocument13 pagesMonetary Policy in Developing Countryvivek.birla100% (1)

- GL4102-07-Equivalence and Compound Interest-BaruDocument34 pagesGL4102-07-Equivalence and Compound Interest-BaruVicky Faras Barunson PanggabeanNo ratings yet

- How RBI Went Wrong On Inflation - MintDocument11 pagesHow RBI Went Wrong On Inflation - MintUdbhavNo ratings yet

- Zimbabwe: From Hyperinflation To Growth, Cato Development Policy Analysis No. 6Document36 pagesZimbabwe: From Hyperinflation To Growth, Cato Development Policy Analysis No. 6Cato Institute100% (3)

- Lesson-3 EeDocument15 pagesLesson-3 EeChristian MagdangalNo ratings yet

- Methods of Credit Control Used by Central BankDocument5 pagesMethods of Credit Control Used by Central BankAnkit GuptaNo ratings yet